Funding by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) under

Germany´s Excellence Strategy – EXC 2126/1– 390838866 is gratefully acknowledged.

www.econtribute.de

ECONtribute

Discussion Paper No. 212

November 2022

Francisco Amaral Martin Dohmen

Sebastian Kohl Moritz Schularick

Interest Rates and the Spatial Polarization of

Housing Markets

Funding by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) under

Germany’s Excellence Strategy – EXC 2126/1-390838866 is gratefully acknowledged.

Interest rates and the spatial polarization of

housing markets

*

Francisco Amaral, Martin Dohmen, Sebastian Kohl, and Moritz Schularick

†

November 29, 2022

Abstract

Rising within-country differences in house values are a much debated trend in

the U.S. and internationally. Using new long-run regional data for 15 advanced

economies, we first show that standard explanations linking growing price dispersion

to rent dispersion are contradicted by an important stylized fact: rent dispersion

has increased far less than price dispersion. We then propose a new explanation: a

uniform decline in real risk-free interest rates can have heterogeneous spatial effects

on house values. Falling real safe rates disproportionately push up prices in large

agglomerations where initial rent-price ratios are low, leading to housing market

polarization on the national level.

Keywords: House prices, regional housing markets, spatial polarization

JEL codes: G10, G12, G51, R30

*

This work is part of a larger project supported by the European Research Council Grant (ERC-

2017-COG 772332). We thank Gabriel Ahlfeldt, Benjamin Born, Andrea Eisfeldt, Arpit Gupta, Dmitry

Kuvshinov, Andrea Modena, Amine Ouazad, Marco Pagano, Francisco Queir

´

os and the participants at

the ”The Socioeconomics of Housing and Finance” workshop in Berlin and at the ”ECHOPPE Housing

Conference” in Toulouse for helpful feedback. The project also received support from the Deutsche

Forschungsgemeinschaft (DFG) under Germany’s Excellence Strategy – EXC 2126/1 – 390838866.

†

Amaral: Macro Finance Lab, University of Bonn,

francisco.amaral@uni-bonn.de

; Dohmen: Macro

Finance Lab, University of Bonn,

mdohmen@uni-bonn.de

; Kohl: Free University Berlin,

;

Schularick: University of Bonn and Sciences Po Paris, schularick@uni-bonn.de.

1

1 Introduction

In 1980, the median home in Scranton, PA, was worth more than half the median

home in New York City. By 2018, its value had decreased to one fifth of the New

York City home according to U.S. Census data. In the U.S. and internationally, there

has been a substantial increase in regional housing price differences since the 1980s

(Van Nieuwerburgh and Weill, 2010; Hilber and Mense, 2021). The spatial structure

of economic activity has changed considerably across countries in recent decades. A

prominent trend is increasing social and spatial polarization among different sub-

national housing markets. As housing is the most important asset for most households,

the increasing dispersion of housing prices and housing wealth have become the subject

of intense public debate.

1

From an economic point of view, rising price dispersion across segmented housing

markets could increase spatial misallocation of labor as productive workers are forced

to stay in places where housing is still affordable. For instance, Hsieh and Moretti (2019)

estimate that such misallocation slowed down the growth rate of U.S. GDP by one third

in past decades. An increase in local housing prices has also been shown to lead to

more misallocation of capital (Herkenhoff, Ohanian, and Prescott, 2018), to affect local

non-tradable employment (Mian and Sufi, 2014) and demand conditions (Mian and

Sufi, 2011; Mian, Rao, and Sufi, 2013; Guren et al., 2020), as well as consumer prices

(Stroebel and Vavra, 2019).

Why have housing prices risen more in some locations than in others? In the most

parsimonious framework, rental cash flows determine the value of housing assets: the

price of a house is equivalent to the discounted expected future rental cash flow it

generates (Poterba, 1984). An important implication – and the starting point for most

existing explanations of growing housing price dispersion – is that price and rent

dispersion should evolve in lockstep. Yet, as we will show, this approach is at odds

with an important stylized fact: rent dispersion has increased considerably less than

price dispersion in recent decades, both in the U.S. and internationally. Existing studies

that model housing price dispersion as a function of growing differences in local rents

(

e.g.

; Van Nieuwerburgh and Weill, 2010; Gyourko, Mayer, and Sinai, 2013) typically

overestimate changes in rent dispersion by a substantial margin.

We use a novel long-run data set of housing prices and rents for 27 major agglomera-

tions in 15 developed countries as well as long-run data covering the entire cross-section

of U.S. MSAs, and show that price–rent ratios in large agglomerations have increased

about twice as much as the national average since the 1980s. Moreover, new research

1

For instance, existing homeowners in high price urban areas have an incentive to restrict urban growth

to the detriment of new buyers (Ortalo-Magn

´

e and Prat, 2014). The increasing polarization of housing

wealth may have also contributed to political polarization at the national level (Adler and Ansell, 2019;

Ansell, 2019).

2

using granular transaction data suggest that the disconnect between rent and price

dispersion is not driven by measurement error due to market segmentation between

owner-occupied and rental housing (Begley, Loewenstein, and Willen, 2021; Demers and

Eisfeldt, 2021).

We propose a novel explanation that allows for increasing dispersion of within-

country housing prices despite much smaller increases in rent dispersion, and ultimately

even without changes in rents altogether. In essence, we argue that a decline in real

risk-free interest rates will have differential effects on housing prices if there is hetero-

geneity in initial rent–price ratios across housing markets within an economy. U.S. and

international data provide ample evidence for such differences in rental yields across

regions. Importantly, large agglomerations exhibit systematically lower rent–price ratios

than smaller cities and more remote regions (Demers and Eisfeldt, 2021; Hilber and

Mense, 2021). Such differences in rent–price ratios can be generated either by spatial

heterogeneity in housing risk, or by differences in local rent growth expectations.

2

Empirically, the presence of higher housing risk premia outside the large agglomerations

has been demonstrated by Amaral et al. (2021). There is limited evidence on rent growth

expectations on the regional level, but realized rent growth does not seem to differ much

between the major agglomerations and the national average (Van Nieuwerburgh and

Weill, 2010; Amaral et al., 2021). Note, however, that for our proposed mechanism the

source of the heterogeneity in initial rent–price ratios is irrelevant.

To rationalize how the well-documented decline in real safe interest rates since

the 1980s (Holston, Laubach, and Williams, 2017; Del Negro et al., 2019) has boosted

economy-wide housing price dispersion in the presence of initial difference in rent–price

ratios, we turn to a spatial version of the Gordon growth model (Gordon, 1962).

3

We

integrate heterogeneity in risk premia and rent growth expectations across regions in

the present-value equation for housing prices and show that a fall in real discount rates

disproportionately affects the valuation of housing in cities in which initial rent–price

ratios are low. This is because a fall in discount rates leads to a linear fall in rent–price

ratios but a non-linear increase in the price–rent ratio as the inverse function of the

rent–price ratio. With lower initial levels in larger agglomerations such as New York

City, a fall in economy-wide real safe interest rate leads to stronger increases in the

price–rent ratios in these places and to an increase in economy-wide housing price

dispersion without concomitant rent dispersion.

In a last step, we calibrate our model to the data and demonstrate that it can generate

an increase in prices as well as increasing dispersion of price–rent ratios similar to the

2

Note that this holds under more general conditions. Using a simple discount rate – cash flow

decomposition (Campbell and Shiller, 1988), differences in rent–price ratios are driven by local rent

growth expectations or by differences in local housing discount rates.

3

In Figure 9, we plot the evolution of real safe rates for the U.S. and the world using the estimates

from Del Negro et al. (2019). Safe rates display a continuous downward trend since the mid-1980s.

3

observational data. Quantitatively, a fall of the real discount rate of 1.3 percentage points

between 1985 and 2018 generates the rise in real housing prices and their dispersion

observed in our sample of 27 large agglomerations. A 1.3 percentage points fall is close

to existing estimates that point to a fall in real housing discount rates of around 1 and 1.1

percentage points over a similar period (Bracke, Pinchbeck, and Wyatt, 2018; Kuvshinov

and Zimmermann, 2020). Note that the fall in real discount rates was less pronounced

than the fall in the real safe rate, as there is evidence that risk-premia increased over

this period (Caballero, Farhi, and Gourinchas, 2017).

We are not the first to link the rise in real housing prices to declining real interest rates

on the national level (Miles and Monro, 2019; Garriga, Manuelli, and Peralta-Alva, 2019).

Yet to the best of our knowledge, our study is the first to make the point that, in the

presence of initial heterogeneity in rent–price ratios, declining real risk-free interest rates

can not only explain rising overall real housing prices, but also growing housing price

dispersion. Related work by Kroen et al. (2021) for the stock market shows that falling

real interest rates contribute to the rise of superstar firms, especially when interest rate

levels are low.

The remainder of this paper is organized as follows. The following section examines

existing explanations for the increase in housing price dispersion and the evidence

suggesting that these explanations are insufficient. Section 2.2 presents new empirical

evidence that housing price dispersion has notably increased more than rent dispersion

since the 1980s. The subsequent section presents the new mechanism and confirms that

it matches the empirical evidence and can generate the excess price dispersion observed

in the data. The final section concludes.

2 Polarization of housing markets

Table 1 shows the price ratio between the most expensive and the median city as

well as the coefficient of variation of housing prices for cities for the U.S., Sweden,

Germany and the UK in 1980 and today. The ratio of the most expensive to the

median housing price region, and the change in the coefficient of variation tell a

consistent story: in the U.S. and internationally, price dispersion in housing markets

has increased substantially since the 1980s. Rising polarization and its causes have

attracted considerable attention in the spatial and urban economics literature, e.g.,

Glaeser and Gyourko (2002); Quigley and Raphael (2005); Glaeser, Gyourko, and

Saiz (2008); Saks (2008); Saiz (2010); Van Nieuwerburgh and Weill (2010); Gyourko,

Mayer, and Sinai (2013); Favara and Imbs (2015); Hilber and Vermeulen (2016); Been,

Ellen, and O’Regan (2018); Oikarinen et al. (2018); Arundel and Hochstenbach (2019);

Hilber and Mense (2021); Molloy, Nathanson, and Paciorek (2022); Vanhapelto (2022).

4

Table 1: Price ratio of most expensive to median city & regional coefficient of variation

Ratio (Max/Median) Coefficient of Variation

Country

1980 Today

Increase

1980 Today

Increase

N

USA 2.81 8.28 2.9 0.23 0.70 3.1 311

SWE 2.97* 6.14 2.1 0.31* 0.54 1.8 290

DEU 1.45 2.66 1.8 0.20 0.44 2.3 42

UK 3.19* 5.00 1.6 0.31* 0.53 1.7 307

Note: The table shows the housing price ratio of the most expensive to the median location as well as the coefficient of

variation for housing prices in the U.S., Sweden, Germany and the UK in 1980 and today. The units of observation

are the following: for the U.S. MSAs, for Sweden and Germany municipalities and for the U.K. local planning

authorities. *: The data for Sweden starts in 1981 and for the UK in 1995. Data for today is from 2018 for the

U.S. and Germany, from 2020 for the UK and from 2021 for Sweden. The coefficient of variation is defined as

the ratio of the standard deviation to the mean, which are both weighted by initial population. Data sources are:

U.S.: Housing census (1980) and American Community Survey (2018) (see below); Sweden: Purchase price of one-

and two-dwelling buildings by municipality from Statistics Sweden; Germany: Preisspiegel Immobilienverband

Deutschland (Amaral et al., 2021); UK: Median house prices for administrative geographies from the Office for

National Statistics.

2.1 Price dispersion in spatial housing models

In the existing literature, increasing price dispersion is typically linked to diverging

housing market fundamentals across regions. In spatial housing models, price dispersion

derives from the embedded present value equation for housing:

P

i

t

=

∞

∑

j=1

E

Rent

i

t+j

∗

1

1 + r

t

j

!

, (1)

where

P

i

t

is the real housing price in city i at time t,

∑

∞

j=1

Rent

i

t+j

is the stream of future

real rent payments net of costs, and

r

t

is the real discount rate at time t. Note that we are

abstracting from consumption growth in our definition of

r

.

4

The equation directly links

current local housing prices and current and future local rents. Changes in economic

fundamentals, such as wages, affect local demand for housing services and thereby rents

and housing prices.

For instance, Van Nieuwerburgh and Weill (2010) construct a spatial, dynamic equi-

librium model in the tradition of Rosen (1979) and Roback (1982) for the distribution of

metropolitan areas in the U.S. These metropolitan areas are hit by idiosyncratic and per-

sistent productivity shocks. Households with heterogeneous abilities move freely across

4

Note that equation 1 can be derived from a simple consumption based asset-pricing model where

investors derive utility from current and future consumption, by setting

1

1+r

t

= β

u

′

(c

t+1

)

u

′

(c

t

)

, where

β

is the

discount factor of the investor and

u

′

its marginal utility with respect to consumption (Cochrane, 2005).

To simplify, we will abstract from the influence of consumption growth on

r

and simply refer to

r

as the

real discount rate.

5

metropolitan areas in reaction to these shocks. Housing supply is limited by supply

regulations, meaning that rents will adjust to compensate for regional wage differences.

This, in turn, determines housing prices. The authors calibrate productivity shocks to

match the increase in the observed regional wage dispersion between metropolitan areas

from 1975 to 2007. The model matches the increase in housing price dispersion observed

in the data. However, as the authors note, it also produces an increase in rent dispersion

three times larger than observed empirically.

In another well-known paper, Gyourko, Mayer, and Sinai (2013) develop a two-

location model to show that increasing national demand generated by population

growth affects regions differently, depending on local housing supply elasticities. Under

the assumption that people prefer to live in supply-constrained cities, the model predicts

that in response to increasing national demand, supply-constrained cities will experience

a stronger rental increase than unconstrained cities. This increase in rents passes through

to housing prices via the present-value equation. The authors call the cities that display

a combination of low supply elasticities and strong housing price growth “superstar

cities”. The paper does not explicitly study the model predictions for rents, but in

Appendix A, we use the paper’s data and show that prices in superstar cities increased

considerably more than rents.

A partial exception to the assumption that growing housing price dispersion is a

function of increasing rent dispersion is Hilber and Mense (2021). The authors use

regional data for the U.K. from 1997 to 2018 and start from the empirical observation that

prices have increased much more in the “superstar” city London than rents, i.e., the price–

rent ratio has surged in London compared to the rest of the country. They explain this

with serially correlated housing demand shocks that induce heterogeneous rent growth

expectations. However, the paper is chiefly concerned with cyclical fluctuations and

the proposed mechanism generates transitory divergence in price–rent ratios between

regions. Over longer horizons, housing demand shocks mean-revert so that rents and

prices move in lockstep (Piazzesi and Schneider, 2016).

2.2 Empirical evidence on pr ice and rent dispersion

Explanations focused on rent dispersion as the source of increasing price dispersion

are at odds with one important stylized fact in the data: price dispersion has increased

much more than rent dispersion. Evidence for such divergent trends has not only been

exposed in the U.K. data discussed above (Hilber and Mense, 2021), but also in recent

U.S. data (Demers and Eisfeldt, 2021; Molloy, Nathanson, and Paciorek, 2022).

Concerns that measurement error could be responsible for the apparent divergence

between rent and price growth do not appear convincing in the light of recent studies

with micro data. In principle, market segmentation could lead to selection bias if rental

6

data are typically taken from lower quality segments of the housing market while prices

mainly come from higher-quality segments (Glaeser and Gyourko, 2007). However,

Begley, Loewenstein, and Willen (2021) study micro-data from Corelogic on prices and

rents for the same property to estimate price–rent ratios, thereby avoiding selection

bias. They show that the price variation in owner- and renter-occupied housing markets

are closely correlated. If anything, renter-occupied prices have risen more than owner-

occupied prices. Demers and Eisfeldt (2021) also use micro-data from the American

Housing Survey to build rent–price ratios for 15 different U.S. cities from 1985 to 2020.

Relying on hedonic models and non-parametric methods, they show that rent–price

ratios fell most strongly in “expensive” cities.

In the following, we systematize the available evidence for price and rental dispersion

using two comprehensive data sets that have recently become available (Amaral et

al., 2021). One is a long-run cross country data set; the other covers the entire cross-

section of regions in the U.S.. Both data sets show that dispersion in housing prices

increased substantially more than dispersion in rents since the 1980s.

The first data set covers housing price series, rent series, and rent–price ratios for 27

agglomerations in 15 OECD countries over the past century. The major agglomerations

are defined as the largest cities within each country in terms of 1900 population statistics,

including cities like London, New York, Paris, Berlin and Tokyo. We merge the city-level

series with nation-wide housing data from Jord

`

a et al. (2019).

The second covers the entire cross-section of 316 MSAs in the U.S. It comprises

of housing prices, rents and price–rent ratios with decadal frequency from housing

censuses. It is based on the data in Gyourko, Mayer, and Sinai (2013), but extended to

2018 using the American Community Survey.

Figure 1 panel (a) plots the geometric mean of real housing price and rent increases

between 1980 and 2018 for the 27 major agglomerations next to the geometric mean of

national real housing price and rent increases.

5

The national means are weighted by

the number of sample agglomerations in the respective country. The Figure brings two

key insights. First, housing prices have grown much more than rents in both the major

agglomerations and at national levels. Second, housing prices have grown considerably

more in the major agglomerations than the national average. The difference in mean

growth rates is as large as 70 basis points per year, which implies that mean growth

rates for the agglomerations have been more than 50% higher compared to national

housing price growth rates over the past four decades. With only 35 basis points the

difference in yearly rent growth rates is considerably lower.

Appendix B presents geometric means of housing price and rent growth rates

5

We use log growth rates to calculate means and confidence intervals, such that the resulting values

can be interpreted as geometric means. This way, mean values show the overall trend during the past 4

decades and are not driven by the volatility of the series.

7

Figure 1:

Evolution of housing price and rent growth rates and price-rent ratios between 1980 and 2018

(a) Annual growth rates 27 major agglomerations

0 .5 1 1.5 2 2.5

Annual growth rate (%)

Housing prices Rents

Agglomerations

National

(b) Annual growth rates U.S. MSAs

0 .2 .4 .6 .8

Density

0 1 2 3 4

Annual growth rate (%)

Housing prices

Rents

(c) Price-rent ratios 27 major agglomerations

1.53

1.28

.5 1 1.5

Price-rent ratio (1980 = 1)

1950 1960 1970 1980 1990 2000 2010 2020

Agglomerations

National

(d) Price-rent ratios U.S. MSAs

0 .05 .1 .15 .2

Density

10 20 30 40 50 60 70 80

1980

2018

Note: Panel (a): Geometric mean of annual housing price and rent growth rates of 27 major agglomerations (black)

and the respective national averages weighted by the number of sample agglomerations in the respective country.

Means and confidence intervals are calculated using log growth rates and transformed back to percentage growth

rates afterwards. Panel (b): Kernel density of annualized housing price and rent growth rates between 1980 and

2018 for 316 U.S. MSAs. Panel (c): Index of equally-weighted average increases of price-rent ratios of 27 major

agglomerations and average national increases of price-rent ratios weighted by the number of sample agglomerations

in the respective country. 1980=1. Panel (d): Kernel density of price-rent ratios of 316 U.S. MSAs in 1980 and

2018 calculated from net rental yields.

between 1980 and 2018 by city, demonstrating that housing prices have grown more than

rents in almost all economies. Housing price growth has been higher at the city-level

than nationally for virtually all agglomerations in the cross-country data set. This

phenomenon is particularly pronounced for the largest agglomerations, like London,

New York or Paris.

Figure 1 panel (b) shows kernel densities for the geometric mean of housing price

and rent growth rates between 1980 and 2018 by MSA for the full sample of U.S. MSAs.

Housing price growth rates have not only been on average higher compared to rent

8

growth rates, but also show more dispersion. The fat right tail of housing price growth

rates is particularly striking. As discussed in Gyourko, Mayer, and Sinai (2013) this

indicates that a small set of cities had very high yearly housing price growth rates.

Importantly, this is not mirrored by rent growth rates.

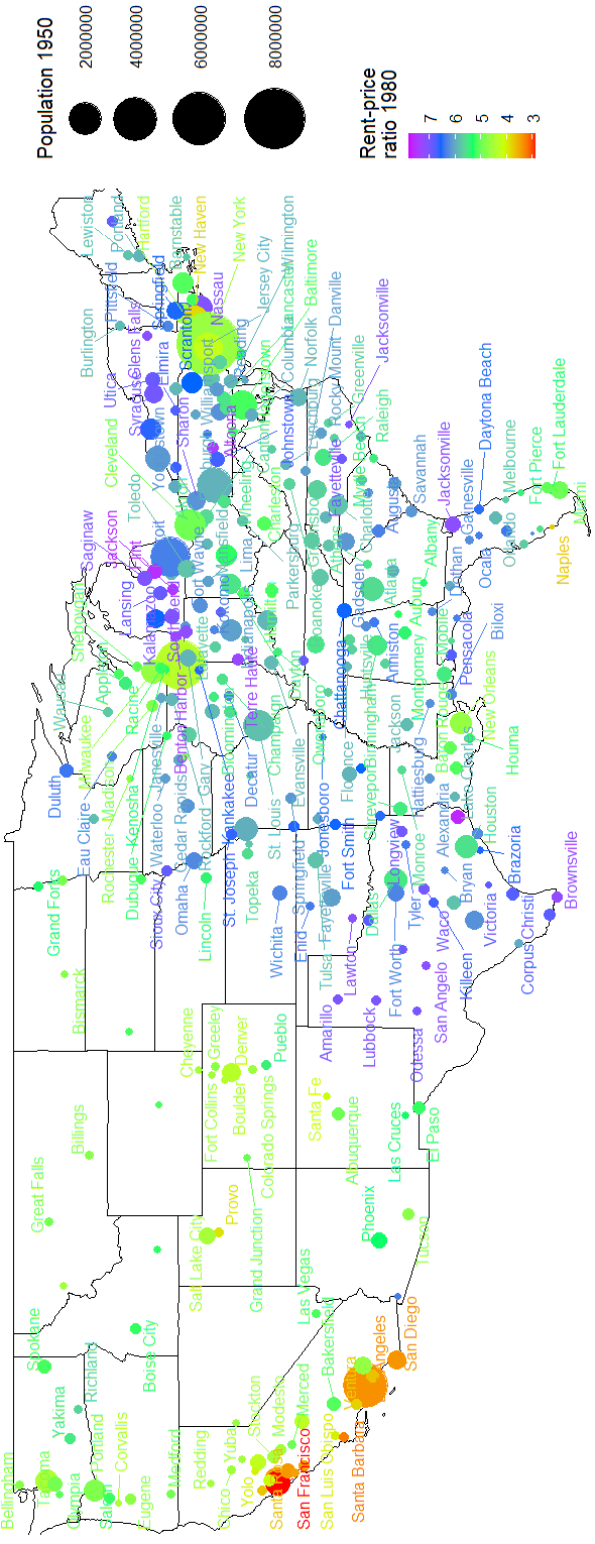

A necessary condition for our mechanism to hold is that rent–price ratios differ

initially by cities. We mapped rent-price ratios for US MSAs in 1980. The resulting

Figure 10 in the Appendix visually shows a correlation between city size and the initial

rent-price ratios and a clear geographical clustering: the regions with populous urban

agglomerations at the coasts already started with considerably lower rent-price ratios in

1980 when compared to the cities in the more rural central regions.

6

Additionally, we

show in Figure 3 that this result also holds for our international data set.

Figure 1 panel (c) shows the average increases in price-rent ratios over time for

the 27 major agglomerations and on the national level to show the proportion of the

housing price dispersion that cannot be accounted for by rent dispersion. Changes

in price–rent ratios indicate how much housing prices changed after accounting for

changes in rents. From previous observations, price–rent ratios are expected to have

increased considerably since 1980. More importantly, the data show that price–rent

ratios have increased considerably more in the major agglomerations than the national

average. While the gap in price–rent ratios varies over the cycle, a phenomenon that

could be explained by the mechanism proposed in Hilber and Mense (2021), it shows

a strong persistence over the last decades and seems to be increasing over time. The

gap starts to arise during the 1980s and does not exist in the period before. This timing

coincides with the fall in the risk free rate.

Figure 1 panel (d) plots the distribution of U.S. MSA-level price–rent ratios in 1980

and 2018, demonstrating not only that the dispersion of price-rent ratios was already

substantial in 1980, but also that it increased considerably over the last decades. Again,

this phenomenon is particularly strong for the distribution’s right tail, where also the

major agglomerations like New York are located. As expected, mean price–rent ratios

have also increased over time. Still, the coefficient of variation (CV) increased from 0.19

to 0.32.

3 Falling real interest rates and housing price dispersion

This section constructs a parsimonious, spatial asset-pricing model of the housing

market to rationalize an increase in housing price dispersion that does not follow from

increasing rent dispersion but results from differences in initial rent–price ratios between

cities.

6

Demers and Eisfeldt (2021) also show substantial differences in rent-price ratios for a smaller sample

of U.S. MSAs in the 1980s.

9

We also start from present value equation (1), the only difference being that we allow

for differences in real discount rates between cities:

P

i

t

=

∞

∑

j=1

E

Rent

i

t+j

∗

1

1 + r

i

t

!

j

. (2)

From a theoretical perspective, a combination of local market segmentation and incom-

plete markets imply that discount rates do not need to equalize between cities.

7

Piazzesi,

Schneider, and Stroebel (2020) show that housing markets are locally segmented, using

data on online searches to document large differences in housing search behavior across

different municipalities in California.

8

Housing markets are also incomplete because

housing assets are indivisible, and homeowners are typically non-diversified. The lack of

diversification implies limitations to arbitrage precluding discount rates from equalizing

(Piazzesi and Schneider, 2016).

Empirically, Amaral et al. (2021) show that over the long run returns have been

persistently lower in large cities than in the rest of the country. Differences in housing

returns are likely due to differences in housing risk, as housing prices co-vary less with

income in larger MSAs and idiosyncratic housing price risk is lower. The assumption that

the discount rate differs geographically is further supported by the empirical evidence

that landlords concentrate their housing portfolios close to their place of residency,

exposing them to local housing market risks (Levy, 2021).

In the following, we assume that discount rates are composed of a risk-free compo-

nent, that is equal for the entire country and a risk-premium that can differ by the city

invested in;

r

i

t

= risk-free

t

+ risk-premium

i

t

. To simplify the discussion, we make two

additional assumptions: First, we assume that rents in city i are expected at time t to

grow at a constant rate

g

i

t

. Second, we assume that

r

i

t

> g

i

t

, such that housing prices

are finite. This allows us to rewrite equation (2) as the Gordon (1962) growth valuation

formula:

P

i

t

=

∞

∑

j=1

Rent

i

t

∗

1 + g

i

t

1 + r

i

t

!

j

⇐⇒ P

i

t

= Rent

i

t

∗

1 + g

i

t

r

i

t

− g

i

t

. (3)

Following this equation, the rent-price ratio is equal to:

Rent-price ratio

i

t

=

Rent

i

t

P

i

t

=

r

i

t

− g

i

t

1 + g

i

t

. (4)

We next consider a setting with two cities: agglomeration A and reservation city

B. The reservation city can be understood as the average of all other locations within

7

Sagi (2021) builds a housing search model, showing that heterogeneity in discount rates is an essential

condition to explain the dynamics in real estate prices.

8

They also demonstrate that differences in housing search between different quality segments within

municipalities are less pronounced.

10

a country except the large agglomeration. To compare both cities, we make three

additional assumptions. First, as argued in the urban economics literature (Gyourko,

Mayer, and Sinai, 2013; Hilber and Mense, 2021) we assume expected rent growth in the

large agglomeration is higher than or equal to the reservation city;

g

A

t

≥ g

B

t

∀t

. Second,

as argued above, we assume that risk-premia are lower or equal for housing investments

in large agglomerations compared to the reservation city, such that

r

A

t

≤ r

B

t

∀t

. Third,

we assume that at least one of the two previous inequalities is strict, such that rent–price

ratios are lower in the agglomeration and:

r

B

t

− g

B

t

> r

A

t

− g

A

t

> 0. (5)

From equation (3) we can write the log price difference between cities A and B as:

log(P

A

t

) − log(P

B

t

) = log(Rent

A

t

) + log

1 + g

A

t

r

A

t

− g

A

t

− log(Rent

B

t

) − log

1 + g

B

t

r

B

t

− g

B

t

. (6)

Next we derive the predictions of our model after a fall in the real risk-free rate. We

assume that the real risk-free rate decreases by ∆, such that:

log(P

A

t

) − log(P

B

t

) =

log(Rent

A

t

) + log

1 + g

A

t

r

A

t

− ∆ − g

A

t

− log(Rent

B

t

) − log

1 + g

B

t

r

B

t

− ∆ − g

B

t

. (7)

If we differentiate with respect to ∆ and under the assumptions made above, we get:

∂

log(P

A

t

) − log(P

B

t

)

∂∆

=

1

r

A

t

− ∆ − g

A

t

−

1

r

B

t

− ∆ − g

B

t

> 0.

This demonstrates that a uniform fall in real discount rates across both cities, generated

by a fall in the real risk-free rate, increases housing price dispersion if rent–price ratios

initially differ.

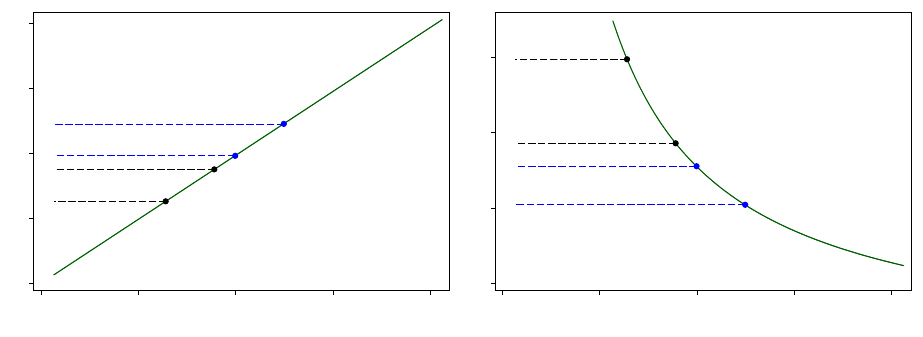

The intuition for this observation is presented in Figure 2. Panel (a) plots the rent–

price ratio in the model as a function of

r − g

for a varying

r

, wherein the rent–price

ratio changes linearly in

r

. Following equation (5), we assume that

r − g

is lower in

the agglomeration at time t, resulting in a lower rent–price ratio. Next, we assume

that between

t

and

t + 1

r falls in both cities by one percentage point. This leads to

an approximately equal fall in the rent–price ratio in the agglomeration (A) and in the

reservation city (B).

Figure 2 panel (b) plots the corresponding price–rent ratio. As the price–rent ratio

is the inverse function of the rent–price ratio, when

r

changes, the price–rent ratio

changes in a non-linear fashion. Since the initial price–rent ratio is higher in the

11

Figure 2: A fall in discount rates in the model

(a) Rent-price ratios

Agglomeration A, t

Reservation city B, t

Agglomeration A, t+1

Reservation city B, t+1

0 .02 .04 .06 .08

0 .02 .04 .06 .08

r-g

(b) Price-rent ratios

Agglomeration A, t

Reservation city B, t

Agglomeration A, t+1

Reservation city B, t+1

10 20 30 40

0 .02 .04 .06 .08

r-g

Note: Panel (a) plots the rent–price ratio in our model as a function of

r − g

. To calculate the points, we assumed

that g = 0.0175. Panel (b) shows the corresponding price–rent ratio.

agglomeration, an equally large fall in

r

leads to a larger increase in the price–rent ratio

in the agglomeration than in the reservation city. Subsequently, the price dispersion

between the agglomeration and the reservation city increases when

r

falls, even when

rents are constant in both cities.

3.1 Rent–price ratios in the data

The previous section determined that price dispersion increases in response to a fall

in the real risk-free rate if rent–price ratios initially differ. Our model also predicts a

parallel fall in rent–price ratios across cities due to a fall in the real risk-free rate.

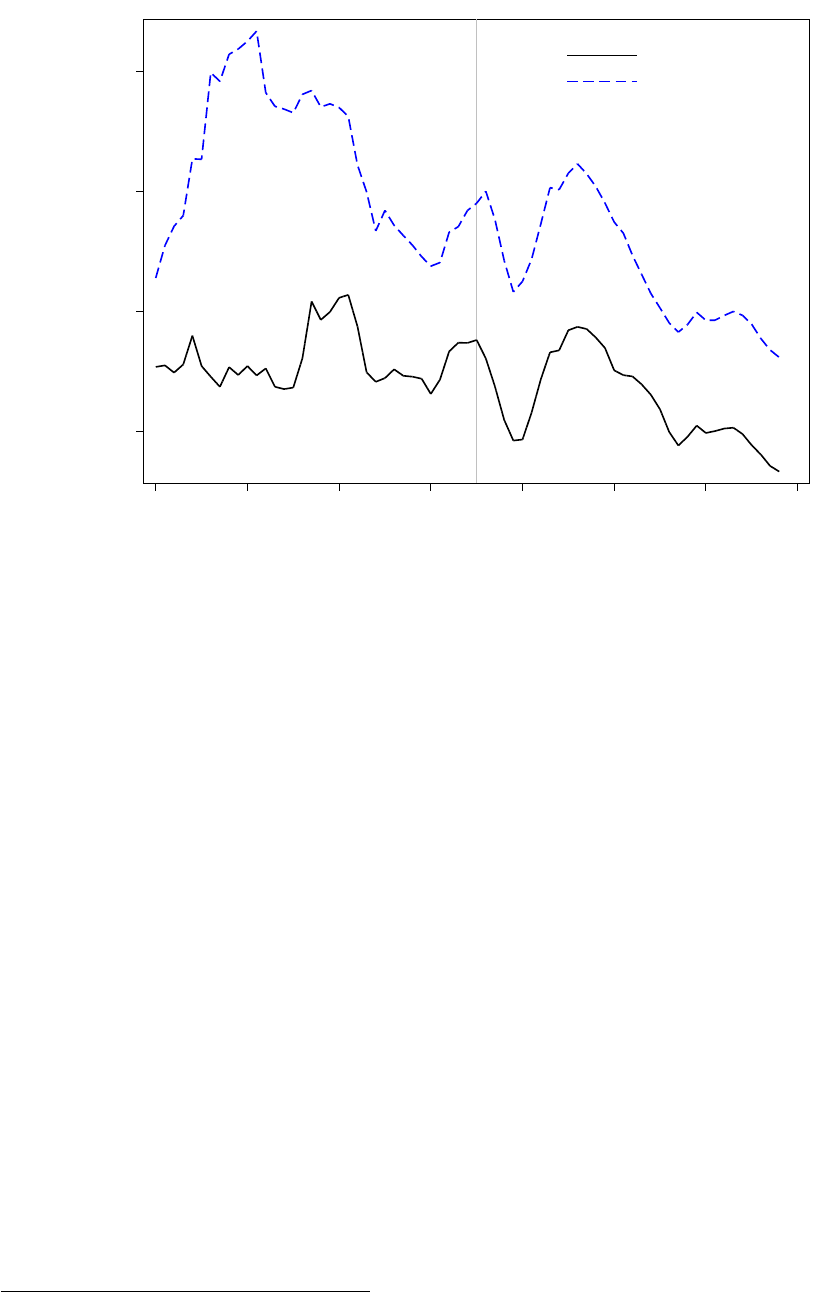

Figure 3 plots the average rent-price ratios in the 27 major agglomerations and on the

national level. Two observations are important. First, rent–price ratios have been lower

in the major agglomerations over the entire period since 1950. This evidence validates

the assumption regarding the initial differences in rent–price ratios.

Second, the rent–price ratios in the major agglomerations and at the national level

have moved in parallel trajectories since 1985 (abstracting from the cyclical variation),

suggesting a common downward trend. Rent-price ratios fell by around 1.2 percentage

points from 1985 to 2018 in the major agglomerations and at the national level. The

equally large fall in rent–price ratios in the major agglomerations and at the national

level is equivalent to the parallel fall in rent–price ratios predicted by the model. Note

that alternative mechanisms that attempt to explain the increase in price dispersion

based on factors that solely affect the major agglomerations, would predict a divergence

in rent–price ratios between the major agglomerations and the rest.

We also use the U.S. MSA-level data to compare the full distribution of price–rent

12

Figure 3: Rent–price ratios in the data

.03 .04 .05 .06

1950 1960 1970 1980 1990 2000 2010 2020

Agglomerations

National

Note: The solid black line is the non-weighted average rent–price ratio of 27 major agglomerations. The dashed blue

line is the average of the national rent–price ratio weighted by the number of sample agglomerations in the respective

country.

ratios in 2018 with our model prediction. While the data align well with our proposed

mechanism, there is room for other factors at play such as diverging rent growth

expectations between the large agglomerations and the rest of the economy. We discuss

this in more detail in Appendix D.

4 Model calibration

To simulate the increase in price dispersion in response to a fall in r in our model,

we calibrate the model to the following values. We set the expected real rent growth in

the agglomeration and the reservation city equal to 1.75 %,

g

A

t

= g

B

t

= 0.0175 ∀t

, which

is close to long-run real rent growth rates observed in our international data set.

9

Next,

we assume that the real discount rate in the agglomeration is 1 percentage point lower

than in the reservation city;

r

A

t

= r

B

t

− 0.01 ∀t

. This is equivalent to the difference in

total housing returns of around 1 percentage point found in Amaral et al. (2021). For

simplification we assume that real rents in the agglomeration and in the reservation city

are equal to one in period one, Rent

A

1

= Rent

B

1

= 1.

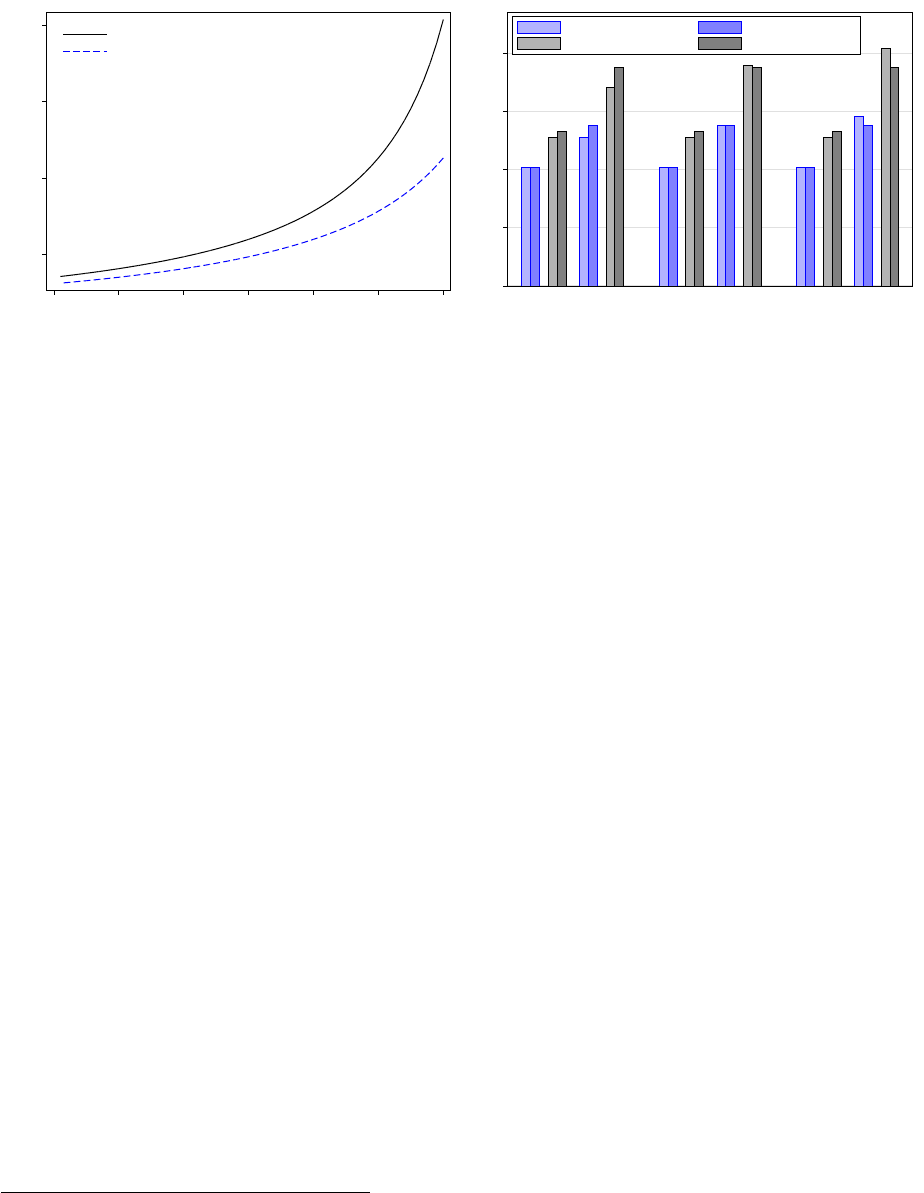

Figure 4 panel (a) plots the resulting price–rent ratios in the agglomeration and

9

Between 1950 and 2018, rents grew on average by 1.86 % in the 27 major agglomerations and by 1.65

% at the national level.

13

Figure 4: Simulated price-rent ratios in response to a fall in r

(a) Price-rent ratios as a function of r

A

t

20 40 60 80

Price-rent ratio

.1 .09 .08 .07 .06 .05 .04

r

A

Agglomeration A

Reservation city B

(b) Model predictions vs. data

0 10 20 30 40

Price-rent ratio

fall in r = 0.010 fall in r = 0.013 fall in r = 0.015

1985 2018 1985 2018 1985 2018

National Model National Data

Agglomeration Model Agglomeration Data

Note: Panel (a) shows price–rent ratios for the agglomeration and the reservation city in the model relative to the

discount rate in the reservation city. Panel (b) compares the model to the data for different assumed values of the fall

in the discount rate r. For both exercises, we assume that g = 0.0175 and r

A

= r

B

− 0.01.

reservation cities as a function of

r

B

t

, demonstrating that the dispersion in price–rent

ratios increases when discount rates fall. Although the initial difference between the

cities is small for high discount rates, the difference becomes substantial as discount

rates become smaller.

10

The next step is to assess whether our model matches the increasing levels and dis-

persion of price–rent ratios in the data. This requires estimates for the housing discount

rates in 1985 and 2018. The estimated decline in the real risk-free rate ranges from 2.5 to

5 percentage points depending on the estimation method (Del Negro et al., 2019; Rachel

and Summers, 2019). At the same time, there is considerable evidence that risk-premia

have risen during this period, which partly offsets the effect of the fall in the risk-free

rate on housing discount rates (Caballero, Farhi, and Gourinchas, 2017; Kuvshinov and

Zimmermann, 2020). To the best of our knowledge, there exist two estimates for the

decline in real housing discount rates over this period. Using data on U.K. leaseholds,

Bracke, Pinchbeck, and Wyatt (2018) estimate a drop of around 1 percentage point

between the 1990s and the 2010s for very long housing discount rates, their results are

in line with Giglio, Maggiori, and Stroebel (2015), who also estimate discount rates for

the housing market in Singapore.

11

Kuvshinov and Zimmermann (2020) estimate a

drop of around 1.1 percentage points between 1985 and 2015 for a sample of developed

countries very similar to ours.

12

Figure 4 panel (b) compares the price–rent ratios predicted by our model to the actual

10

The same result is demonstrated by Kroen et al. (2021) for stock markets.

11

Both papers measure discount rates for housing service flows more than 100 years in the future.

12

Our sample additionally contains Canada and our data sources differ for some specific countries. The

details can be found in the Data Appendix of Amaral et al. (2021).

14

price–rent ratios in the data for the years 1985 and 2018. We represent three scenarios

for the fall in real discount rates. On the left, real discount rates fell by 1 p.p., in the

middle by 1.3 p.p. and on the right by 1.5 p.p. Overall, the model slightly overshoots the

price–rent ratio in the major agglomerations in 1985.

13

This indicates that the difference

in risk-premia between the agglomerations and the national average was either smaller

than 1 percentage point or the rent-growth expectations have been slightly higher in the

major agglomerations.

In the scenario where real discount rates fall by 1 percentage point, our model cannot

fully account for the rise in levels and dispersion of the price–rent ratio. It does, however,

generate a substantial portion of the increase in levels and dispersion we observe in the

data. Assuming a fall in

r

of 1.5 percentage points instead, our model does overshoot

both the level and the dispersion in housing prices we observe in the data. Matching the

increase in levels and dispersion in the data requires a fall in discount rates of around

1.3 percentage points.

Our model also matches the increase in levels and dispersion of price–rent ratios if

we assume that expected rent growth was 1 p.p. higher in the major agglomerations,

keeping discount rates constant across cities,

r

A

= r

B

. Given the small difference in

observed rent growth and the stable return difference between major agglomerations

and the national average, we assert that a constant difference in discount rates is more

realistic than a constant difference in expected rent growth. A large-scale simulation of

many different combinations of different model variables (Appendix C) demonstrates

that falling discount rates robustly lead to increasing housing price dispersion for most

realistic value combinations for r and g.

5 Conclusion

In this paper, we present a novel explanation for increasing housing price dispersion

that, unlike existing models, does not require a comparable rise in rent dispersion. The

key new insight is that a uniform fall in real interest rates can have heterogeneous

spatial effects. For realistic values for the fall in real discount rates, the model is able

to reproduce the growing dispersion of price–rent ratios observed in the data even

in the absence of changes in fundamentals. In light of the central role of rental and

housing price dynamics in urban economics, more research is needed to integrate this

mechanism into more complex spatial models.

14

An important takeaway of the paper is

that increasing polarization of housing prices between “superstar cities” and the rest

13

Note that the model exactly matches the national price–rent ratio in 1985 by construction, since we

back-out the initial average national discount rate from the rent-price ratio in 1985 using our model.

14

A promising example of this is the dynamic spatial equilibrium model of housing demand and supply

in Vanhapelto (2022).

15

of the country is not just driven by supply-side restrictions, but that interest rates can

play a central role not only for the pricing on a national level, but also for the growing

dispersion of housing prices. For future research in urban economics this implies to also

pay attention to financial factors when thinking about trends in regional housing markets.

The findings of this paper potentially also speak to the housing market outlook in the

current environment of rising interest rates. All else equal, some of the polarization of

housing prices that we could observe over the past decades can be expected to revert if

going forward real discount rates rise again.

16

References

Adler, David and Ben Ansell (June 2019). “Housing and Populism”. In: West European

Politics 43(2), pp. 344–365.

Amaral, Francisco et al. (2021). “Superstar Returns”. In: FRB of New York Staff Report(

999).

Ansell, Ben (May 2019). “The Politics of Housing”. In: Annual Review of Political Science

22(1), pp. 165–185.

Arundel, Rowan and Cody Hochstenbach (2019). “Divided Access and the Spatial

Polarization of Housing Wealth”. In: Urban Geography, pp. 1–27.

Been, Vicki, Ingrid Gould Ellen, and Katherine O’Regan (Dec. 2018). “Supply Skepticism:

Housing Supply and Affordability”. In: Housing Policy Debate 29(1), pp. 25–40.

Begley, Jaclene, Lara Loewenstein, and Paul S. Willen (2021). “The Rent-price Ratio

during the 2000s Housing Boom and Bust: Measurement and Implications.” In: Work

in progress.

Blanchard, Olivier J. and Lawrence F Katz (1992). “Regional evolutions”. In: Brookings

Papers on Economic Activity, Economic Studies Program, The Brookings Institution 23(1).

Bracke, Philippe, Edward W Pinchbeck, and James Wyatt (2018). “The Time Value of

Housing: Historical Evidence on Discount Rates”. In: The Economic Journal 128(613),

pp. 1820–1843.

Caballero, Ricardo J., Emmanuel Farhi, and Pierre-Olivier Gourinchas (May 2017). “Rents,

Technical Change, and Risk Premia Accounting for Secular Trends in Interest Rates,

Returns on Capital, Earning Yields, and Factor Shares”. In: American Economic Review

107(5), pp. 614–620.

Campbell, John Y. and Robert J. Shiller (July 1988). “The Dividend-Price Ratio and

Expectations of Future Dividends and Discount Factors”. In: Review of Financial

Studies 1(3), pp. 195–228.

Cochrane, John H. (2005). Asset Pricing. Princeton University Press.

Del Negro, Marco et al. (May 2019). “Global Trends in Interest Rates”. In: Journal of

International Economics 118, pp. 248–262.

Demers, Andrew and Andrea L. Eisfeldt (May 2021). “Total Returns to Single-Family

Rentals”. In: Real Estate Economics.

Favara, Giovanni and Jean Imbs (Mar. 2015). “Credit Supply and the Price of Housing”.

In: American Economic Review 105(3), pp. 958–992.

Garriga, Carlos, Rodolfo Manuelli, and Adrian Peralta-Alva (June 2019). “A Macroeco-

nomic Model of Price Swings in the Housing Market”. In: American Economic Review

109(6), pp. 2036–2072.

Giglio, Stefano, Matteo Maggiori, and Johannes Stroebel (2015). “Very Long-Run Dis-

count Rates”. In: The Quarterly Journal of Economics 130(1), pp. 1–53.

17

Glaeser, Edward and Joseph Gyourko (Mar. 2002). The Impact of Zoning on Housing

Affordability. Tech. rep.

Glaeser, Edward and Joseph Gyourko (2007). “Arbitrage in Housing Markets”. In.

Glaeser, Edward, Joseph Gyourko, and Albert Saiz (Sept. 2008). “Housing Supply and

Housing Bubbles”. In: Journal of Urban Economics 64(2), pp. 198–217.

Gordon, Myron J (1962). “The savings investment and valuation of a corporation”. In:

The Review of Economics and Statistics, pp. 37–51.

Guren, Adam M et al. (Apr. 2020). “Housing Wealth Effects: The Long View”. In: The

Review of Economic Studies 88(2), pp. 669–707.

Gyourko, Joseph, Christopher Mayer, and Todd Sinai (Nov. 2013). “Superstar Cities”. In:

American Economic Journal: Economic Policy 5(4), pp. 167–199.

Herkenhoff, Kyle F, Lee E Ohanian, and Edward C Prescott (2018). “Tarnishing the

golden and empire states: Land-use restrictions and the US economic slowdown”. In:

Journal of Monetary Economics 93, pp. 89–109.

Hilber, Christian and Andreas Mense (2021). “Why Have House Prices Risen so Much

More than Rents in Superstar Cities?” In.

Hilber, Christian and Wouter Vermeulen (June 2016). “The Impact of Supply Constraints

on House Prices in England”. In: The Economic Journal 126(591), pp. 358–405.

Holston, Kathryn, Thomas Laubach, and John C Williams (2017). “Measuring the Natural

Rate of Interest: International Trends and Determinants”. In: Journal of International

Economics 108, S59–S75.

Hsieh, Chang-Tai and Enrico Moretti (Apr. 2019). “Housing Constraints and Spatial

Misallocation”. In: American Economic Journal: Macroeconomics 11(2), pp. 1–39.

Jord

`

a,

`

Oscar et al. (Apr. 2019). “The Rate of Return on Everything, 1870-2015*”. In: The

Quarterly Journal of Economics 134(3), pp. 1225–1298.

Kroen, Thomas et al. (2021). “Falling Rates and Rising Superstars”. In.

Kuvshinov, Dmitry and Kaspar Zimmermann (2020). “The Expected Return on Risky

Assets: International Long-run Evidence”. In: SSRN 3546005.

Levy, Antoine (2021). “Housing Policy with Home-Biased Landlords: Evidence from

French Rental Markets”. In.

Mian, Atif, Kamalesh Rao, and Amir Sufi (Sept. 2013). “Household Balance Sheets,

Consumption, and the Economic Slump*”. In: The Quarterly Journal of Economics

128(4), pp. 1687–1726.

Mian, Atif and Amir Sufi (Aug. 2011). “House Prices, Home Equity-Based Borrow-

ing, and the US Household Leverage Crisis”. In: American Economic Review 101(5),

pp. 2132–2156.

Mian, Atif and Amir Sufi (Nov. 2014). “What Explains the 2007-2009 Drop in Employ-

ment?” In: Econometrica 82(6), pp. 2197–2223.

18

Miles, David Kenneth and Victoria Monro (2019). “UK House Prices and Three Decades

of Decline in the Risk-Free Real Interest Rate”. In: SSRN Electronic Journal.

Molloy, Raven, Charles Nathanson, and Andrew Paciorek (2022). “Housing Supply and

Affordability: Evidence from Rents, Housing Consumption and Household Location”.

In: Journal of Urban Economics 129, p. 103427.

Oikarinen, Elias et al. (May 2018). “U.S. Metropolitan House Price Dynamics”. In: Journal

of Urban Economics 105, pp. 54–69.

Ortalo-Magn

´

e, Fran

c¸

ois and Andrea Prat (2014). “On the Political Economy of Ur-

ban Growth: Homeownership versus Affordability”. In: American Economic Journal:

Microeconomics 6(1), pp. 154–81.

Piazzesi, Monika and Martin Schneider (2016). “Housing and Macroeconomics”. In:

Handbook of Macroeconomics. Elsevier, pp. 1547–1640.

Piazzesi, Monika, Martin Schneider, and Johannes Stroebel (2020). “Segmented housing

search”. In: American Economic Review 110(3), pp. 720–59.

Poterba, James M. (Nov. 1984). “Tax Subsidies to Owner-Occupied Housing: An Asset-

Market Approach”. In: The Quarterly Journal of Economics 99(4), p. 729.

Quigley, John M and Steven Raphael (Apr. 2005). “Regulation and the High Cost of

Housing in California”. In: American Economic Review 95(2), pp. 323–328.

Rachel, Lukasz and Lawrence Summers (Aug. 2019). On Secular Stagnation in the Industri-

alized World. Tech. rep.

Roback, Jennifer (1982). “Wages, Rents, and the Quality of Life”. In: Journal of Political

Economy 90(6), pp. 1257–1278.

Rosen, Sherwin (1979). “Wage-Based Indexes of Urban Quality of Life”. In: Current Issues

in Urban Economics, pp. 74–104.

Sagi, Jacob S (Oct. 2021). “Asset-Level Risk and Return in Real Estate Investments”. In:

The Review of Financial Studies 34(8). Ed. by Stijn Van Nieuwerburgh, pp. 3647–3694.

Saiz, Albert (2010). “The Geographic Determinants of Housing Supply”. In: The Quarterly

Journal of Economics 125(3), pp. 1253–1296.

Saks, Raven (July 2008). “Job Creation and Housing Construction: Constraints on

Metropolitan Area Employment Growth”. In: Journal of Urban Economics 64(1), pp. 178–

195.

Stroebel, Johannes and Joseph Vavra (June 2019). “House Prices, Local Demand, and

Retail Prices”. In: Journal of Political Economy 127(3), pp. 1391–1436.

Van Nieuwerburgh, Stijn G and Pierre-Olivier Weill (Aug. 2010). “Why Has House Price

Dispersion Gone Up?” In: Review of Economic Studies 77(4), pp. 1567–1606.

Vanhapelto, Tuuli (2022). “House Prices and Rents in a Dynamic Spatial Equilibrium”.

In: Job Market Paper.

19

Appendix

A Superstar cities revisited

A.1 Rent growth

Gyourko, Mayer, and Sinai (2013) derive a set of propositions, that directly imply

that superstar cities should have experienced stronger rent growth than the rest of the

country. Proposition 1 states that superstar cities have higher rental values than the

rest of the country. Proposition 3 states that an increase in aggregate income leads to

stronger rental increases in the superstar cities than in the rest.

15

These two propositions

are tested in Tables 2 and 3 of the paper, using log house value as the dependent variable.

Here, we replicate the analysis focusing on the effects on house value growth and rent

growth. Table 2 presents our regression output. There are two primary results. First, the

coefficients for rent values are significant and positive, just as the coefficients for house

values. Second, the coefficients for rent values are slightly less than half those of house

values. This indicates that the effects on rents are much smaller than on prices, which

raises the question of whether we can fully explain the strong divergence in prices with

the divergence in rents.

Table 2: Replicating Panel A from Tables 2 and 3 in Gyourko, Mayer, and Sinai (2013)

log house value log rent value log house value log rent value

Superstar 0.605 0.291

(0.0729) (0.0377)

Superstar x Rich 0.394 0.172

(0.0356) (0.0193)

N 1116 1116 1116 1116

adj. R

2

0.414 0.308 0.856 0.861

Note: This table replicates Panel A from Tables 2 and 3 in Gyourko, Mayer, and Sinai (2013). In addition to the

regression on log house value, we perform the same regression on rent log value. Columns 1 and 2 present the

results of a regression of the left hand-side variable on a superstar dummy and year fixed effects. Columns 3 and 4

present the OLS coefficients of a regression on an interaction effect of a superstar dummy and the log number of rich

families in the U.S. and time and superstar fixed effects. Standard errors are in parentheses and are clustered at the

MSA-level.

15

Propositions 2 and 4 relate to income growth in the superstar cities.

20

A.2 Price-rent ratios

In this subsection, we present evidence that the divergence in price-rent ratios

between superstar cities and the rest has strongly increased since the 1980s, extending

the data set presented in Gyourko, Mayer, and Sinai (2013) to 2010 and 2018. We then

use the definition of superstar cities to categorize the cities into superstars group and

non-superstars groups, which we call the rest of the country. We estimate an equally

weighted average of price–rent ratios for both groups by year. Figure 5 presents the

results. The Figure shows that price–rent ratios have been increasing over time in

superstar areas and in the rest of the country. However, in the superstar cities, price–rent

ratios have increased much more, leading to a growing regional divergence in price–rent

ratios.

Figure 5: Price–rent ratios in the U.S., 1950-2018

10 20 30

1950 1960 1970 1980 1990 2000 2010 2018

Rest of country

Superstars

CI 95%

Note: We define superstar cities as cities that were at least once a superstar city between 1950 and 2000 according to

the superstar definition in Gyourko, Mayer, and Sinai (2013). We extended the data from Gyourko, Mayer, and

Sinai (2013) to 2010 and 2018. Each bar represents an unweighted average by year for the specific group. 95%

confidence bands are shown in black.

The model developed by Gyourko, Mayer, and Sinai (2013) predicts that price–rent

ratios are higher in superstar cities, but it does not account for the growing gap between

superstars and non-superstars over time.

21

B

Price and rent growth rates for 27 major agglomerations

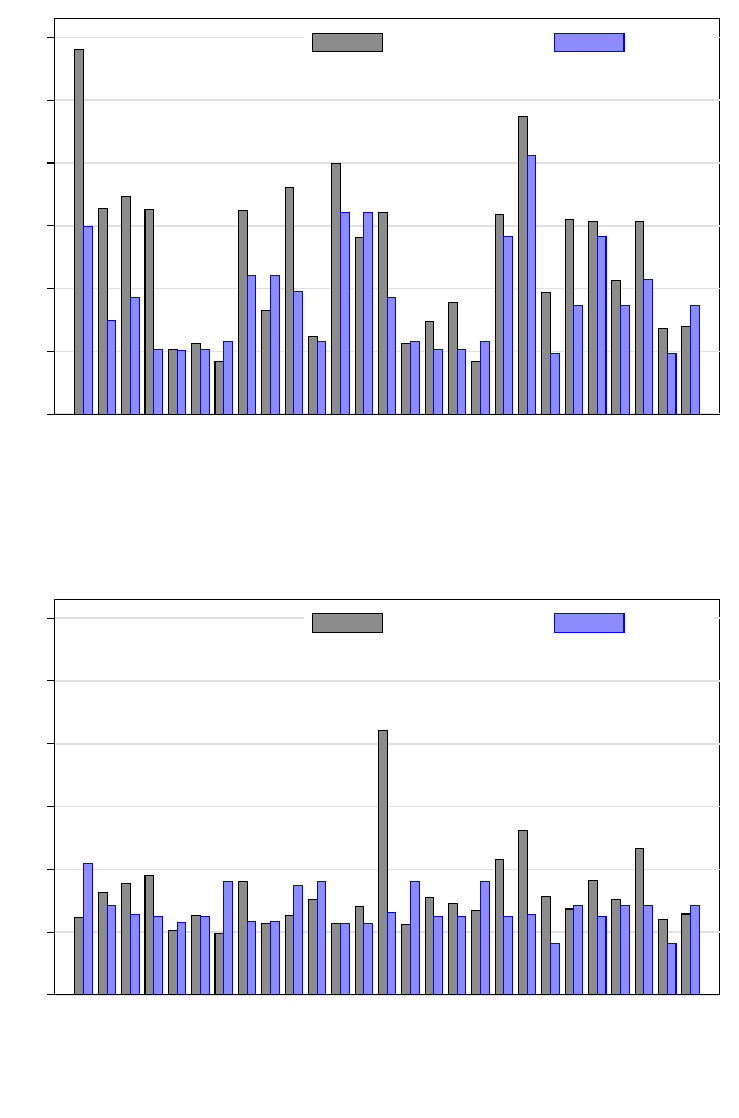

Figure 6: City-level growth rates for 27 major agglomerations compared to national averages

(a) Housing prices

0 1 2 3 4 5 6

London

New York

Paris

Berlin

Tokyo

Hamburg

Naples

Barcelona

Madrid

Amsterdam

Milan

Melbourne

Sydney

Copenhagen

Rome

Cologne

Frankfurt

Turin

Stockholm

Oslo

Toronto

Zurich

Gothenburg

Basel

Helsinki

Vancouver

Bern

Agglomerations National

(b) Rents

0 1 2 3 4 5 6

London

New York

Paris

Berlin

Tokyo

Hamburg

Naples

Barcelona

Madrid

Amsterdam

Milan

Melbourne

Sydney

Copenhagen

Rome

Cologne

Frankfurt

Turin

Stockholm

Oslo

Toronto

Zurich

Gothenburg

Basel

Helsinki

Vancouver

Bern

Agglomerations National

Note: Geometric mean of annual housing price (Panel (a)) and rent (Panel (b)) growth rates by city for 27 major

agglomerations (black) and the respective national averages (blue).

22

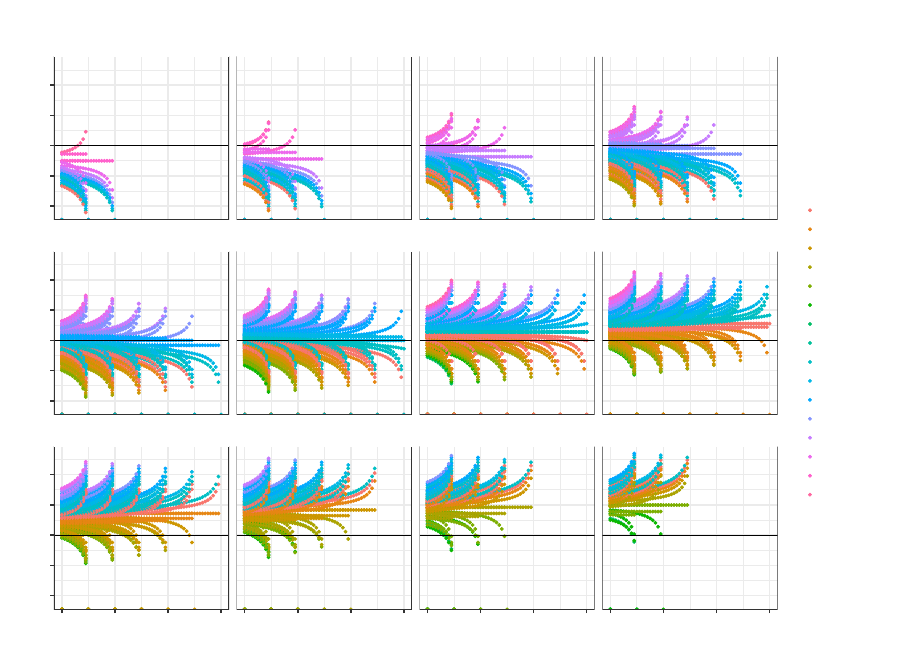

C

Model simulation of risk–free rate fall on housing price

divergence

To examine the scope conditions under which a falling discount rate leads to in-

creasing housing price divergence between the agglomeration and the reservation city,

we simulate our asset-pricing model for a range of potential, and not always realistic,

values. The result displays the housing price divergence (in log) as a function of falling

discount rates (in

%

) and is broken down for all possible combinations of differences

in rent and discount rate growth rates between the agglomeration and reservation city

(7). The figure demonstrates that housing price divergence occurs under a majority of

calibrations, as long as the agglomeration rent growth excess and the reservation city

excess discount rate is sufficiently high.

Figure 7: Simulation results by excess rent growth of agglomeration

2

3

4

5

−2

−1

0

1

−6

−5

−4

−3

0 2 4 6 0 2 4 6 0 2 4 6 0 2 4 6

−5.0

−2.5

0.0

2.5

5.0

−5.0

−2.5

0.0

2.5

5.0

−5.0

−2.5

0.0

2.5

5.0

Fall in discount rate

House price divergence

Reservation city

excess discount

−1

−2

−3

−4

−5

−6

−7

−8

0

1

2

3

4

5

6

7

Major agglomeration rent growth excess

Note: Facets show the percentage points by which the agglomeration’s rent growth exceeds that of the reservation city.

Colors indicate the percentage points by which the reservation city’s discount rate exceeds that of the agglomeration.

23

D Model evidence using U.S. MSA-level data

We also use the U.S. MSA-level data from Gyourko, Mayer, and Sinai (2013), which

was extended to 2018 in Amaral et al. (2021), to test our mechanism empirically. We want

to replicate Figure 3 in the main paper. Our mechanism predicts a one-to-one relation

between rental yields in 1980 and in 2018, with a linear shift due to the fall in real

discount rates (compare Figure 2 in the main paper). It also predicts a non-linear relation

between rental yields in 1980 and price–rent ratios in 2018, with initially lower rental

yield MSAs subsequently having disproportionately higher price–rent ratios (compare

Figure 3 panel (b) in the main paper). As demonstrated below, these predictions hold to

a great extent in the data.

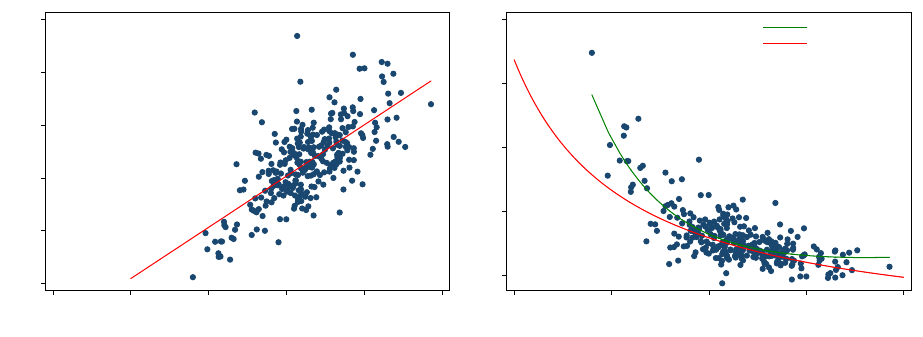

Figure 8 panel (a) plots the rent–price ratios for all MSAs in 2018 relative to the rent–

price ratios in 1980. It also shows a linear fit with the resulting regression coefficients.

Rent–price ratios in 2018 can indeed be predicted by rent–price ratios in 1980 but have

fallen uniformly by approximately 85 basis points. Of course, MSA-level rent–price

ratios do not perfectly align with the regression line. This implies that rent–price ratios

have also been affected by city–specific shocks. Not all variation in rent–price ratios

can be explained by a fall in discount rates alone, however, the linear fit can explain

approximately half of the variation in the data.

Figure 8: Comparison model and U.S. MSA-level data

(a) Rent-price ratio 2018

.01 .02 .03 .04 .05 .06

Rent-price ratio, 2018

.01 .02 .03 .04 .05 .06

Rent-price ratio, 1980

m: 0.973 (0.0583)

y

0

: -0.009 (0.0025)

R squared: 0.489

(b) Price-rent ratio 2018

20 40 60 80 100

Price-rent ratio, 2018

.02 .03 .04 .05 .06

Rent-price ratio, 1980

Fractional fit

Model prediction

Note: Panel (a) shows the rent–price ratios in 2018 relative to the rent–price ratios in 1980 together with a linear fit

and the resulting regression coefficients (standard errors in parentheses). Panel (b) shows the price–rent ratio in

2018 relative to the rent–price ratio in 1980 together with a fractional fit and the predictions of our model resulting

from the linear fit in Panel (a). The data is taken from Gyourko, Mayer, and Sinai (2013) and extended by Amaral

et al. (2021).

Panel (b) of Figure 8 plots price–rent ratios in 2018, also presenting a fractional fit to

the data (green line). The red line depicts the price–rent ratios that the model would

24

predict for 2018, given the rent–price ratio in 1980 and the uniform fall in rent–price

ratios estimated in panel (a). Again, the model does not fit the data perfectly, however,

it does agree with the overall picture of the data and predicts higher price–rent ratios

for cities that already had low rent–price ratios in 1980. The fact that price–rent ratios in

cities with the lowest rental yields initially are even higher than predicted by the model

leaves some room for alternative explanations. One example would be increasingly

more optimistic rent expectations (g) in major agglomerations relative to the rest of the

country. Another would be a tightening of supply constraints in major agglomerations.

E Fall in real safe rates

Several papers have documented the long-run decline in real safe rates across OECD

economies since the 1980s (Del Negro et al., 2019; Rachel and Summers, 2019; Blanchard

and Katz, 1992). Using the estimates from Del Negro et al. (2019), we plot the time-

series evolution of ex-ante real safe rates in the U.S. as well as averaged over 15 OECD

economies in Figure 9. It is evident that real safe rates have been declining considerably

both in the U.S. as well as across the world, since the 1980s.

Figure 9: Global and U.S. Real Safe Rates, 1950-2016

0 1 2 3 4

Real Safe Rates (%)

1950 1960 1970 1980 1990 2000 2010 2020

U.S.

Global

Note: The Figure plots the posterior median of the trend in global and U.S. real safe rates. The estimates are taken

from Del Negro et al. (2019).

25