The Los Angeles Area

FASHION INDUSTRY PROFILE

November 2011

The Los Angeles Area Fashion Industry Profile

Sponsored by CIT

November 2011

CIT Trade Finance

CIT Trade Finance is one of the nation’s leading providers of factoring and financing

to the apparel industry. CIT tailors financial solutions that help companies of all

sizes increase sales, improve cash flow, reduce operating expenses and eliminate

customer credit losses. CIT serves apparel companies ranging in size from $2 million

to $1 billion in annual sales that sell to over 300,000 wholesale and retail customers

nationwide. CIT’s internet-based platform provides clients with real-time credit

approvals and comprehensive accounts receivable information. To learn more, visit

www.cit.com/TradeFinance.

Written by Dr. John J. Blank, Deputy Chief Economist, with assistance from Rafael De Anda.

Very special thanks go out to Ilse Metchek, President of the California Fashion Association, for key

guidance and insights. Special thanks goes to CIT for its sponsorship of this report. To California

Fashion Association members, my appreciation for such a vibrant industry to write about.

And with fond remembrance of Jack Kyser, whose spirit permeates this report.

Note: This report incorporates apparel manufacturing (NAICS 315) and textile mills (NAICS 313) data.

Both of these segments in the value chain have a strong presence in the Southland. This report also

includes apparel, piece goods, and notions merchant wholesaler data found in NAICS 4243. Be aware

that a "piece goods and notions" portion of sales located within this wholesale trade category makes up

around 10%. It will not cover the textile products industry, which generally includes home decoration

products such as linen and carpet. Finally, this report does not cover apparel retailing in much detail.

As the premier business leadership organization, the Los Angeles Economic Development Corporation's

(LAEDC) mission is to attract, retain, and grow businesses and jobs in the regions of Los Angeles County,

as well as to identify trends and affect positive change for the local economy. Since 1996, the LAEDC

Business Development team has helped in the creation, retention, and attraction of more than 171,000

jobs in over 1,350 businesses, with a direct economic impact of $8.4 billion.

The Kyser Center for Economic Research at the LAEDC is a key source for current and forecast data on

Southern California's economy. Regular publications include: An Annual and Semi-Annual Economic

Forecast & Industry Outlook, International Trade Trend & Impacts, L.A. Stats, Manufacturing in Southern

California, a weekly e-Edge email series, and a variety of regional and industry level economic reports

such as the one you are about to read. All reports and data are provided free to the general public via

our information website at http://www.laedc.org.

In addition, the LAEDC Economic and Policy Analysis Group offers custom research with expertise in

transportation, the environment, infrastructure, regional trends, and regional industry analysis.

Disclaimer: The opinions, statement, and information that appear in this report are those of the LAEDC

and do not necessarily reflect the views or outlook of CIT. CIT does not endorse or certify the accuracy of

such opinions, statements, and information.

© 2011 Los Angeles County Economic Development Corp., 444 South Flower St., 34th Floor, Los Angeles,

CA 90071. Web: http://www.laedc.org, Tel: (213)-622-4300 or (888) 4-LAEDC-1. Fax: 213-622-710

Table of Contents

Executive Summary ....................................................................................................................................................... 1

Los Angeles Apparel Industry Profile ..................................................................................................................... 2

The Apparel Industry by the Numbers ..................................................................................................................... 5

Overall Employment Facts ....................................................................................................................................... 7

Wholesaler, Manufacturing and Textiles Employment .......................................................................................... 11

Wages and Earnings ............................................................................................................................................... 15

A Demographic Profile of Apparel Manufacturing Workers .................................................................................. 19

Merchandise Prices ................................................................................................................................................ 19

Finance ................................................................................................................................................................... 23

International Trade ................................................................................................................................................ 26

Indirect Impacts ................................................................................................................................................... 29

Los Angeles Apparel Manufacturing: An Industry Under Siege ............................................................................ 31

A Design-driven Industry ........................................................................................................................................ 31

...Dominated by Immigrants................................................................................................................................... 32

Perceptions and Misperceptions ............................................................................................................................ 32

A Truly Global Industry ........................................................................................................................................... 34

Niche Markets in Quick-Turn Merchandise ............................................................................................................ 36

Los Angeles and Orange Counties: Two Distinct Trendsetters .............................................................................. 37

Technology Comes to the Rescue? ........................................................................................................................ 38

Labor Burdens: A Barrier to Job Growth ............................................................................................................... 39

Barriers to Exporting .............................................................................................................................................. 40

The March Towards Free Trade Continues ........................................................................................................... 42

Los Angeles and New York: Friends of Foes? ....................................................................................................... 43

Textiles Manufacturing: Another Sunset Industry ............................................................................................... 44

Topping it Off: Cosmetics, Jewelry and Footwear ............................................................................................... 44

Outlook for Los Angeles’ Apparel Industry ........................................................................................................... 46

Pluses ..................................................................................................................................................................... 46

Minuses .................................................................................................................................................................. 47

Items to watch ....................................................................................................................................................... 47

What Can be Done to Support the Industry ......................................................................................................... 48

Quotes from Vogue on "Made in California" ....................................................................................................... 49

Index of Statistical Tables

Table 1: Companies in California with Revenues of $1 Million and Greater, 2011 ................................... 24

Table 2: Conditions of Financial Stress in L.A. County Apparel Industries, August 2011 ........................... 25

Table 3: Los Angeles Customs District: Textile and Apparel Imports, 2010 .............................................. 27

Table 4: Direct & Indirect Apparel/Textiles Earnings in Los Angeles County, 2008 ................................... 30

Table 5: Direct & Indirect Apparel/Textile Jobs in Los Angeles County, 2008 ........................................... 30

Table 6: Apparel & Textiles Employment In Los Angeles County vs. New York PMSA, 2009 .................... 41

Table 7: Other Fashion-related Industries ................................................................................................. 46

LAEDC - Kyser Center P a g e | 1 Fashion Industry Profile 2011

Executive Summary

Our Key Strengths

- Massive economic impact of apparel on the L.A. economy. Over $40B in L.A. apparel imports, over

$13B in local revenues, and at least $6.0B flowing into local incomes.

- A global industry with durable reasons for being in L.A. in the future --with its powerful combo of

geography and orientation to fast fashion.

- A U.S. fast-fashion industry dominated by L.A retailers like Forever 21 Inc., Wet Seal, and Papaya.

- Enduring popularity of L.A. based design inspired by the sun, light, nature, and easy living.

- A concept of "L.A. Style" constantly propagated by media obsession with Hollywood celebrities.

- L.A. brands and designer names command a price premium, and our wholesalers keep growing.

- Tech helps L.A.'s design shops stay competitive -- shortening product cycles and reducing costs.

- The competitive advantage of L.A.'s textiles industry -- in design, in the ability to diversify product lines,

which involves processes with many layers of expertise, speed, and a willingness to try new things.

Whither Wages and Jobs?

- Export sales and recent global expansions can substantially add to L.A. jobs.

- Stability of wages in the industry in the L.A. area, while China is shifting to higher wage industries.

- A "second migration" to lower wage countries --from China to places like Vietnam or Bangladesh-- is

under way. These country's politics, regulations, and taxes can be dysfunctional, sometimes severely so.

- The L.A. apparel industry of today has greatly improved working conditions from ten years ago.

- Though jobs losses here are disheartening, L.A. is doing much better than national trends.

- Many forms of L.A. employment fall outside the three catch-all's of apparel manufacturing, textiles,

and wholesalers.

Major Stresses

- Globalization.

- Cotton prices have had a major impact on the industry.

- In light of industry financial stress numbers, a key implication: small sized firms in L.A. (below $2M in

revenues) have a greater chance of operating under conditions of financial stress.

LAEDC - Kyser Center P a g e | 2 Fashion Industry Profile 2011

THE LOS ANGELES AREA APPAREL INDUSTRY PROFILE -- 2011

The fashion industry is perhaps the most under-appreciated industry in Los Angeles. It's reach is global.

L.A.'s apparel industry success has long been driven by the pull of design talent; favorable cost

economics; the appeal of casual clothing (particularly denim); the global reach of technology and

fashion; and speed to market. Over $40 billion in apparel imports comes through L.A. ports; local

businesses earn at least $13 billion from just the L.A. County apparel wholesale and manufacturing

businesses; and their workers earn over $6.0 billion in direct, indirect, and induced income. This vibrant

industry still has lots more potential for expansion.

The mere mention of apparel manufacturing, unfortunately, can conjure up very dated images of

sweatshops full of minority women operating sewing machines next to a mountain of cut fabric and

under the eye of abusive bosses. That's not the true picture of the multiple faces within the apparel

industry in today's Los Angeles. Instead, the image should be one of design entrepreneurs and models

in a design studio located somewhere around 9th and Los Angeles; their workers sit near this well-lit

design studio, imagining new clothing designs and sending them electronically to offshore factories, or

to a local contractor; graphic artists electronically draw sketches for the next set of online ads; logistics

experts arrange for merchandise to be shipped to distribution centers or specialized clothing stores

around the world; fashion photographers take pictures against the backdrop of Pacific beaches; fashion

models walk down runways; or freight forwarders electronically sign customs papers for a Chinese

container full of finished merchandise. Furthermore, while local apparel and textile manufacturing jobs

have been declining since 2000, the numbers in wholesaling, i.e. 'jobber' employment, have been

increasing. The most interesting, most remunerative, and locally clustered jobs, ---customer-facing

design work--- are increasing too.

The woes of local apparel manufacturers have not diminished the popularity of L.A. based design

inspired by the sun, light, nature, and easy living. These designs are collectively known as the "L.A.

Style". The design side has continued to stay local and continues to prosper only by interacting with this

fertile local environment. The divergent fates of the various parts in the apparel value chain speak to a

relentless drive towards getting more revenues. First, from greater use of the sophisticated skills,

talents, and customer insights offered by local design entrepreneurs. And then preserving profit

margins -- by utilizing low skill workers to cut and sew ever higher volumes of mass-produced apparel in

far flung regions of the world.

Unfortunately, many people judge the current state of the L.A. apparel industry by using the most

readily available data -- employment. To counter this data, consider this: in a sign of this industry's

enduring importance to the regional economy, total wages earned by the L.A. County apparel industry

have remained stable over the last decade. Fewer apparel manufacturing jobs have come with (and

been caused by) a steady increase in weekly earnings for these workers.

LAEDC - Kyser Center P a g e | 3 Fashion Industry Profile 2011

Variations of Fashion Industry Business Models

Fashion design and the apparel production industry in Los Angeles have taken on a rich variety of

corporate forms. Eleven are worth mentioning by name. An example of a company (or set of

companies) that execute their business strategy using each of the eleven specific corporate forms

follows.

1. Large U.S. Conglomerate with Local Subsidiary - Lucky Brand, Perry Ellis, Warnaco

2. International Corporation with U.S. Brand Entity - Billabong, Speedo

3. Licensee of International Corporation - Jerry Leigh (Licensee of Disney)

4. Manufacturing Exclusively for Retail - Bebe, Gap, Forever 21

5. Separate Divisions of 'Umbrella' Corporation - Roxy for Quicksilver/ Vince for Kellwood

6. Owner/Entrepreneur/Domestic Production -Vertical -- American Apparel, St. John

-Using Contractors -- True Religion

7. Owner/Sales Executive -Joe Jeans, Hard Tail

8. Owner/Designer -Trina Turk, Sue Wong

9. Owner/Production Executive -Hudson, Knit Works, (Private label children's wear developers)

10. Owner/Entrepreneur/Importer - Body Glove, California Dynasty

11. Brand Companies - Entities that solely own intellectual property and license the brands to various

manufacturers. Such entities drove the rise of several prominent brands in recent years, including many

originating from SoCal (e.g. Iconix, Inc. owns Rampage, OP, and Ed Hardy). In L.A. County, the Cherokee

Group based in Van Nuys is a great example.

Many L.A. apparel "manufacturers" actually do not manufacture anything. Brand-less private label

contractors, similar to the Original Equipment Manufacturers (OEMs) and parts supplier relationships in

the auto and computer industries, actually do the cutting and sewing. The manufacturers are legally

responsible for ultimately fulfilling their contracts with retailers, the quality of their products, and their

contractors' labor practices regarding wage and overtime issues. Since contractors can bid for work

orders from many manufacturers, many are highly specialized and efficient at their core competencies.

By using contractors, the manufacturers are also able to adjust the apparel production rates depending

on market demand, structuring cost systems that are more variable and less fixed. (In this report, data

for "apparel manufacturing' refer to both manufacturers and contractors because it's hard to separate

the two in official statistics. We will specify the focus of the particular discussion when appropriate.)

LAEDC - Kyser Center P a g e | 4 Fashion Industry Profile 2011

Looking back at jobs data, apparel manufacturing jobs in L.A. County started a decline around 1996.

The North American Free Trade Act (NAFTA) between the U.S., Canada, and Mexico was a seminal event

for the Los Angeles-centered apparel industry cluster. Implementation of NAFTA on January 1, 1994,

brought the immediate elimination of tariffs on more than one half of U.S. imports from Mexico and

more than one third of U.S. exports to Mexico. Within 10 years, all U.S.-Mexico tariffs would be

eliminated except for some U.S. agricultural exports.

For the L.A. apparel industry, the NAFTA made it easier for apparel manufacturers to make finished

products with cheaper labor. At first, the early apparel outsourced to Mexico was often shipped back

late, service was poor, and fabric quality was not up to par. But the door to a global outsourcing

business had been opened a crack, and that door would be opened wider and wider.

Scroll into 1997, a year tied to the Asian Financial Crisis. After the sudden pullback of capital, import-

export manufacturers located in Asia benefitted from the pull of depreciating Asian currencies against

the U.S. dollar. Collapsing internal demand flattened Asian low-skilled hourly wage profiles across the

region. Some of these Asian workers served globally-sourced apparel contractors.

A strong push came from higher U.S. hourly wages and regulations too. In 1997, as just an example,

California enacted AB 633. This state law said that brand holders have joint liability with contractors for

issues like age discrimination and OSHA requirements, and for worker's compensation. Taking both the

push and pull factors in combination, and an already strong cost advantage found new traction. The

L.A. apparel industry shifted more and more labor-intensive production offshore to Asia, specifically to

China.

During this extended migration of activity, many L.A. apparel manufacturing firms could only stand and

watch as cheap imports flooded our ports. Some capitulated and closed their domestic factories and

moved production outside the U.S. Quicker turnaround, smaller volumes, and more frequent design

output have been the only tactics industries facing intense import competition from places like China

could employ to survive. Using these tactics, half the L.A. apparel manufacturing base has been able to

stay local.

During the mid to late 1990s, China also implemented a second five-year central plan to further develop

its market economy. This phase of plans opened China's coastal cities to greater import-export trade.

More and more, China's manufacturing and assembly operations participated in globally-sourced

industries -- aka operations like apparel and textile manufacturing. Soon, Chinese activities sunk more

deeply into the global manufacturing fabric. And this meant they captured the bulk of the U.S. market.

On December 1, 2007, under WTO rules, quotas on apparel shipped from China to the U.S. were dropped.

Apparel import volumes to the U.S. from China took another step up. But interestingly, manufacturing

the basic low profit margin items in apparel lines in China began to compete with other Chinese

industries for the services of expert sewing -- causing a rise in apparel manufacturing wages in China.

LAEDC - Kyser Center P a g e | 5 Fashion Industry Profile 2011

In 2009, the Commerce Department's Office of Textiles & Apparel (OTEXA) listed the top five suppliers

to the U.S. as follows:

Apparel to U.S.

Textiles to U.S.

1. China

1. China

2. Vietnam

2. Pakistan

3. Bangladesh

3. India

4. Honduras

4. South Korea

5. Indonesia

5. Mexico

Moving forward to data available in 2011, and you see the global apparel manufacturing industry looks

to generate $316 billion in export revenues. Major apparel producing countries in terms of export

revenues are China, Italy, Germany, Turkey, India, and Bangladesh according to the United Nations. The

major textile exporting countries include South Korea and Vietnam. Major companies include Youngor

Group (China), Armani (Italy), MOL Magazalari (Turkey) and Gokaldas Exports (India).

China accounts for 34% of the global apparel market, having seen its export revenues double over the

last decade. The Chinese apparel manufacturing industry includes about 18,000 companies, with a

combined annual revenue of about $200 billion, according to the National Bureau of Statistics of China.

However, China's wages are rising as its workforce shrinks, due to strict family-planning policies.

Apparel workers are also going into other Chinese industries, who compete for their skills by offering

better wages, hours, and working conditions. China now faces lower-skilled, lower-paying jobs moving

offshore. This so-called "second migration" is occurring to countries such as Bangladesh, Cambodia,

Indonesia, Laos, and Vietnam, according to apparel trading agent Li & Fung. Bangladesh and Cambodia

have the lowest wages in the world.

Today, rising wages in China and rising energy costs worldwide have combined to force up apparel

manufacturing and shipping costs tied to the mainland Chinese economy. In the last couple of years,

forces in market-driven growth increased the demand for labor and increased energy use. The overall

effects of prosperity have driven upwards a range of other Chinese costs too -- at a rate greater than in

the U.S. In 2011 and into 2012, "all-in" comparative cost advantages are starting to not be as wide.

China is focusing its next five year development plan to 2015 on creating success in high wage industries

like energy conservation & environmental protection, biotechnology, alternative energy, and new

materials. High end manufacturing is also a top goal.

Industry by the Numbers

The apparel marketing business is highly competitive, based on both price and fashion.

Small integrated manufacturers rely heavily on trade shows and personal contacts to market products to

merchandise buyers. Larger companies have a sales force. The profitability of a customer order

depends largely on its size. Many manufacturers depend on a few large customers for the bulk of their

LAEDC - Kyser Center P a g e | 6 Fashion Industry Profile 2011

business. Under some supply agreements with larger retailers, customers can cancel orders or return

unwanted inventory. To secure these orders, manufacturers often cut prices.

Materials typically account for 65% of apparel manufacturing costs. Although some textiles must be

bought from a single supplier, most textiles are available from numerous sources. Fabric imports have

increased steadily for several years, which includes large increases from China.

1

Several types of manufacturers exist.

Integrated manufacturers design and market their own clothing brands, and make

products both in their own manufacturing plants and in those of independent

contractors. Many clothing designers market their own brands, but contract out the

actual garment production.

Licensees operate their own manufacturing plants and market clothing under

license from the brand owner.

Contract manufacturers may have long-standing relationships (but not actual

contracts) with designers and marketers, or may use brokers to get new business.

Contract manufacturers get business on their ability to produce goods at low cost

and on time. Poor quality work is typically returned to the sewing manufacturer for

reworking or is discounted. The manufacturer placing the order typically owns and

supplies the materials used by contractors.

Despite attempts at greater automation, most apparel is still sewn using specialized sewing machines.

Equipment is bought from makers like Yamato or Juki. Computer systems have had a limited effect on

the manufacturing side of the industry, although computerized machines may be used to produce

patterns and cut materials. To compete effectively for the best contracts, domestic apparel

manufacturers have moved to greater automation, specialty production, and superior service.

The operations of most apparel manufacturers are similar. Designs for a piece of clothing are converted

into cloth patterns along with a plan for the sewing steps needed to produce the product. Cloth is cut in

various sizes (typically four or six sizes) in a cutting room (or cutting plant), and is then sewn (or "made-

up") into finished items by individual workers at sewing stations, in a series of assembly-line steps that

may require special sewing equipment. Finished goods are pressed, inspected, and packaged for

delivery.

Many manufacturers cut fabric in the U.S. and then ship it overseas for sewing into final garments. Such

operators benefitted from the NAFTA and CAFTA treaties. Exporting non-Chinese textiles into China is

difficult as best. China will not accept cut fabric for sewing, unless the textiles used are sourced in

China.

1

Industry Profile: Apparel Manufacturing, First Research, Copyright 2011, Hoover’s Inc., May 16, 2011.

LAEDC - Kyser Center P a g e | 7 Fashion Industry Profile 2011

Machinery that satisfactorily replaces worker's hands has been elusive, because of the soft nature of the

materials being handled. Some standardized articles made from stiff material, mainly jeans, can now be

sewn by semi-automated machinery that requires workers only to position the material. Because of the

different skills and equipment needed to produce different types of clothing, manufacturers usually

develop a specialty.

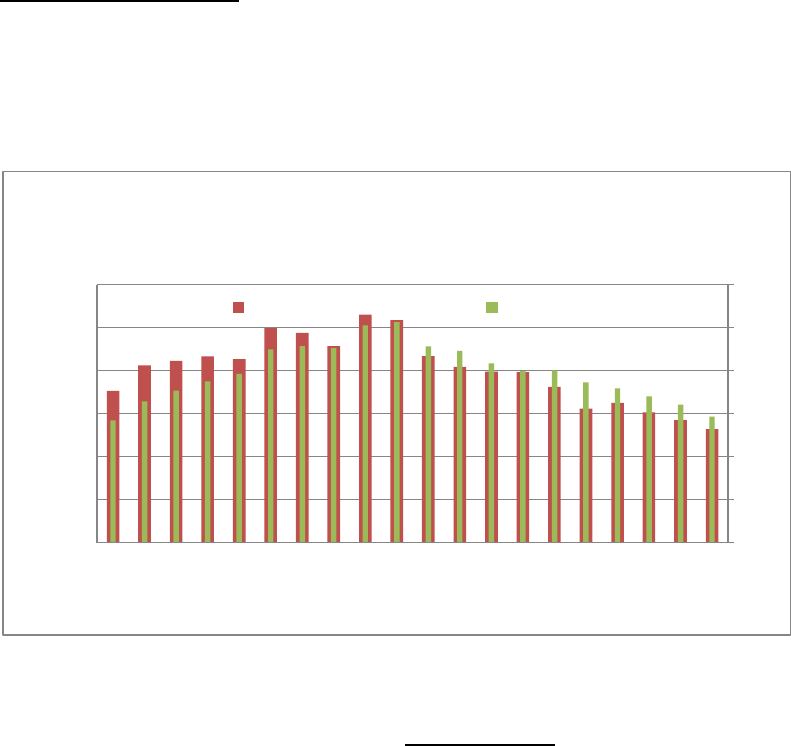

Overall Employment Facts

A collapse in L.A. County apparel establishments took down its manufacturing employment. Looking

back to the year 2000, and you see textile mill employment in L.A. County started its decline, spurred by

a steep rise in energy costs. For the past ten-plus years, the number of establishments in both apparel

manufacturing and textile mills in L.A. County has declined, year-after-year. See below:

When we looked at the three apparel industry sub-segments in the five county area during a four year

period from 2004 to 2008, (textile mills NAICs 313, apparel manufacturing 315, and apparel wholesaling

4243), we found total employment averaged 100,000 workers. The average number for establishments

in the five county area was around 6,400 firms. This implied that an "average" L.A. regional apparel firm

is small; employing around 15 workers.

0

100

200

300

400

500

600

0

1,000

2,000

3,000

4,000

5,000

6,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Number of Establishments in L.A. County

Apparel Mfg.

Textile Mills

Source: California Employment Development Department

Apparel Firms

Textile Firms

LAEDC - Kyser Center P a g e | 8 Fashion Industry Profile 2011

Profitability in individual companies depends on efficient operations and the ability to secure contracts

with clothing marketers. Annual revenue generated to the average company is about $115,000 per

production worker. Small companies can compete effectively with larger ones by specializing in a

particular type of apparel manufacture. The same is true for wholesalers. There are economies of scale

in manufacture. As a sewer gets up towards the 500th pair of jeans, the level of expertise keeps rising,

and output per unit of time increases with it. Making apparel is labor-intensive, making sure profitability

is closely tied to labor costs. Which is why manufacturers move operations to countries with lower

wages. With respect to apparel wholesaling, fewer employees are needed, as no production is required.

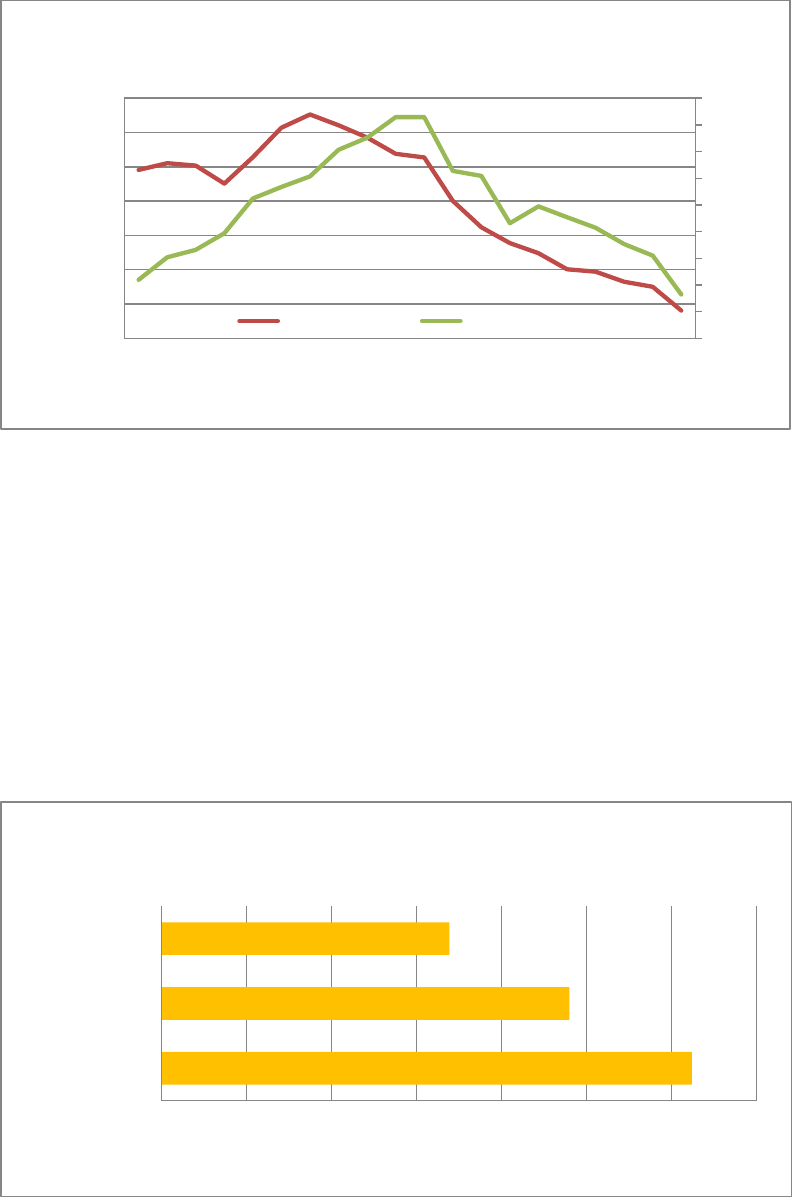

As the subsequent chart shows, most L.A. apparel employment is in very small firms -- one to four

employees.

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

From a 1996 Peak, LA County Lost Apparel Mfg. Jobs. Then in

2000, the Loss of Textile Mill Jobs

Apparel Mfg.

Textile Mills

Source: California Employment Development Department

Apparel Jobs

Textile Jobs

0 10 20 30 40 50 60 70

Wholesalers

Apparel Mfg.

Textile Mills

Further up the Value Chain, there is little in the way of

economies of scale and capital intensity, as evidenced by the

proportion of small 1-4 employee firms

Proportion of Firms with 1-4 Employees (%)

Source: U.S. Census, 2009 County Business Patterns

LAEDC - Kyser Center P a g e | 9 Fashion Industry Profile 2011

Even though jobs losses here are disheartening, L.A. is actually doing much better when compared to the

national trend.

While apparel industry employment has fallen across the United States, the share of employment

captured by the L.A. and Orange County apparel industry has increased. In 2002, for example, L.A. and

Orange County accounted for a 24% share of U.S. apparel manufacturing jobs. In 2009, this proportion

rose. Over 33% of U.S. apparel manufacturing jobs were located in L.A. or Orange County; over 20% of

apparel, piece goods, and notions merchant wholesalers were found here; and almost 7% of all textile

mill jobs. All of these proportions have risen, year-after-year, over the last decade. See below:

Additionally, many forms of L.A. employment in apparel fall outside the three broad catch-all categories.

For example, L.A. apparel industry experts count 1,050 independent fashion designers operating solo;

another 2,771 workers are employed in their independent showrooms; and then 1,240 textile reps and

another 865 home-based agents and brokers are out working on commission. Another bucket of L.A.

workers can be found in a range of ancillary activities like: packaging, labeling, and other support roles

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Firms

Total Wages

The Los Angeles Apparel Industry Makes up over 19% of all

L.A. County Manufacturing Firms, and over 7% of Total Wages

Source: U.S. Census County Business Patterns

0% 10% 20% 30% 40%

Textile mills

Apparel manufacturing

Apparel, piece goods, and notions

merchant wholesalers

LA and Orange County Apparel Industry

Share of Total U.S. Employment - 2009

Source: Dept. of Commerce, 2009 Country Business Patterns

LAEDC - Kyser Center P a g e | 10 Fashion Industry Profile 2011

(220 positions); in custom computer programming (69 positions); in fulfillment support services to

imports (1,100 positions); in consulting services (130 positions); in commercial rental (240 positions);

and in specialized local freight (560 positions). There are around 750 apparel educators teaching in 14

different institutions in the five county area too.

The subsequent table summarizes.

Related Industry Segments

# of Employees

# of Establishments

Independent Fashion Designers

1,050

1,050 (contracted consultants)

Independent Showrooms

2,771

888 (all categories)

Textile Reps

1,240

1,240 (wholesale trade agents & brokers)

Home-based Agents/Brokers

865

517 (no office address)

Outside Services

220

55 (packaging, labeling, support)

Technology

69

22 (custom computer programming)

Fulfillment

1,100

12 (support services to imports)

Labor Compliance

130

4 (consulting services)

Equipment Leasing

240

4 (commercial rental)

Educators

750

21 (teachers and administration

Distribution

560

6 (specialized local freight)

Grand Totals

8,995

3,802

Source: California Fashion Association

Including these activities means adding 8,995 workers operating in 3,802 establishments. This takes the

overall jobs tied to the apparel industry near to 110,000 workers. And the number of total

establishments is likely to be over 10,000.

A significant number of contract workers are not captured by official surveys too.

With rising worker's compensation and health insurance costs, some may think employers might be

tempted to hire contract workers instead of having them on permanent payrolls. While this may be

true, the reality is far more complex. Many workers, especially those who are fast and skilled,

constantly look for better opportunities among different contracting firms. Some do this so they can fill

up all the work hours they care to put in. As a result, the workforce is very fluid in the cut-and-sew

section of the apparel industry. Under these circumstances, benefits such as an employer-financed

(wholly or partially) health insurance program are difficult to manage. Job counts are no easier to

capture.

Contract workers cannot work from their homes. Home sewing is only allowed for craft items like

household-used knitting and pillows. Retailers face fines under California law if they buy sewn apparel

from home sewers. The practice of using home labor for commercial apparel manufacturing is illegal,

because power sewing machines are dangerous to children. Contractors who give work to home labor

will be punished along with the laborer. Not surprisingly, there have been no California Dept. of Labor

Standards and Enforcement (DLSE) violations in seven years.

LAEDC - Kyser Center P a g e | 11 Fashion Industry Profile 2011

Wholesaler, Manufacturing, and Textiles Employment

The data show us a genuine industry cluster exists in Los Angeles County!

Locating near other firms offers the chance for free information to spill over more often, to easily share

paid resources, and keep design trends up-to-date. In recent years, L.A. County accounts for 86% of the

apparel manufacturing employment and 84% of wholesale merchant employment in the five county

area. The apparel industry (excluding retailing) is one of the larger industries in the Los Angeles five-

county area.

Los Angeles County has the largest job count. With a steady distant second at 12% of apparel

manufacturing jobs, Orange County has a smaller base focused on surfwear and activewear. Orange

County has gained share in jobs over recent years, due to the acceptance of the surfer style. L.A. has a

classic manufacturing cluster surrounding the Fashion District in downtown Los Angeles. In the case of

Orange County, the industry is spread out.

Wholesale apparel data

Defining a wholesaling job is as much about what it is not, as what it is:

No design

No manufacturing

No production

No technical specs.

Just activity involved in the purchase and re-sale of completed apparel.

Wholesale apparel merchant jobs are more dispersed within the five county area. Ventura, San

Bernardino and Riverside Counties collected about 6% of apparel wholesale numbers. In recent years,

Orange County collected 10%.

80%

85%

90%

95%

100%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

In Terms of Apparel Manufacturing Jobs,

Orange County Has Grown its Share

Ventura

San Bernardino

Riverside

Orange County

Los Angeles

Source: U.S. Census, 2009 County Business Patterns

LAEDC - Kyser Center P a g e | 12 Fashion Industry Profile 2011

Apparel merchant wholesaling in L.A. County remains a cyclical business. Revenues grow with the

overall strength in the U.S. economy; slip back when it declines; and recover along with the rest of retail

sales.

Apparel wholesale jobs stayed in a very modest growth mode over the last ten years too -- adding +1,000

jobs in L.A. County from peak to peak.

Wholesaling employment benefits from both import and export activities. Small lot jobbers are in sync

with the fastest growth end markets, i.e. specialized retailers selling contemporary women's clothes.

Demand is mostly regional -- in California and Western states -- but a substantial national and

international traffic happens. L.A.'s large local market is one reason why apparel wholesaling firms

continue to prosper, even as L.A. County apparel manufacturing and textile employment declines

dramatically.

Third party logistics (aka "3PL's") are another source of L.A. County jobs for this industry

2

.

The very geography of L.A. and its proximity to Asia creates a natural driver of growth in the industry.

Shipments from Asia are weeks faster to Long Beach than to the East Coast. This allows an apparel

manufacturer to maintain better liquidity through faster inventory turns. Furthermore, a growing

number of apparel companies from around the United States are using 3PL's based in L.A. These 3PL's

receive containers, break them down, and then do the type of prep work normally done in the

company's own warehouses (i.e. hang tags, garment bags, hangers, and re-boxing). Then, they ship to

the wholesale customers. Very often the 3PL has access to the company's internal inventory

management and electronic data interchange (EDI) systems, which makes it a seamless process. These

shipments are booked as revenue for the wholesaler, wherever they may be located. But they

contribute directly to the apparel industry in L.A.

A concentration of trade facilitators in the immediate L.A. area --customs brokers, freight forwarders,

and trade attorneys-- make interaction with the 3PL’s easier for Los Angeles based importers too.

2

Attributed to Eric Fisch, Vice President, Commercial Banking and Sr. Apparel Analyst, HSBC in Los Angeles, CA.

80%

85%

90%

95%

100%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

In Terms of Apparel Wholesaler Jobs,

Orange County has Grown its Share

Ventura

San Bernardino

Riverside

Orange County

Los Angeles

Source: U.S. Census, 2009 County Business Patterns

LAEDC - Kyser Center P a g e | 13 Fashion Industry Profile 2011

In addition, the nearby Mexican maquiladoras (maquilas) apparel operations have improved in terms of

quality and labor force skills in recent years.

While one's initial inclination would be that this arrangement has drained jobs in SoCal, in many cases it

is the opposite. These lower wage apparel jobs would have gone to Asia, not California. What the

maquila's have fostered is growth in wholesaler jobs in SoCal, where they anchor due to the proximity to

the border. Because of the mechanics of the duty free program (goods need to originate in the U.S.,

have value added in Mexico, and then return to U.S.), apparel companies located in the rest of the

country do not utilize it. This has helped to foster growth in SoCal wholesalers.

Over the last cycle, L.A. County and Orange County showed a modest consolidation in the number of

wholesale firms.

At its peak in 2001, 19,600 workers at 2,500 firms were busy in L.A. County apparel wholesaling.

In the next wholesaling peak reached in early 2008, L.A. County recorded 20,700 people in a

smaller number of just 2,360 firms.

In 2001, Orange County had 3,000 wholesaling jobs at 300 firms.

At the next peak in 2008, Orange County offered 2,850 jobs at just 240 firms.

Stronger apparel wholesaling firms (still quite small in most cases) have been able to grow modestly;

often at the expense of firms who exited the market over the last ten years.

Wholesale apparel activity across California's counties is more dispersed than apparel manufacturing.

10,000

12,000

14,000

16,000

18,000

20,000

22,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Avg. Annual Employment of

Apparel Wholesalers

Shows an Increase Beginning in 2004

Apparel Wholesalers

Source: U.S. Census, 2009 County Business Patterns

Wholesale Jobs

LAEDC - Kyser Center P a g e | 14 Fashion Industry Profile 2011

See the subsequent chart to confirm:

Apparel manufacturing data

Using 2009 data, L.A. County apparel manufacturing jobs came in at 48,000 workers within 2,600 firms.

Over the last decade and more, L.A. County apparel manufacturing saw both jobs and establishments

cut in half. In Los Angeles County, the peak for apparel manufacturing activity came with 105,300 jobs

scored in 1996. The peak for L.A. County apparel manufacturing establishments came two years later in

1998 at 5,300 firms. Since then, in every consecutive year, both the L.A. County job and establishment

counts have fallen. Increasingly, consolidation and restructuring efforts have been to cut losses.

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Los Angeles, CA

Orange, CA

San Diego, CA

Alameda, CA

San Bernardino, CA

Ventura, CA

San Francisco, CA

Santa Barbara, CA

San Mateo, CA

Santa Clara, CA

Contra Costa, CA

Riverside, CA

Santa Cruz, CA

Marin, CA

Sacramento, CA

Napa, CA

San Luis Obispo, CA

Imperial, CA

Apparel, Piece Goods, & Notions Wholesaler Jobs in

California are mostly located in L.A. County, though

distribution is widely spread in nearby counties

Source: U.S. Census, 2009 County Business Patterns

0 10000 20000 30000 40000 50000

Los Angeles, CA

Orange, CA

San Francisco, CA

San Diego, CA

Alameda, CA

San Bernardino, CA

Santa Clara, CA

Marin, CA

Sonoma, CA

Ventura, CA

Sacramento, CA

San Mateo, CA

Contra Costa, CA

Yolo, CA

Kern, CA

Apparel Manufacturing Jobs 315:

L.A. County Leads the way in California

Source: U.S. Census, 2009 County Business Patterns

LAEDC - Kyser Center P a g e | 15 Fashion Industry Profile 2011

Textile mill data

Textiles mills in Los Angeles County performed under similar stress over the last decade. The 2009 data

put this sub-segment at 7,600 jobs and 290 firms. Again, a cut in half. Textiles mill employment in L.A.

County reached its peak in 1998 and 1999. At that time, these mills offered 14,300 jobs at 510 firms.

Wages & Earnings

Paradoxically, the average level of wages increased in recent years. More highly skilled specialty jobs

remained in the U.S. factories, while lower-skilled, lower-paying jobs moved offshore.

Annual performances of wages & earnings in L.A. County offer a good vantage point.

Since 2000, U.S. Census data show apparel manufacturing workers have taken home rising weekly

earnings in L.A. County. In 2011, an average apparel manufacturing worker is making over $600 a week.

In 2000, that same worker earned $400 a week. Putting in 40 hours each week in today's L.A. County

means L.A. County cut and sew apparel manufacturing jobs may pay $15 for an hour's worth of work.

And today's apparel wholesalers earn close to $900 a week. This is $22.50 an hour. In 2000 in

comparison, apparel wholesalers operating successfully in L.A. County pulled in $650 a week offering the

same services.

The subsequent chart shows this relentless upward increase...quite clearly!

0

200

400

600

800

1000

1200

1400

1-4

5-9

10-19

20-49

50-99

100-249

250-499

500-999

1000 or

more

Apparel Manufacturing 315 jobs in

L.A. County are in small firms (1-4, 5-9, & 10-19 employees)

Number of Firms

Source: U.S. Census, 2009 County Business Patterns

LAEDC - Kyser Center P a g e | 16 Fashion Industry Profile 2011

A private set of wholesale and apparel manufacturing data adjust these findings somewhat: According

to Dun & Bradstreet data drawn in August 2011, NAICs code 4243 for apparel wholesale jobs came in at

29,454 (42% of the cluster). NAICs for apparel manufacturing came in at 39,382 jobs (58% of the total

for the cluster) for a total of 68,836 jobs (roughly the same total number of jobs as the government's

data). This means several thousand higher-paying wholesale jobs in the Dun & Bradstreet database are

counted within apparel manufacturing jobs in the U.S. government's database.

Could higher-paying wholesaling jobs be masquerading as apparel manufacturing jobs? The Bureau of

Labor Statistics in May 2011 put the national average for apparel manufacturing jobs at $11.69 an hour,

versus the $15 an hour we calculated from the government data for L.A. County. A notable differential.

More than anything else, rising domestic (and locally-determined) hourly labor costs forced L.A. County

manufacturing and contracting firms to form relationships with outside suppliers. Mostly in China, but

also in a range of countries such as South Korea, Vietnam, Mexico, India, and Indonesia. Over the last

ten years, the rise in L.A. County hourly apparel manufacturing wages has been relentless.

Why?

In this region, the remaining L.A. apparel manufacturing and textile mill employment opportunities have

become increasingly specialized. Workers are also increasingly surrounded by larger numbers of better

paying jobs in service industries. These two effects have been seen across the United States economy

in all regions. Finally, increases in minimum wages have been implemented, forcing up the rest of

hourly pay scales with it. California’s minimum wage is $8.00 per hour (set January 1, 2008), while the

federal minimum wage is $6.55 per hour (set July, 2008).

Two charts below provide additional facts on the overall strength of L.A. County apparel industry wages

& earnings.

First, the total L.A. County apparel wage bill:

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Average Weekly Wage

L.A. County Average Weekly Wages

Apparel Wholesaling Pays Much Better

Apparel Wholesaling

Apparel Mfg.

Textile Mills

Source: U.S. Census, 2009 County Business Patterns

LAEDC - Kyser Center P a g e | 17 Fashion Industry Profile 2011

Second, L.A. County apparel wage data shown as the percent of all L.A. County private industry:

The BLS Quarterly Census of Employment and Wages (QCEW) offers annual salary data in the three sub-

industries in SoCal:

1. Using first quarter of 2011 data, L.A. County textile mill jobs paid $28K a year. Orange

County jobs paid $24K a year. Nationally, such jobs paid $30K a year.

2. Apparel manufacturing jobs? L.A. County paid $24K a year and Orange County paid

$27K a year. Nationally, "cut and sew" jobs paid $24K a year.

3. L.A. County wholesale apparel jobs? They paid $46K a year. Orange County jobs paid

$57K a year. Nationally, wholesale apparel jobs paid $52K a year.

Los Angeles County has kept a cost advantage in all three major areas of the apparel industry.

$0

$500,000,000

$1,000,000,000

$1,500,000,000

$2,000,000,000

$2,500,000,000

$3,000,000,000

$3,500,000,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Total Wages of L.A. County Apparel Industry

Textile Mills

Apparel Mfg.

Apparel Wholesalers

Source: U.S. Census, 2009 County Business Patterns

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

L.A. County Apparel Industry Total Wages

(as Percent of All Private Industry Wages)

Source: U.S. Census, 2009 County Business Patterns

LAEDC - Kyser Center P a g e | 18 Fashion Industry Profile 2011

L.A. County is a cheaper place to hire apparel workers. Orange County is a bit cheaper

to hire textile workers.

See subsequent chart for a summary comparing L.A. County and U.S. pay:

Looking for still another take on this industry?

Consider the American Apparel & Footwear Association's "2011 Salary Survey and Job Market Report".

Their 2000 respondents came from across the United States, with 90% of people working in apparel and

footwear firms of greater than 10 employees. 36% of respondents worked at the really big apparel and

footwear firms -- i.e. those above 1000 employees.

Their 2000 jobs fell into the following categories.

34% Design & Technical Development

14% Sales & Marketing

13% Production & Product Development

13% Planning and Merchandising

13% Retail, Ecommerce & Store Level

5% Operations & IT

1% Transportation & Logistics

1% Customs, Trade, & Compliance

Source: 24/Seven and American Apparel & Footwear Association, 2011

79% of respondents were female. 53% were single. 77% had no children at home. 67% had some

college attainment.

0 10 20 30 40 50 60

Textile mills

Apparel manufacturing

Apparel, piece goods, and

notions merchant wholesalers

Showing Los Angeles County has a cost advantage, U.S. worker pay

levels are higher in all three apparel industries

US Pay

LA Pay ($000)

Source: BLS (QCEW)

LAEDC - Kyser Center P a g e | 19 Fashion Industry Profile 2011

The median fashion and retail salary at the big U.S. companies was $70,000. At the top of the economic

totem pole in these big corporate apparel and footwear firms, the survey showed a SVP of Design could

make $390,000 a year; a Fashion Director up to $430,000 a year. The median compensation for a SVP

of Production/Sourcing individual made $260,000 a year. Entry level Associate Designers were paid a

median salary of between $40,000 and $50,000 a year. The same level of compensation was earned by

entry-level Purchasing/Sourcing Assistants.

A Demographic Profile of Apparel Manufacturing Workers

Demographic data from Census 2000 provide another glimpse into the apparel manufacturing sector.

(Census 2010 data are still not available.) Unfortunately, we are unable to distinguish between apparel

"manufacturers" and "contractors", which do most of the actual production work. Most data being

discussed here are likely from apparel manufacturing contractors.

Hispanics (81%) and Asians (16%) dominate the ranks of production workers.

Roughly two-thirds are women.

The results from the Census's 5-Percent Public Use Microdata Sample (5% PUMS) for the Los Angeles

five-county area affirm some of the perceptions about the apparel manufacturing industry. Most

workers did not complete high school and do not speak English proficiently. Over three-quarters are

non-citizens but may have permanent residency status and thus employment authorization. They work,

on average, 40 hours per week. Technical personnel, which includes engineers, computer

programmers, and mechanics are still dominated by minorities, but they tend to have a higher

educational attainment.

For comparison, consider the demographics of Designers & Researchers. Only 31% are Hispanic, 64%

have a college degree, and just 22% are non-citizens. Top Managers? 18% are Hispanic, 52% have a

college degree, and 25% are non-citizens.

Merchandise Prices

Like the computer industry, the apparel industry has had to do battle with falling prices for its products.

Falling average prices in the apparel sector have been caused by the shift of production to lower-cost

locales, changes in retailing, and a general acceptance of a more casual appearance for both workplace

and social occasions.

More and more apparel has been sold at value retailers (e.g. Wal-Mart and Target) and "wholesale

clubs" (e.g. Costco and Sam's Club) instead of department stores too. Mid-income consumers have

become more value-oriented in recent years, and discount chains upgraded their offerings to attract this

huge segment of the population. In some cases, chain stores licensed designer brands and have taken

LAEDC - Kyser Center P a g e | 20 Fashion Industry Profile 2011

over manufacturing responsibilities. Now, some once-hot designer brands are available at very low

prices through these stores.

Until 2008...

In the last three years, there has been a visible increase in apparel prices in Los Angeles.

Apparel making markets have experienced the effects of a rise in oil and of commodity prices such as

cotton and linen. These costs have yet to be passed on to consumers. Also, there is accumulating

evidence coming in from Asia, over a period of many years, that rising labor costs need to be passed on

too. Today, the rate of inflation in China is a key focus for domestic apparel makers.

A subsequent chart shows just how explosive cotton prices have been in the United States. Cotton prices

for export are 250% in this export index, while they used to be 100% just two years ago. It also shows a

cooling cotton price trend started in the first half of 2011. The U.S. South and California are some of the

world's biggest exporters of cotton.

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Retail Apparel Prices Rise in Los Angeles

Source: U.S. Dept. of Labor, Bureau of Labor Statistics

0

50

100

150

200

250

300

350

400

2006

2007

2007

2007

2007

2008

2008

2008

2008

2009

2009

2009

2009

2010

2010

2010

2010

2011

2011

Cotton Export Indices Show Surging Prices

Source: U.S. Dept. of Labor, Bureau of Labor Statistics

LAEDC - Kyser Center P a g e | 21 Fashion Industry Profile 2011

More globally, cotton prices spiked to $2.30 per pound in 2011 because of bad crops; brought on by

inclement weather and increasing world demand. They recently fell to around $1.05 per pound. In

addition, rising globally-set oil prices boosted prices for petroleum-based products such as nylon and

polyester. Raw materials make up a small fraction of the cost in an finished garment. But when the

underlying input price moves are this strong, they are felt. These rising costs could be passed on to

consumers.

Cotton prices have had a major impact on the industry. Towards the end of 2011, many wholesalers

are only beginning to realize their impact. They committed to purchase cotton months ago when cotton

prices were highest. The run-up in prices made the textile mills in Asia more conservative, forcing

wholesalers to pre-pay for cotton. This high-priced cotton is the raw material in goods they are now

delivering to retailers. Many retailers have also been aggressive in requesting price reductions that

mirror the recent reductions in cotton prices. This further pressures wholesalers. The combination of

these factors has caused both profit margin and cash flow issues for them.

In the following two charts, we show the Textile Mill and Apparel Manufacturing Producer Price Indexes

(PPIs). PPIs measure the average change over time in selling prices received by domestic producers for

their output.

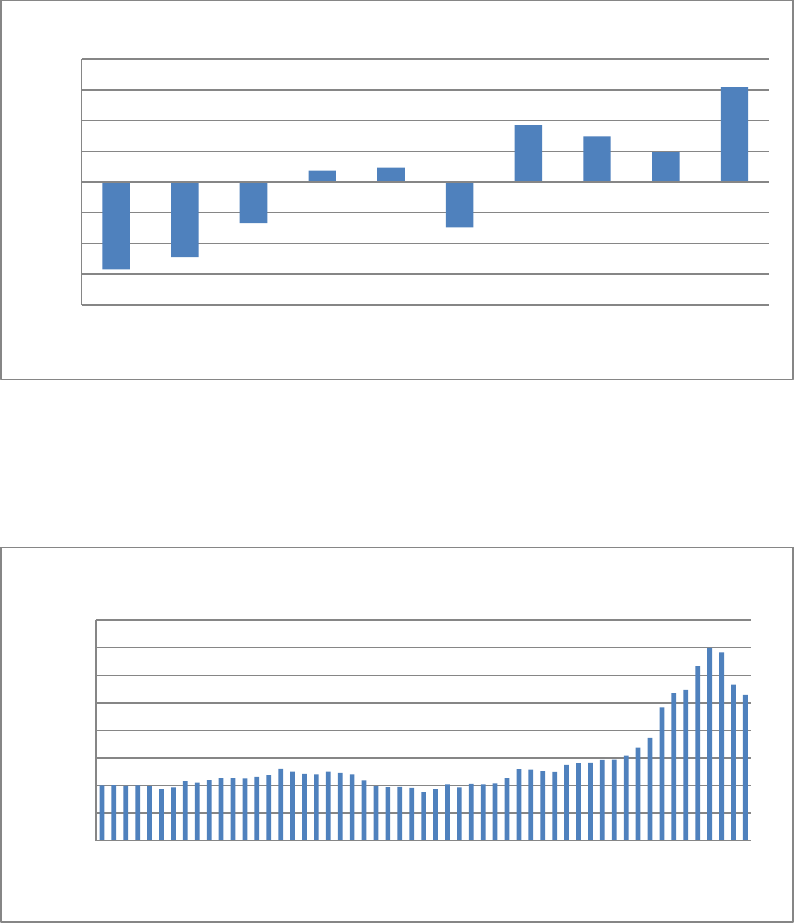

Effects from higher cotton prices can be seen at the textile producer's price level of the value chain.

From 2010 to 2011, Textile Mills increased prices from 115 to over 130 in PPI index terms. A +13%

increase. Previously, increases had been +2% to +3% annually.

See the subsequent chart:

The PPI for Apparel Manufacturers captures the effect of higher labor costs. The year-on-year increase

had been close to +1%. It picked up notably in 2011, most likely from higher labor costs in China. The

PPI for Apparel Manufacturers did not show any change from rising input prices like cotton.

See the subsequent chart:

90

95

100

105

110

115

120

125

130

135

2004

2005

2006

2007

2008

2009

2010

2011

PPI Textile Mills - Shows the Effects of Cotton Prices in 2011

Source: U.S. Dept. of Labor, Bureau of Labor Statistics

LAEDC - Kyser Center P a g e | 22 Fashion Industry Profile 2011

These data show most textile mills are partly passing on cotton and other commodity price increases.

Most apparel manufacturers are passing on a part of rising labor costs to customers too. But some

apparel manufacturers are cutting costs by re-engineering fabric blends, making laces and trims in-

house, and streamlining use of embellishments such as appliqués, bows, beading, and piping. A similar

type of material substitution is likely at some textile mills, using less expensive textiles and trims.

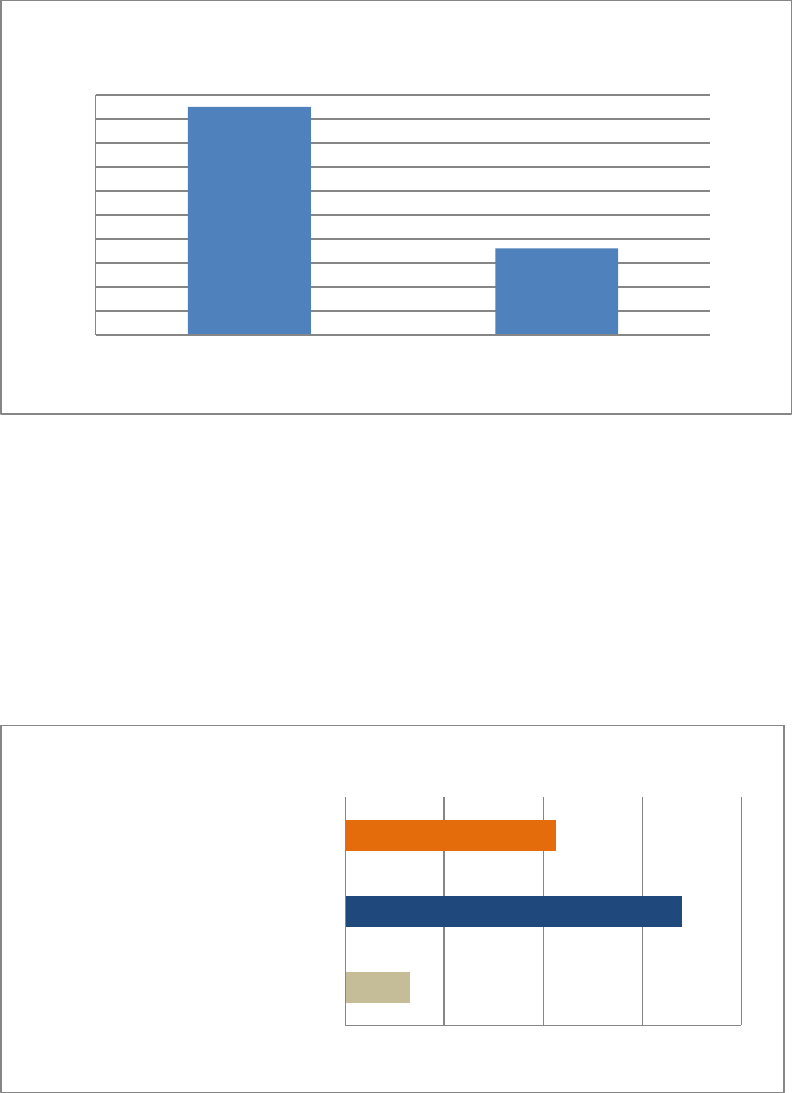

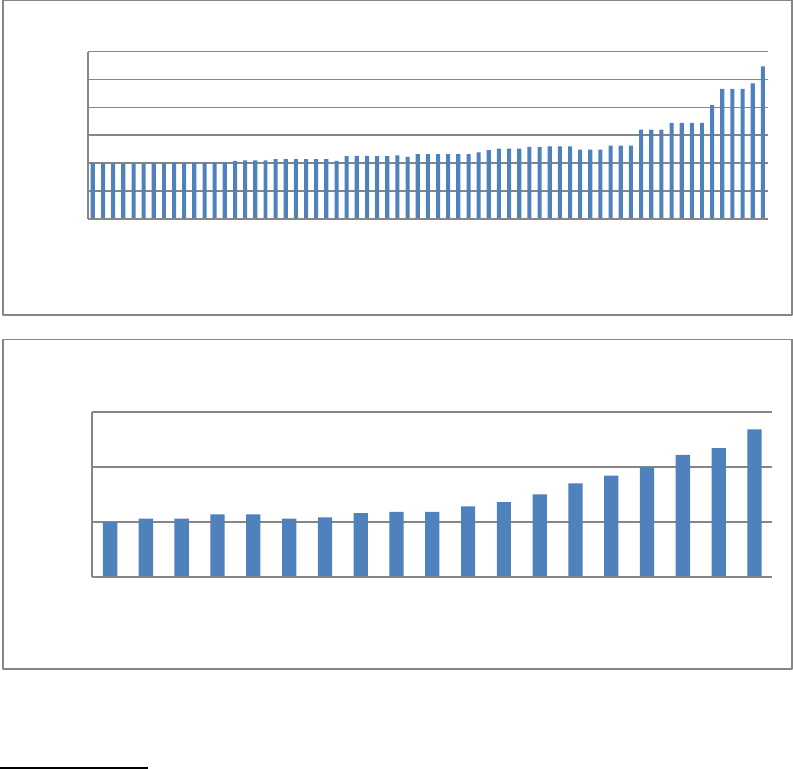

As another subsequent chart shows, the U.S. profit per dollar of sales before income taxes for "Apparel

and Leather Products" rested at 10% in the five quarters up to the end of March 2011. At 10%, the

apparel industry pre-tax profit margin remains close to average U.S. non-durable manufacturing profit

margins. Textile Mills earned a 4% pre-tax margin. In comparison, Computer and Electronic Products

makers earned a 23% pre-tax margin.

At the base of the value chain (apparel manufacturing), the flat quarterly profit profile doesn't show any

effects from higher costs. The effect of rising costs has not been dealt with visibly.

Yet!

96

98

100

102

104

106

2004

2005

2006

2007

2008

2009

2010

2011

PPI Apparel Manufacturing -

Some Evidence of the Pass Through of Material Costs in 2011

Source: U.S. Dept. of Labor, Bureau of Labor Statistics

0

2

4

6

8

10

12

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011

Percentage of Profit Per Dollar of Sales Before Income Taxes -

Apparel and Leather Products are Close to the Overall Mfg. Average

Source: U.S. Census Bureau

LAEDC - Kyser Center P a g e | 23 Fashion Industry Profile 2011

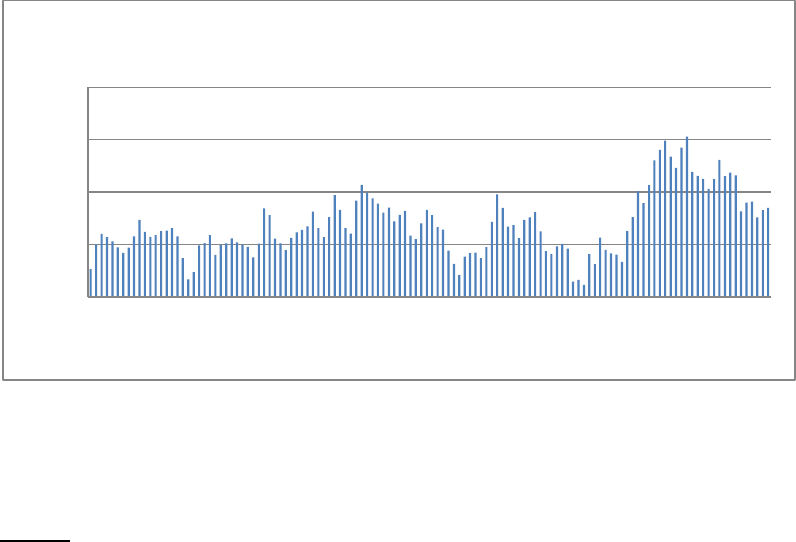

Looking towards the end of the value chain, there was very visible price discounting in women's and

girl's apparel prices at department stores around the peak of the 2008 financial crisis. In 2010, price

rises at department stores recouped some of the 2008 era discounts on offer to move merchandise.

See the subsequent chart to confirm:

Retailers at the end of the value chain are facing down a difficult choice: Between cutting their profit

margins, or passing on price increases to their already stressed customer base. It remains to be seen if

further price increases at retail due to higher cotton prices can be made successfully.

Finance

Revenue for many apparel manufacturers is seasonal, because spring and fall are the prime selling

seasons. Contractors are essentially financed by manufacturers they work for, with partial payments as

shipments are made. Manufacturers often have financing needs for both receivables and inventory.

Payments from large buyers and payments to foreign contractors may be via letters of credit.

The lack of equipment finance is a major issue in Los Angeles. Finance availability keeps modernization

for local manufacturing at bay. Equipment financing needs have decreased in recent years as more

manufacturers use foreign contractors. Due to the loss of the California manufacturer's tax credit in

2003, brand owners are also no longer incentivized to finance new equipment for their contractors.

Overall, apparel in the U.S. remains a challenging business -- net income earned is about 1% of revenues.

It is 0.9% for smaller firms. However, strong entry figures in difficult economic times provide ample

evidence that sizeable returns are available to L.A. based apparel companies with good design ideas,

strong management, and well-crafted business models. In 2009, at the depth of the last downturn, we

had a +6.9% increase in the amount of apparel-making companies registered with the California DLSE.

A breakdown by California county of apparel manufacturing (NAICS 315) and textile mill (NAICS 313)

companies and revenues shows L.A. County and Orange County are clear leaders. Counting all 2011

500

550

600

650

700

2001

2001

2001

2002

2002

2003

2003

2003

2004

2004

2005

2005

2006

2006

2006

2007

2007

2008

2008

2008

2009

2009

2010

2010

2011

2011

Dept. Store Women's and Girl's Accessories Price Index

Evidence of Cooling in Recent Months...

Source: U.S. Dept. of Labor, Bureau of Labor Statistics

LAEDC - Kyser Center P a g e | 24 Fashion Industry Profile 2011

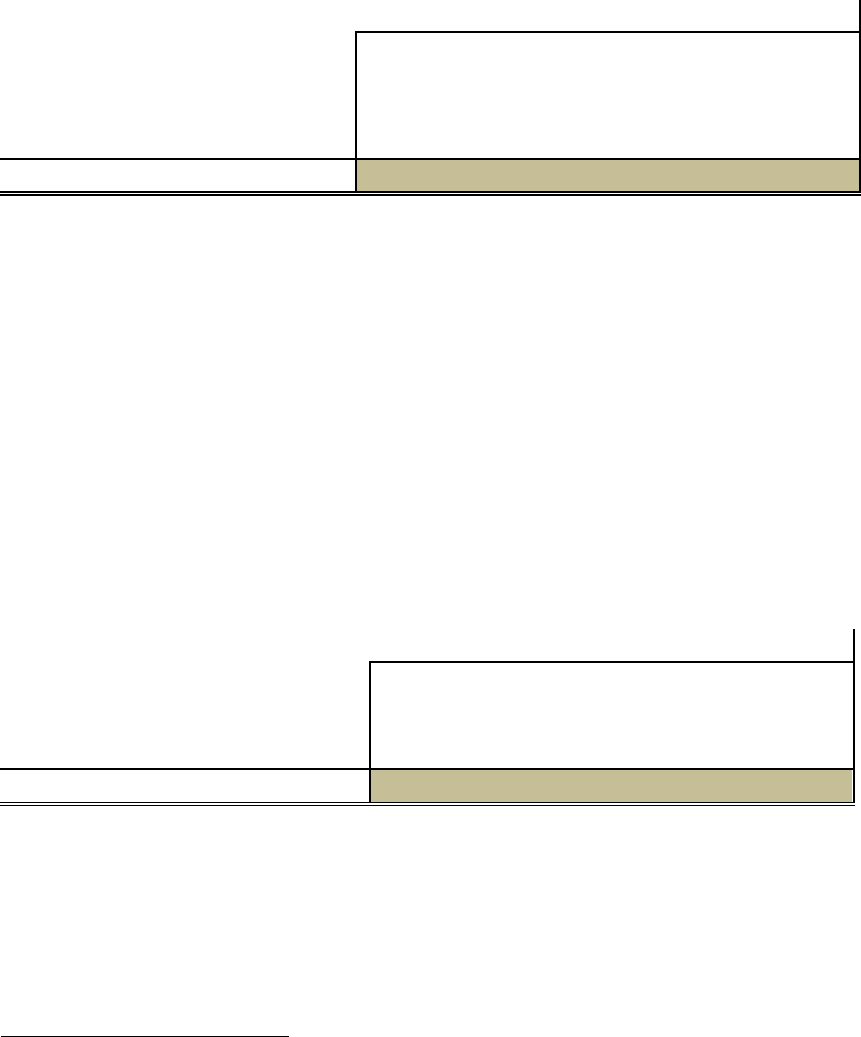

apparel and textiles operations in California, 994 companies earned above $1 million in revenue. Of that

number, L.A. County had 692 companies and Orange County had 96 (summing up to 80% of the total).

See the subsequent table:

Table 1: Companies in California with Revenues of $1 Million and Greater, 2011

Apparel Manufacturing (NAICS 315) and Textile Mills (NAICS 313)

County

Total

Companies

Total

Revenues

($ millions)

Total

Employees

Average

revenues

($ millions)

Average

employees

Los Angeles County

692

$4,882

44,906

$7

65

Orange County

96

$1,256

13,355

$13

139

Riverside County

7

$28

366

$4

52

San Bernardino County

5

$20

280

$4

56

Ventura County

14

$82

1,065

$6

76

Alameda County

19

$1,319

1,465

$69

77

Contra Costa County

6

$33

392

$5

65

El Dorado County

1

$1

20

$1

20

Fresno County

5

$10

90

$2

18

Humboldt County

2

$7

111

$3

56

Imperial County

1

$2

20

$2

20

Kern County

2

$5

39

$3

20

Marin County

2

$5

39

$3

20

Merced County

1

$2

40

$2

40

Monterey County

2

$18

259

$9

130

Napa County

1

$1

4

$1

4

Nevada County

1

$1

2

$1

2

Sacramento County

2

$6

51

$3

26

San Benito County

1

$1

17

$1

17

San Diego County

40

$421

6,453

$11

161

San Francisco County

26

$4,508

17,769

$173

683

San Luis Obispo County

3

$5

58

$2

19

San Mateo County

7

$30

426

$4

61

Santa Barbara County

5

$31

112

$6

22

Santa Clara County

7

$16

125

$2

18

Santa Cruz County

3

$27

102

$9

34

Solano County

1

$3

25

$3

25

Sonoma County

4

$10

111

$3

28

Tuolumne County

1

$1

14

$1

14

Other (Unknown

location)

37

$1,589

13,566

$43

367

Grand Total

994

$14,320

101,282

$14

102

LAEDC - Kyser Center P a g e | 25 Fashion Industry Profile 2011

Note: San Francisco is the home of Levi-Strauss, with revenue of $4.4 Billion.

Source: Hoover's

Dun & Bradstreet data, also captured in 2011, show the amount of financial stress evident among the

apparel wholesalers (4243), the apparel manufacturers (315), and the textile mills (313) in L.A. County.

In 2011, as a result of very competitive market conditions in L.A. County, fully 45% of apparel

wholesalers, apparel manufacturers, and textile mills operate under significant financial stress.

In this industry, 25% of revenues in L.A. County are earned in conditions of financial stress too.

In light of these numbers, a key implication emerges: a small sized firm in L.A. has a greater chance of

operating under conditions of financial stress. Less product and process diversification, lower access to

credit, and other issues appear relevant.

See the table below:

Table 2: Conditions of Financial Stress in L.A. County Apparel Industries, August 2011

Risk

Level

1

2

3

4

5

Unclassified/

Bankrupt

Total

4243 Apparel

Wholesalers

Firms

19

844

1447

1670

143

68

4191

($ millions)

Revenues

$304

$1,436

$2,301

$1,360

$213

$22

$5,635

Risk

Level

1

2

3

4

5

Unclassified/

Bankrupt

Total

313 & 315

Apparel

Manufacturing

Firms

27

455

885

961

138

69

2535

and Textile

Mills

Revenues

$412

$3,619

$1,639

$960

$197

$556

$7,383

Risk

Level

1

2

3

HIGH

RISK/4

HIGHEST

RISK/5

Unclassified/

Bankrupt

4243 Apparel

Wholesalers

Firms

0%

20%

35%

40%

3%

2%

Revenues

5%

25%

41%

24%

4%

0%

313 & 315

Apparel

Manufacturing

Firms

1%

18%

35%

38%

5%

3%

and Textile

Mills

Revenues

6%

49%

22%

13%

3%

8%

Source: Dun & Bradstreet

As the data in both tables show, the L.A. apparel industry is largely small and middle-market companies.

Many are managed by owner-operators. They have a great deal of their own capital invested in their

business. This is one of the driving forces behind why such companies turn to a form of financing called

LAEDC - Kyser Center P a g e | 26 Fashion Industry Profile 2011

factoring. Privately-owned businesses generally do not want to risk additional capital by extending large

amounts of credit to their retail customers.

Factoring is an agreement between a factoring company and the suppliers of goods, typically to the

retail industry. A small, owner-operated apparel manufacturer supplying clothes to a women's dress

retailer is a classic example. The factor purchases the accounts receivable from a supplier (the small

apparel manufacturer in this case) and assumes responsibility for a retailer’s financial inability to pay

(the women's dress retailer in this case). This financing activity combines:

Credit protection and advice.

Accounts receivable bookkeeping, including electronic invoice and payment processing.

Collections, cash management, and lockbox processing.

Accounts receivable financing.

Factoring helps companies of all sizes, from start-ups to mature companies:

Improve cash flow.

Eliminate credit losses.

Reduce operating expenses.

Expand working capital financing through advances.

Improve management information through online reports.

Major international banks focus their marketing efforts for factoring services on the larger apparel firms,

i.e. those above $ 2 million in annual sales. If a firm is smaller than $ 2 million, a smaller, locally-based

factor picks up the business. These smaller, locally-based factors tend to charge much higher

commission rates, due to the greater risks their clients face.

International Trade

The U.S. imports the bulk of apparel sold domestically. In 2010, the U.S. imported $71.4 billion worth of

apparel, with $40.6 billion arriving through the Los Angeles Customs District.

Since most imports come from Asia, a significant portion passes through the Los Angeles Customs

District (LACD), which includes the twin ports of Los Angeles and Long Beach, Port Hueneme, LAX,

Ontario International, and McCarran Field (Las Vegas). Of the top source countries for apparel imports

to the LACD, China was by far the largest with $24.8 billion in 2010 (our definition of "China" includes

Hong Kong and Macau for reasons to be explained in the Foreign Competition section). It is followed by

Vietnam ($4.4 billion), Indonesia ($2.7 billion), Bangladesh ($1.2 billion),Thailand ($760 million),

Philippines ($700 million), India ($620 million), Taiwan ($280 million), and South Korea ($120 million).

In 2004, when we last did this report, China accounted for 1/3 of apparel imports coming through the

L.A. area's seaports and airports. In 2011, China accounted for 2/3 of apparel imports with six times the

dollar value of 2004. Vietnam, Bangladesh, and India did not receive mention in 2004. Now, they stand

as number two, number four, and number six.

LAEDC - Kyser Center P a g e | 27 Fashion Industry Profile 2011

(Note: trade data for the L.A. Customs District do not reflect actual production or consumption in the

SoCal area. It is the most comprehensive data available, and we feel it does provide a good picture of

the overall trend. For L.A.-Canada and L.A.-Mexico trade, however, the data are severely skewed

because much trade passes through border customs districts like San Diego and Seattle. According to

industry insiders, Mexico is the second largest source of L.A.'s apparel imports behind, who else, China).

For textiles (not textile products such as carpets, rugs, etc.), China was also the largest source of imports

at $687 million (out of a total of $1.7 billion in textile imports to the LACD), followed by South Korea

($297 million), Taiwan ($172 million), Japan ($121 million), Indonesia ($91 million) and India ($78

million). Italy ($51 million) was the first European country to reach the top textile import list.

See the table below:

Table 3: Los Angeles Customs District, Textile and Apparel Imports in 2010

Country

Total

Textiles

Apparel

($ Value)

($ Value)

($ Value)

World

40,595,746,183

1,656,551,261

38,939,194,922

China

25,477,525,781

686,840,071

24,790,685,710

Vietnam

4,421,128,517

27,565,293

4,393,563,224

Indonesia

2,816,255,708

91,492,316

2,724,763,392

Bangladesh

1,190,147,379

145,084

1,190,002,295

Thailand

803,662,413

44,028,732

759,633,681

India

707,044,559

78,058,578

628,985,981

Philippines

698,329,905

1,171,788

697,158,117

Taiwan

451,559,679

172,090,837

279,468,842

South Korea

417,602,893

297,102,849

120,500,044

Japan

127,369,986

121,034,086

6,335,900

Hong Kong

94,953,193

3,208,088

91,745,105

Macau

36,188,562

36,188,562

Singapore

35,590,786

66,572

35,524,214

Asia

37,277,359,361

1,522,804,294

35,754,555,067

92%

92%

92%

Source: USATradeonline.gov

Textiles: 50 (Silk, Including Yarn), 51 (Wool and Animal Hair), 52 (Cotton, Including Yarn), 54 (Manmade Filament), 55 (Manmade Staple

Fiber), 58 (Spec. Wov Fabric), 60 (Knitted or Crochet)

Apparel: 61 (Apparel Articles and Accessories, Knit or Crochet), 62 (Apparel Articles, Not Knit), 64 (Footwear, Gaiters)

A stark difference exists between these two lists. Top apparel importers are very low wage countries. In

comparison, textile making is both capital and technology intensive. So, top textile importers are higher

wage, higher education, and more developed Asian economies. Driving home this point, the list of top

LAEDC - Kyser Center P a g e | 28 Fashion Industry Profile 2011

textile importers includes the wealthy country of Italy. Italy has a strong tradition of making textiles.

Comparing the two lists suggests Asia is now two regions within itself -- a poor, lesser developed one --

and a well developed one much like Italy.

Top consumers of L.A. apparel exports (a total of $870 million in 2010) were Japan ($178 million) , China

($97 million), South Korea ($92 million), the United Kingdom ($64 million), Belgium ($55 million), and

Australia ($41 million). A large portion of U.S. exports are shipped by air, a sign these are often high-

value, time-sensitive merchandise. What's being exported? Anything from swimwear to designer

dresses to Dodger's shirts.

U.S. exports of textiles ($3.16 billion in 2010) may return to the U.S. after a few weeks as finished

products. China was the number one destination in 2010 at $1.78 billion, followed by Indonesia ($238

million), Vietnam ($191 million), South Korea ($160 million), and Taiwan ($112 million). Interestingly,

the 2010 list includes the telling supra-low wage destinations of Bangladesh ($75 million), Guatemala