0

CONSUMER FINANCIAL PROTECTION BUREAU | APRIL 2020

The

Early Effects of the

COVID

-19 Pandemic on

Credit

Applications

CFPB Office of Research

Special Issue Brief

1 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

1. Introduction

This report uses the Consumer Financial Protection Bureau’s Consumer Credit Panel (CCP) to

examine the early effects of the COVID-19 pandemic on credit applications as measured by the

number of credit inquiries in credit records.

1

The Bureau received the March 2020 data file in

early April. The data file includes information on inquiries up through a few days before the end

of March. We analyzed these data and present findings in this report.

The focus of this report is on inquiries because they are among the first credit market measures

to change in credit record data in response to changes in economic activity. When a consumer

applies for new credit to purchase a car or a home or for a new credit card account, most lenders

will seek information about the consumer from a nationwide consumer reporting agency. This is

often referred to as a “hard inquiry.” Inquiries typically appear almost immediately in credit

record data when a consumer’s credit report is pulled.

2

Other credit market measures, such as

delinquencies or forbearances on existing accounts, are generally less quickly observed since

information on existing accounts is reported with some lag.

We compare hard inquiry volume in the last week of March with that in the first week and adjust

for within-month trends based on data from the March CCP in earlier years (2013–2019). We

find that auto loan inquiries dropped by 52 percent between the first and last week of March,

new mortgage inquiries dropped by 27 percent, and revolving credit card inquiries declined by

40 percent. Additionally, the drops are significantly more pronounced for consumers with

higher credit scores. For auto loan inquiries, consumers with deep subprime scores (those with a

Vantage credit score below 500) experienced a 49 percent drop in inquiries while consumers

with super prime scores (those with a Vantage credit score above 780) experienced a 67 percent

drop. The relative differences are even larger for revolving credit card inquiries (34 percent drop

vs. 59 percent drop for the same two groups) and new mortgage inquiries (20 percent drop vs.

36 percent drop for the same two groups).

The observed drop in inquiries could be due to a drop in underlying credit demand, a drop in

credit supply affecting inquiries either directly or indirectly by heightening consumers’

1

Report prepared by Éva Nagypál, Ph.D, Christa Gibbs, Ph.D., and Scott Fulford, Ph.D. in the Office of Research.

2

One indication of inquiries appearing almost immediately is the very small number of inquiries that appear with

delay. For example, 0.06 percent of auto loan inquiries with an inquiry date falling on dates covered by the March

2019 file were reported first in the April 2019 file. For more information on how inquiries have evolved over time,

see the Bureau’s Consumer Credit Trends Inquiry Index:

https://www.consumerfinance.gov/data-

research/consumer-credit-trends/mortgages/inquiry-activity/.

2 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

expectation of being turned down for credit, or a lack of opportunity for car and home sales to

take place due to physical restrictions on movement and economic activity.

3

Regardless of the

reason, the data indicate all types of inquiries dropped significantly and that consumers with

higher credit scores have more flexibility in substituting away from applying for credit than

consumers with lower credit scores.

4

We also find significant geographic variation in the decline in inquiries, with states in the South

and Mountain regions experiencing smaller drops and the Northeast and California

experiencing the largest drops. We relate these drops to the case rate (number of COVID-19

cases per 100,000 residents) in each state by the end of our data. We find that the case rate is

strongly negatively correlated with the drop in auto loan and new mortgage inquiries with a

correlation coefficient of -0.47 and -0.53, respectively. In other words, states with a higher case

rate experienced a larger drop in auto loan and new mortgage inquiries. We do not find much of

a correlation—positive or negative—between revolving credit card inquiries and the case rate.

We also relate the drops in inquiries to the unemployment insurance (UI) claims share (i.e., the

share of covered workers who submitted unemployment insurance claims) during the last two

weeks of March in each state. We find that the UI claims share is strongly negatively correlated

with the drop in auto loan inquiries with a correlation coefficient of -0.60. This means that

states with a higher UI claims share experienced a larger drop in auto loan inquiries. The

correlation is weaker for new mortgage or revolving credit card inquiries at -0.37 and -0.18,

respectively. These results indicate that divergent forces may be driving the drop in inquiries for

different credit products.

3

There may be some similarities between the economic consequences of the COVID-19 pandemic and those of a

natural disaster, without the destruction of property. For more on the impact of natural disasters on credit

reporting, see: Daniel Banko-Ferran and Judith Ricks. 2018. Natural Disasters and Credit Reporting. November

2018 Quarterly Consumer Credit Trends.

https://files.consumerfinance.gov/f/documents/bcfp_quarterly-

consumer-credit-trends_report_2018-11_natural-disaster-reporting.pdf.

4

This flexibility is evident in the timing of applications as well. While credit scores are relatively stable for many

consumers, others experience large increases or decreases in their scores. Consumers are more likely to apply for a

general purpose credit card when their credit score is close to its maximum. On the other hand, the number of credit

card inquiries per person decreases sharply as credit scores reach their minimum. See: Ryan Sandler and Anita

Chen. 2019. Timing of Applications for Consumer Credit. May 2019 Quarterly Consumer Credit Trends.

https://files.consumerfinance.gov/f/documents/cfpb_consumer-credit-trends_timing-applications-consumer-

credit_2019-05.pdf.

3 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

2. Data

The CCP is a longitudinal, nationally representative 1-in-48 sample of de-identified credit

records from one of the three nationwide consumer reporting agencies. The sample includes

approximately five million credit records representing the universe of approximately 240

million credit records. After the end of each month, the CFPB receives updated credit records for

all sampled credit records, if available.

The records include information about the credit accounts included in each consumer’s credit

record (such as auto loans, mortgages, credit cards, student loans, and other bank installment

loans). Also included is information about any credit record inquiries made by lenders in

response to an application for credit, and details on non-credit-related debts. In addition, the

CFPB receives de-identified information on the borrowers in the panel on a quarterly basis,

including geography (census tract), credit score, and birth year information.

This report focuses on inquiries, since those are among the first measures to change in credit

record data in response to changes in economic activity. Specifically, we focus on hard inquiries

for auto loans, new mortgages,

5

revolving credit cards, and inquiries that either fall into smaller

categories

6

or do not contain enough information to determine their exact nature (unspecified

and other inquiries).

7

These four types of inquiries made up 86.5 percent of all inquiries in the

month of March in 2013 through 2019.

8

5

A mortgage inquiry is categorized as new if the consumer does not have an open mortgage tradeline already. These

inquiries are likely to correspond to purchase mortgage inquiries, though they do not capture all purchase

mortgages since many home purchases are by people who hold a mortgage on their existing home. The rest of

mortgage inquiries are categorized as replacement. These include refinances that are not well-suited to be studied

with the methodology of this report, since they are primarily driven by interest rate movements, even within a

month. In fact, there was a large boom in replacement mortgage inquiries, especially among consumers with high

credit scores, in the first week of March. There were close to 20,000 inquiries for consumers with prime and super

prime scores in the first week of March 2020, compared to around 6,500 per week during the month of March in

2013 through 2019. By the fourth week of March, the number of weekly inquiries for this group moderated to

around 12,000, which was still well above the previous years’ average March weekly number.

6

These include personal installment and revolving loans, and some other small categories.

7

These are inquiries where there is not enough information in the credit record to determine the type of inquiry. For

example, the most common combinations that are categorized as unspecified have an unknown account type and

have a business category related to unspecific banking or finance.

8

Replacement mortgage inquiries make up another 7.3 percent. The remaining 6.1 percent of inquiries are made up

of student loan inquiries, of which there are very few in March, business loan inquiries, collection inquiries, and

inquiries not related to credit extension, such as for the purpose of screening tenants.

4 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

3. The Early Effects of the

Pandemic on Inquiries

The March CCP data files include inquiries up through a few days before the end of March, with

inquiries for the last day being only partly covered. Since inquiries vary within the week (most

notably there are few inquiries on Sundays), we construct a weekly count of inquiries by inquiry

category, defining the week in such a way that allows us to use the largest span of the data. In

addition to the within-week patterns, inquiries also show strong within-month patterns that

vary by category and by the type of consumer considered. For example, as shown in detail in the

Appendix, consumers with deep subprime scores tend to have more auto loan inquires at the

beginning of March while consumers with super prime scores tend to have more auto loan

inquires at the end of the month. To account for these patterns and to examine how the volume

of inquiries was affected by inquiry category and consumers considered, we adopt the following

approach.

We construct the change in inquiries by inquiry category and by consumer group for each week

of the month using the first week of the month as the baseline. To get at the effect of COVID-19,

we assume that, without the pandemic, week-to-week proportional changes in inquiries in

March 2020 (relative to the first week of March) would have been the same as the average week-

to-week changes in inquiries in the month of March in 2013 through 2019. The Appendix

contains further mathematical details.

Figure 1: Percentage change in credit inquiries relative to the first week of March

2020 by week by inquiry category

5 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

We start by considering all consumers together. As shown in Figure 1, the volume of inquiries

declined in all categories, and the decline was gradual and pronounced. The drop was the largest

among auto loan inquiries and smallest among new mortgage inquiries (which did not start

declining appreciably until week 3). By the last week of March, by which point a good part of the

country was under stay-at-home orders, auto loan inquiries dropped by 52.4 percent,

9

new

mortgage inquiries by 26.9 percent,

10

revolving credit card inquiries by 39.7 percent,

11

and

unspecified and other inquiries by 34.6 percent.

12

While some of the underlying mechanisms contributing to these declines are probably the same

across the inquiry categories, there are likely important differences, too. On the demand side,

the pandemic led to a surge in unemployment and an increase in economic uncertainty. These

forces likely reduced the demand for credit tied to the purchase of durable goods (e.g., cars and

homes), which are expenses that often can be deferred.

13

At the same time, the pandemic may

have had offsetting effects on the demand for revolving credit cards since transaction demand

likely decreased while the demand for the possibility to borrow likely increased. As miles

traveled declined due to social distancing measures and stay-at-home orders, the demand for

cars was likely further reduced, possibly explaining why this category saw the largest decline. In

addition, car and home purchases typically have a strong in-person component, making online

purchases less attractive even if available. One possible explanation for the lower decline in

home purchases is that such purchases take longer to execute, and inquiries in March may be

partly reflecting decisions to purchase a new home prior to the onset of the pandemic.

14

9

According to Autodata Corporation, new vehicle sales dropped by 33 percent between February and March 2020.

No weekly statistics are provided. See http://www.motorintelligence.com/

.

10

According to the National Association of Realtors, sales of existing homes dropped by 8.5 percent between

February and March 2020. No weekly statistics are provided. See

https://www.nar.realtor/research-and-

statistics/housing-statistics/existing-home-sales.

11

Retail revolving credit cards made up 20 percent of inquiries within the revolving credit card category in the month

of March in 2013 through 2019. Not surprisingly, the drop in the number of these inquiries in March 2020 was

significantly larger at 70 percent than the drop among general purpose credit cards at 33 percent.

12

The downward pattern observed in this group indicates that the general pattern of a decrease in credit inquiries

observed for the specific products (that make up 61.4 percent of inquiries) also holds more broadly for this group

(that makes up 25.4 percent of inquiries).

13

By delaying durable goods purchases, consumers can help smooth consumption. Research suggests that the

precipitous decline in car purchases during the Great Recession is largely explained through this timing of car

purchases dimension (see Bill Dupor, Rong Li, Saif Mehkari, and Yi-Chan Tsai. 2018. The 2008 U.S. Auto Market

Collapse. Federal Reserve Bank of St. Louis Research Division Working Paper 2019-019A.

https://doi.org/10.20955/wp.2018.019).

14

For mortgage loans, there is also the consideration that a lender may pull the credit report of the consumer several

times during the underwriting process and prior to the consummation of the loan.

6 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

At the same time, the supply of credit was likely reduced as the pandemic lowered lenders’

perceptions of consumers’ creditworthiness. This may have been less pronounced for

collateralized loans, though the larger size of these loans may be a countervailing factor.

Next, we examine the drop in more detail by credit score. We use a Vantage credit score

15

as our

measure of a consumer’s creditworthiness and define credit score groups as deep subprime

(score below 5oo), subprime (score between 500 and 600), near prime (score between 601 and

660), prime (score between 661 and 780), and super prime (score above 780).

16

The distribution

of consumers and inquiries across these groups is shown in the Appendix.

Figure 2: Percentage change in auto loan inquiries relative to the first week of March

2020 by week by credit score group

Figure 2 shows the percentage change in auto loan inquiries by week across the above credit

score groups relative to the first week of March 2020. According to the figure, by the last week of

March, the decline exceeded 67 percent for consumers with super prime scores while it was 47.3

percent for consumers with near prime scores (the group with the smallest decline). These

patterns may be explained by consumers with super prime scores having more flexibility in

forgoing a credit application than consumers with near prime scores (perhaps due to such

consumers owning more cars and cars in better shape, having access to alternative forms of

credit, or having more of an opportunity to work from home, etc.).

15

We use VantageScore 3.0.

16

https://www.thebalance.com/fico-score-vs-vantagescore-961144.

7 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

Figure 3: Percentage change in new mortgage inquiries relative to the first week of March

2020 by week by credit score group

Figure 3 shows the percentage change in new mortgage inquiries by credit score group for the

last three weeks in March 2020 relative to the first week. By the last week, the relative patterns

are like those seen for auto loan inquiries: the super prime group saw the largest drop at 36.2

percent, while the deep subprime group saw a drop barely half in size, at 19.8 percent Again,

these differences likely reflect differences in demand responses as supply considerations are

unlikely to have more adverse effects on consumers with super prime scores.

8 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

Figure 4: Percentage change in revolving credit card inquiries relative to the first week of

March 2020 by week by credit score group

Figure 4 shows the percentage change in revolving credit card inquiries by credit score group for

the last three weeks in March 2020 relative to the first week. The patterns are broadly like those

seen for auto loans, with more pronounced differences for consumers with super prime scores

versus other consumers. The sharp drop in revolving credit card inquiries for consumers with

super prime scores may reflect the fact that most of this group’s revolving credit card demand

can be attributed to transactional demand.

17,18

17

See: Grodzicki, Daniel and Sergei Kulaev. 2019. Data Point: Credit Card Revolvers.

https://files.consumerfinance.gov/f/documents/bcfp_data-point_credit-card-revolvers.pdf.

18

In addition to the analysis by credit score group, we also conducted analysis by age (not shown). The patterns are

qualitatively similar for auto loan and revolving credit card inquiries. For instance, by the fourth week of March,

auto loan inquiries dropped 13 percentage points more for those 62 and older than for those under 30. While these

age groups do not fully align with the score groups discussed above, credit score is positively correlated with age.

New mortgage inquiries show a different pattern, however, with larger drops for consumers age 30-61 than for

younger or older applicants.

9 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

4. Geographical Variation

Next, we present evidence on the variation in the within-March decline in inquiries across the

states. Figure 5 shows the percentage change in auto loan inquiries between the first and last

week of March 2020 for states that have a large enough population.

19

Figure 5: Percentage change in auto loan inquiries between the first and last week of

March 2020 by state

Though all states experienced a drop, there is clearly substantial variation in the percentage

change in auto loan inquiries. States in the Northeast and California, together with Michigan

and Nevada, experienced the largest drops. Mississippi, Kansas, Oregon, and the Mountain

states of Utah and Idaho experienced more modest declines.

20

19

Since we are relying on differences in weekly inquiries and normalizing by using the same difference in prior years

(2013-2019), our measure requires a considerable number of inquiries to be accurately measured. For this reason,

in all our state level analyses of auto loans and revolving credit card inquiries, we restrict attention to the 39 states

that had a population of at least 1.5 million people. For the state level analyses of new mortgage inquiries, we set the

population threshold at 5 million people due to the lower frequency of these inquiries, resulting in 23 states (not

mapped). Neither Alaska nor Hawaii, not shown on the map, rise above these population thresholds.

20

Other than for mortgages, not all lenders conduct an inquiry with each of the three nationwide consumer reporting

companies for every loan. Which consumer reporting agency lenders choose may vary along several dimensions,

10 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

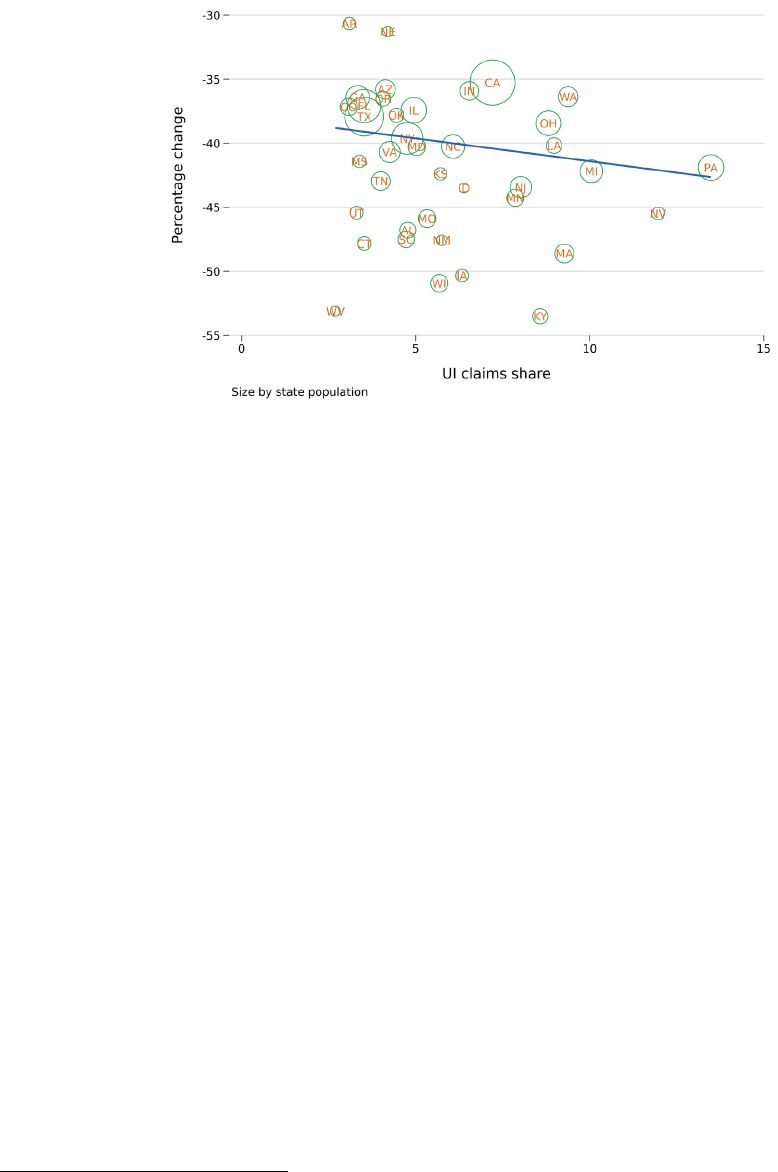

Figure 6 relates the changes in auto loan inquiries to the state level case rate, defined as the

number of COVID-19 cases per 100,000 residents as of the end of our data.

21

Figure 7, in turn,

relates the changes in auto loan inquiries to the state UI claims share, defined as the share of

covered workers who submitted unemployment insurance claims in the state during the last two

weeks of March.

22,23

Figure 6: Percentage change in auto loan inquiries between the first and last week of

March 2020 versus the number of cases per 100,000 residents by state

The plots show a fitted line using population weights and show circles around the state name

proportional to population size. The plots include Alaska and Hawaii as well the low-population

including geography. However, by examining changes between the first and last week of March, the analysis

controls for any differences in coverage if they are constant within the month.

21

Data on the number of cases and deaths are from the New York Times Github repository

(https://raw.githubusercontent.com/nytimes/covid-19-data/master/us-counties.csv). Cases and deaths are the sum

of county level case and death counts by state reported as of the day the CCP was updated at the end of March.

Population estimates are from the Census Bureau. (

https://www.census.gov/data/datasets/time-

series/demo/popest/2010s-national-total.html#par_textimage_1810472256 using dataset Annual Estimates of the

Resident Population for the United States, Regions, States, and Puerto Rico: April 1, 2010 to July 1, 2019 (NST-

EST2019-01). Data on case rates are known to have several shortcomings including differences in reporting criteria

and testing rates across states, but they are closely tracked and influence government responses to the coronavirus

pandemic.

22

Data on unemployment insurance claims and covered employment have been downloaded from

https://oui.doleta.gov/unemploy/claims.asp

.

23

We focus on the case rate and the UI claims share because they are widely cited measures of the pandemic’s effect

and they show significant correlation with the change in inquiries for at least some inquiry categories.

11 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

states excluded from the maps. By showing each state separately and proportional to

population, the variation among states is evident.

Figure 7: Percentage change in auto loan inquiries between the first and last week of

March 2020 versus the share of covered workers who submitted unemployment

insurance claims during the last two weeks of March by state

Clearly, the drop in auto loan inquiries is strongly correlated with both a state’s case rate and its

UI claims share.

24,25

This likely reflects several underlying mechanisms. The case rate may be a

good measure for the perceived increase in economic uncertainty and for the reduced

transportation demand as residents started practicing social distancing measures, predictors of

auto loan demand discussed above. The perceived increase in economic uncertainty may also be

a predictor of the size of supply side responses as lenders lower their perception of consumers’

creditworthiness. The UI claims share is a good indicator of the prevalence of negative income

shocks that also reduce the demand for cars. There are, of course, important deviations from the

overall trends. For example, Pennsylvania, unlike neighboring states, did not initially allow

24

As is clear from Figure 6, New York is an outlier in cases. A multivariate regression of the state level percentage

drop in auto loan inquiries on the log case rate and the UI claims share explains 52.7 percent of the variation in the

percentage drop. Excluding New York lowers percent of variation explained to 50.3 percent, but both explanatory

variables remain statistically significant.

25

Depending on the exact specification, the share of a state’s population that is estimated to be staying home based

on location data is also a significant predictor of the state level drop in auto loan inquiries. In contrast, the date of

restaurant closures and the number of days spent under a stay-at-home order by the end of our data do not provide

added explanatory power.

12 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

online sales of cars.

26

This restriction likely explains why Pennsylvania is below the fitted line

with the largest drop in auto loan inquiries.

Figures 8 and 9 show how the percentage change in new mortgage inquiries between the first

and last week of March across states is related to the state level case rate and UI claims share.

The correlation with the case rate is similar to the one with auto loan inquiries.

27

The

underlying mechanisms are likely similar to those for auto loans.

Figure 8: Percentage change in new mortgage inquiries between the first and last week

of March 2020 versus the number of cases per 100,000 residents by state

The relationship with the UI claims share is somewhat negative. One possible reason for the

weaker correlation than for auto loans could be the fact that workers affected by the layoffs

26

Prior to the pandemic, Pennsylvania required a notary public signature for car sales, effectively making online-only

sales impossible. See:

https://www.post-gazette.com/business/career-workplace/2020/04/14/car-dealerships-

nonessential-non-life-sustaining-businesses-Pennsylvania-coronavirus-COVID19/stories/202004130113. Recent

legislation allows some notary services online, allowing online car sales:

https://philadelphia.cbslocal.com/2020/04/20/coronavirus-pennsylvania-gov-wolf-to-ease-restrictions-on-

construction-vehicle-sales/.

27

A multivariate regression of the state level percentage drop in new mortgage inquiries on the log case rate and the

UI claims share explains 33.3 percent of the variation in the percentage drop. Excluding New York lowers percent of

variation explained to 25.7 percent with the log case rate becoming statistically insignificant at the 90 percent level

of confidence. The drop in new mortgage inquiries at the state level seems to be also related to the date of restaurant

closures, the number of days spent under a stay-at-home order by the end of March, and the share of a state’s

population that is estimated to be staying home based on location data. It should be kept in mind that we are only

analyzing 23 states with a population over 5 million people, however, so statistical relationships are tenuous.

13 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

during the first few weeks of the pandemic were primarily in low-wage food service and

personal care occupations, and low-wage workers are likely to be renters.

28

Another possible

reason is the already noted lengthy nature of the home-buying process.

Figure 9: Percentage change in new mortgage inquiries between the first and last week

of March 2020 versus the share of covered workers who submitted unemployment

insurance claims during the last two weeks of March by state

28

Based on occupation-level data available from Washington state at

https://esd.wa.gov/labormarketinfo/unemployment-insurance-data and Occupational Employment Statistics

available at https://www.bls.gov/oes/home.htm.

14 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

Finally, Figures 10 through 12 correspond to revolving credit cards.

Figure 10: Percentage change in revolving credit card inquiries between the first and

last week of March 2020 by state

Here, there is no correlation with the case rate, and the relationship with the UI claims share is

less strong than for auto loan or new mortgage inquiries.

29

Figure 11: Percentage change in revolving credit card inquiries between the first and

last week of March 2020 versus the number of cases per 100,000 residents by state

29

Neither the log case rate nor the UI claims share is a statistically significant predictor of the state level percentage

drop in new revolving credit card inquiries in a multivariate regression framework.

15 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

Figure 12: Percentage change in revolving credit card inquiries between the first and

last week of March 2020 versus the share of covered workers who submitted

unemployment insurance claims during the last two weeks of March by state

Since it is possible to apply for most revolving credit cards online, social distancing is not

necessarily as limiting as it is for auto loans and mortgages, except for certain retail-specific

cards.

30

In addition, the effect of a surge in unemployment and of increased economic

uncertainty on the demand for revolving credit cards is less clear-cut since the demand for these

cards is not tied to the purchase of a durable good. Demand may have fallen less than for auto

loans and new mortgages, but it is likely that, due to the unsecured nature of revolving credit

cards, supply reductions are more pronounced. Due to the nature of the credit card market,

however, these supply considerations may affect the national market and may not have a strong

state specific component.

30

As noted earlier, only a small share of the revolving credit card inquiries correspond to revolving retail credit card

inquiries, and there are not enough of these inquiries in our data to allow for state level analysis.

16 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

5. Appendix

Distribution of consumers and inquiries across credit score groups in the CCP data in the

month of March in 2013 through 2019

Credit score group

Missing

Deep subprime

Subprime Near prime Prime Super prime

Consumers

4.0% 4.5% 20.5% 13.0% 34.2% 23.8%

March inquiries

2.3% 7.7% 28.6% 19.3% 30.0% 12.1%

Our change in inquiry measure

Here, we describe our change in inquiry measure mathematically. Let be a subset of inquiries

defined by inquiry category (e.g., auto loan inquiries), group of consumers (e.g., all consumers

or consumers with deep subprime credit scores), or geography. Let = 2,3,4 be the t

th

week in

March. Then we are looking to measure the relative change:

=

,

,

,

,

where

,

is the expected number of inquiries in 2020 for the given subset for the t

th

week

given the observed changes in 2013 through 2019, defined as:

,

=

,

,

,

,

where

,

is the number of inquiries in years y for the given subset during week t.

Within month variation in inquiries

To demonstrate the within-month variation in the number of inquiries, Figure A1 shows the

percentage change in inquiries for the second through fourth weeks of March relative to the first

week of March for auto loans using data from 2013 through 2019 by credit score group. As can

be seen from the figure, consumers with deep subprime scores have their highest number of

inquiries during the first week and their number of inquiries in subsequent weeks is declining.

By the fourth week, their number of inquiries is eight percent lower than in the first week. On

the contrary, consumers with super prime scores have their lowest number of inquiries during

17 THE EARLY EFFECTS OF COVID-19 PANDEMIC ON CREDIT APPLICATIONS

the first week and their number of inquiries in subsequent weeks is increasing. Their number of

inquiries is 33 percent higher by the fourth week.

Figure A1: Percentage change in auto loan inquiries relative to first week of March by

credit score group, 2013-2019 average

Figure A2 shows the same relationship for revolving credit card inquiries. These types of

inquiries do not show a pronounced within-month pattern.

Figure A2: Percentage change in revolving credit card inquiries relative to first week of

March by credit score group, 2013-2019 average