Federal Student Aid | StudentAid.gov Page 1 of 26

Income-Driven Repayment Plans: Questions and

Answers

Contents

Introduction...........................................................................................................................................................1

General Information .............................................................................................................................................2

Eligible Borrowers ................................................................................................................................................7

Eligible Loans .......................................................................................................................................................9

Monthly Payment Amount ................................................................................................................................. 11

Repayment Period & Loan Forgiveness ........................................................................................................... 15

Married Borrowers ............................................................................................................................................. 18

Application Process ........................................................................................................................................... 20

Miscellaneous ................................................................................................................................................... 24

Introduction

The following questions and answers (Q&A) provide information about the income-driven repayment plans

that are available to most federal student loan borrowers. Throughout the Q&A, we use the following terms:

AGI refers to adjusted gross income, as reported on your federal income tax return.

Direct Loan Program refers to the William D. Ford Federal Direct Loan Program. This program

includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct

Consolidation Loans. Direct Subsidized Loans and Direct Unsubsidized Loans are sometimes called

“Stafford Loans.”

FFEL Program refers to the Federal Family Education Loan Program. This program includes

Subsidized Federal Stafford Loans, Unsubsidized Federal Stafford Loans, Federal PLUS Loans, and

Federal Consolidation Loans. No new loans have been made under this program since July 1, 2010.

Loan servicer refers to the organization that collects your loan payments and completes other

transactions related to your federal student loans. Your loan servicer may or may not be the same

organization as your loan holder (the organization that “owns” your loans). If you are unsure who your

loan servicer is, you can find this information at StudentAid.gov/log-in, or you can call the Federal

Student Aid Information Center (FSAIC) at 1-800-4-FED-AID (1-800-433-3243); (TTY: 1-800-730-

8913).

New borrower refers to an individual who has no outstanding balance on a Direct Loan or FFEL

Program loan when he or she receives a Direct Loan or FFEL Program loan on or after a specified

date.

Parent PLUS Loan refers to a Direct PLUS Loan or Federal PLUS Loan made to a parent borrower

to help pay for the cost of a dependent undergraduate student’s education.

Student PLUS Loan refers to a Direct PLUS Loan or Federal PLUS Loan made to a graduate or

professional student.

Federal Student Aid | StudentAid.gov Page 2 of 26

General Information

1. What is an income-driven repayment plan?

An income-driven repayment plan is a type of repayment plan for federal student loans that can help

make your monthly loan payments more affordable by basing them on your income and family size,

instead of on how much you owe. There are four income-driven repayment plans:

Revised Pay As You Earn Repayment Plan (REPAYE Plan)

Pay As You Earn Repayment Plan (PAYE Plan)

Income-Based Repayment Plan (IBR Plan)

Income-Contingent Repayment Plan (ICR Plan)

The REPAYE Plan, the PAYE Plan, and the ICR Plan are available only to borrowers with loans made

under the Direct Loan Program. The IBR Plan is available to borrowers with loans made under the Direct

Loan Program or the FFEL Program.

Note: These plans have different terms and conditions, and not all borrowers or all loan types qualify for

all of the income-driven plans.

2. Other than providing a more affordable payment, do income-driven plans offer

additional benefits?

Income-driven plans offer the following benefits:

If you repay your loan under any of the income-driven plans and if you still have a loan balance after

20 or 25 years of qualifying repayment, the remaining balance will be forgiven (this time period varies

depending on the plan and other factors).

Payments you make on your Direct Loans under any income-driven plan count toward the 120

payments that are required for the Public Service Loan Forgiveness Program (PSLF). See

StudentAid.gov/publicservice for more information about PSLF.

The REPAYE, PAYE, and IBR plans offer an interest benefit if your monthly payment doesn’t cover

the full amount of interest that accrues on your loans each month. Under all three plans, the

government will pay the difference between your monthly payment amount and the remaining interest

that accrues on your subsidized loans for up to three consecutive years from the date you begin

repaying the loans under the plan. Under the REPAYE Plan, the government will pay half of the

difference on your subsidized loans after this three-year period, and will pay half of the difference on

your unsubsidized loans during all periods.

3. Paying less each month under an income-driven repayment plan seems like a good

thing. Are there any disadvantages?

Whenever you make lower payments or extend your repayment period, you will likely pay more interest

over time—sometimes significantly more—than you would pay under a 10-year Standard Repayment

Plan. Also, under current Internal Revenue Service (IRS) rules, you may be required to pay income tax on

any amount that is forgiven. Carefully consider whether an income-driven plan is the best plan for you

based on your individual circumstances.

Federal Student Aid | StudentAid.gov Page 3 of 26

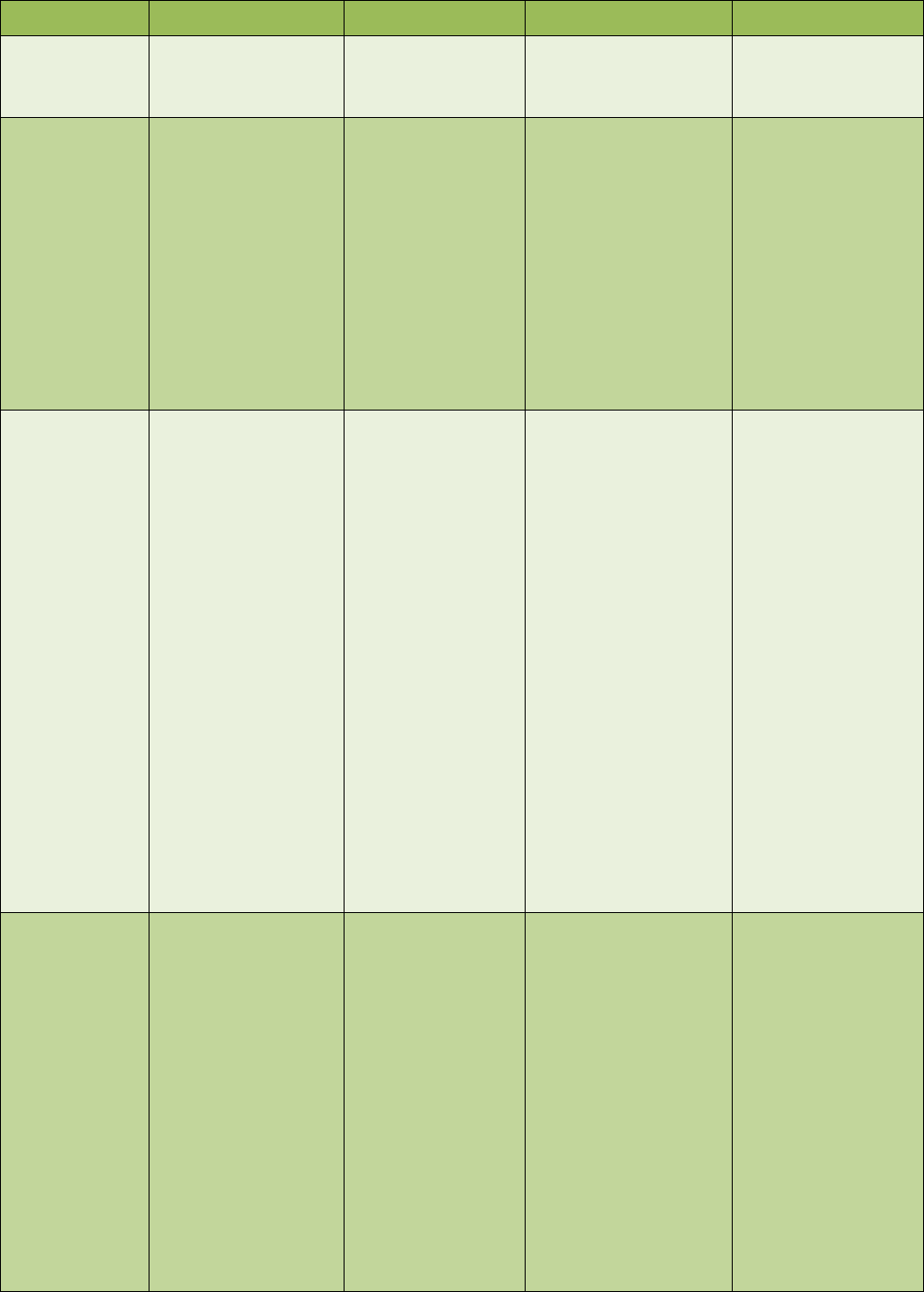

4. What are the differences between the income-driven plans?

The chart below compares the major features of the income-driven plans. The terms and conditions

summarized in the chart are discussed in detail in separate sections of this document. See Eligible

Borrowers, Eligible Loans, Monthly Payment Amount, and Repayment Period & Loan Forgiveness in

this document.

Feature

REPAYE Plan

PAYE Plan

IBR Plan

ICR Plan

Eligible

Borrowers

Direct Loan

borrowers

Direct Loan

borrowers

Note: This plan is

limited to new

borrowers on or

after October 1,

2007, who

received a Direct

Loan disbursement

on or after October

1, 2011.

Direct Loan and FFEL

borrowers

Note: Some terms

and conditions differ

depending on when

you received your

federal student loans.

Direct Loan

borrowers

Eligible Loans

All Direct Loan types

except Parent PLUS

Loans and

consolidation loans

that repaid Parent

PLUS Loans

All Direct Loan

types except

Parent PLUS

Loans and

consolidation loans

that repaid Parent

PLUS Loans

All Direct Loan and

FFEL Program loan

types except Parent

PLUS Loans and

consolidation loans

that repaid Parent

PLUS Loans

All Direct Loan types

except Parent PLUS

Loans.

Consolidation loans

made after July 1,

2006, that repaid

Parent PLUS Loans

may be repaid under

ICR

Income

Requirement

to Enter Plan

None

Your income must

be low compared

to your eligible

federal student

loan debt

Your income must be

low compared to your

eligible federal student

loan debt

None

Requirement

to Recertify

Income and

Family Size

Annually

Annually

Annually

Annually

Monthly

Payment

Generally 10 percent

of your discretionary

income

Generally 10

percent of your

discretionary

income

Generally

10 percent of

your discretionary

income (if you're a

new borrower on

or after July 1,

2014), or

15 percent of

your discretionary

income (if you're

not a new

The lesser of

20 percent

of your

discretionary

income or

what you

would pay on a

repayment plan

with a fixed

payment over

the course of 12

Federal Student Aid | StudentAid.gov Page 4 of 26

Feature

REPAYE Plan

PAYE Plan

IBR Plan

ICR Plan

borrower)

years, adjusted

according to

your income

Cap on

Payment

Amount

None (may be higher

than the 10-year

Standard Repayment

Plan amount)

Never more than

what you would

have paid under

the Standard

Repayment Plan

with a 10-year

repayment period,

based on what you

owed when you

entered the PAYE

Plan

Never more than what

you would have paid

under the Standard

Repayment Plan with

a 10-year repayment

period, based on what

you owed when you

entered the IBR Plan

None (may be

higher than the 10-

year Standard

Repayment Plan

amount)

Married

Borrowers

Payment is generally

based on the

combined income

and loan debt of you

and your spouse,

regardless of

whether you file a

joint or separate

federal income tax

return

If you file a separate

return and you are

separated from your

spouse or are unable

to reasonably access

your spouse's

income, only your

income and loan

debt is used

Payment is based

on the combined

income and loan

debt of you and

your spouse only if

you file a joint

federal income tax

return

Only your income

is considered if you

file a separate

return from your

spouse

Payment is based on

the combined income

and loan debt of you

and your spouse only

if you file a joint

federal income tax

return

Only your income is

considered if you file a

separate return from

your spouse

Payment is based

on the combined

income and loan

debt of you and your

spouse only if you

file a joint federal

income tax return, or

if you and your

spouse choose to

jointly repay under

the plan

Only your income is

considered if you file

a separate return

from your spouse

and do not choose

the joint repayment

option

Repayment

Period & Loan

Forgiveness

Any outstanding

balance is forgiven

after

20 years of

qualifying

repayment if all

loans you're

repaying under

the plan were

received for

undergraduate

study, or

25 years of

qualifying

Any outstanding

balance is forgiven

after 20 years of

qualifying

repayment

Any outstanding

balance is forgiven

after

20 years of

qualifying

repayment (if

you're a new

borrower on or

after July 1, 2014),

or

25 years of

qualifying

repayment (if

you're not a new

Any outstanding

balance is forgiven

after 25 years of

qualifying

repayment

Federal Student Aid | StudentAid.gov Page 5 of 26

Feature

REPAYE Plan

PAYE Plan

IBR Plan

ICR Plan

repayment if any

loans you’re

repaying under

the plan were

received for

graduate or

professional

study

borrower)

Interest

Benefit

If your monthly

payment doesn’t

cover the full amount

of interest that

accrues, the

government pays

the full

amount of the

difference on

your subsidized

loans for the first

three years, and

half of the

difference after

the first three

years, and

half of the

difference on

your

unsubsidized

loans during all

periods

If your monthly

payment doesn't

cover the full

amount of interest

that accrues on

your subsidized

loans, the

government pays

the difference for

the first three years

If your monthly

payment doesn't cover

the full amount of

interest that accrues

on your subsidized

loans, the government

pays the difference for

the first three years

No interest benefit; if

your monthly

payment doesn't

cover the full

amount of interest

that accrues on your

loans, you're still

responsible for

paying the interest

Interest

Capitalization

When

Payment

Doesn’t Cover

All Interest

If your monthly

payment is less than

the amount of

interest that accrues,

any unpaid interest is

capitalized (added to

your loan principal

balance) if

you are

removed from

the plan for

failing to recertify

your income by

the annual

deadline, or

you

voluntarily leave

If your monthly

payment is less

than the amount of

interest that

accrues, any

unpaid interest is

capitalized (added

to your loan

principal balance) if

you no

longer qualify

to make

payments that

are based on

your income or

you leave

the plan

If your monthly

payment is less than

the amount of interest

that accrues, any

unpaid interest is

capitalized (added to

your loan principal

balance) if

you no longer

qualify to make

payments based

on income or

you leave the

plan

There is no limit on

the amount of unpaid

interest that may be

If your monthly

payment is less than

the amount of

interest that

accrues, any unpaid

interest is

capitalized (added

to your loan

principal balance)

annually

When your monthly

payment is less than

the amount of

interest that

accrues, the amount

of unpaid interest

that is capitalized

Federal Student Aid | StudentAid.gov Page 6 of 26

Feature

REPAYE Plan

PAYE Plan

IBR Plan

ICR Plan

the plan

There is no limit on

the amount of unpaid

interest that may be

capitalized under

these conditions

The amount of

unpaid interest that

may be capitalized

if you no longer

qualify to make

payments that are

based on your

income is limited to

10 percent of your

original loan

principal balance at

the time you

entered the PAYE

Plan

capitalized under

these conditions

annually is limited to

10 percent of your

original loan

principal balance at

the time you entered

the ICR Plan

Leaving the

Plan

If you choose to

leave this plan, you

may change to any

other repayment plan

for which you are

eligible

If you choose to

leave this plan, you

may change to any

other repayment

plan for which you

are eligible

If you choose to leave

this plan, you will be

placed on the

Standard Repayment

Plan. If you want to

change from the

Standard Repayment

Plan to a different

repayment plan, you

must first make at

least one payment

under the Standard

Repayment Plan, or

one payment under a

reduced-payment

forbearance (you may

request a reduced-

payment forbearance

if you can’t afford the

Standard Repayment

Plan payment)

If you choose to

leave this plan, you

may change to any

other repayment

plan for which you

are eligible

5. Is there a maximum income limit to qualify for an income-driven repayment plan?

No. There is an income eligibility requirement for the PAYE and IBR plans, but it is not based on a

particular income level. Rather, it compares your income to the amount of your eligible federal student

loan debt. There is no income eligibility requirement for the REPAYE or ICR plans. See Eligible

Borrowers, below, for more information.

6. How can I learn more?

Contact your loan servicer. Find your loan servicer’s contact information at StudentAid.gov/log-in, or

contact the Federal Student Aid Information Center (FSAIC) at 1-800-4-FED-AID (1-800-433-3243); (TTY:

1-800-730-8913).

Federal Student Aid | StudentAid.gov Page 7 of 26

Eligible Borrowers

7. What are the eligibility requirements to repay under an income-driven repayment plan?

The four income-driven repayment plans have different borrower eligibility requirements that are

explained below. Not all borrowers are eligible for each plan.

PAYE Plan and IBR Plan

The PAYE Plan is available only to borrowers with eligible loans made under the Direct Loan Program.

The IBR Plan is available to borrowers with eligible loans made under the Direct Loan Program or the

FFEL Program.

Under the PAYE and IBR plans, your required payment amount is generally a percentage of your

discretionary income. To initially qualify for either plan—and to continue to make payments based on your

income—your income must be low compared to your eligible federal student loan debt.

To determine your eligibility, your loan servicer will do the following:

Determine your monthly payment amount under the PAYE Plan or the IBR Plan, based on your

income and family size.

Determine your monthly payment amount under the 10-year Standard Repayment Plan for your

eligible federal student loans, using either the amount you owed when you first entered repayment on

your loans, or the amount you owe at the time you request the PAYE or IBR plan, whichever is higher.

Compare your 10-year Standard Repayment Plan monthly payment amount with the monthly amount

you would pay under the PAYE or IBR plan based on your income and family size.

If the PAYE or IBR plan monthly payment amount is less than the 10-year Standard Repayment Plan

monthly payment amount, you would meet the initial eligibility requirement. If the amount you would pay

under the PAYE or IBR plan is the same as or more than the amount you would pay under the 10-year

Standard Repayment Plan, you would not benefit from having your monthly payment based on your

income and therefore would not qualify for those plans.

If you meet the eligibility requirement described above, you’re considered to have a “partial financial

hardship.” If you have a partial financial hardship, you qualify to make payments based on income. If you

don’t have a partial financial hardship, you don’t qualify to make payments based on income.

Example

You are single and you owed a total of $40,000 in eligible student loans when your loans first entered

repayment; as a result of capitalized interest (interest that has been added to your loan principal balance)

you now owe $45,000 on those loans.

Your monthly repayment amount under the 10-year Standard Repayment Plan would be $552, based

on $45,000 in loan debt at an interest rate of 8.25%.

If your PAYE or IBR Plan payment amount is less than $552, you would be eligible to repay your

loans under the PAYE Plan (if you meet the other eligibility requirements for this plan) or the IBR Plan.

REPAYE Plan and ICR Plan

The REPAYE and ICR plans do not have an initial eligibility requirement like the PAYE and IBR plans.

Any borrower with an eligible Direct Loan may choose to repay under the REPAYE Plan or ICR Plan.

Federal Student Aid | StudentAid.gov Page 8 of 26

8. Who qualifies for the PAYE Plan?

Your eligibility depends on when you took out federal student loans. You are eligible if

you are a new borrower on or after October 1, 2007, and

you received a disbursement of a Direct Subsidized Loan, a Direct Unsubsidized Loan, or a Direct

PLUS Loan for students on or after October 1, 2011, or you received a Direct Consolidation Loan based

on an application that was received on or after October 1, 2011 (see Note below).

Note: You can’t consolidate your loans to meet the “new borrower” requirement for the PAYE Plan (see

Example 2 below).

The following examples explain who does or does not qualify for the PAYE Plan:

Example 1

You qualify because you were a new borrower and received a Direct Loan disbursement within the

specified time frame.

You received Subsidized Federal Stafford Loans (loans made under the FFEL Program) in

September 2008 and September 2009 and a Direct Subsidized Loan in September 2010.

When you received the loan in September 2008, you had no outstanding balance on any other Direct

Loans or FFEL Program loans.

You then received the first disbursement of another Direct Subsidized Loan in September 2011, and

you received the second disbursement of that loan in January 2012.

Because you had no outstanding balance on a Direct Loan or FFEL Program loan at the time you

received a FFEL Program loan after October 1, 2007 (that is, at the time you received the Subsidized

Federal Stafford Loan in September 2008), and you received a disbursement of a Direct Loan after

October 1, 2011, you qualify.

Alternative: You also would qualify if, instead of receiving the Direct Subsidized Loan in September 2011,

you applied for a Direct Consolidation Loan on or after October 1, 2011, and consolidated the two

Subsidized Federal Stafford Loans you received in September 2008 and September 2009 and the Direct

Subsidized Loan you received in September 2010.

Example 2

You do not qualify because you are not a “new borrower.”

You received Subsidized Federal Stafford Loans in September 2006 and September 2007.

In January 2012 you returned to school and received a Direct Subsidized Loan. At the time you

received this loan, you still had an outstanding balance on the Subsidized Federal Stafford Loans you

received in 2006 and 2007.

Because you had an outstanding balance on FFEL Program loans at the time you received a Direct Loan

after October 1, 2007, you do not qualify even though you received a disbursement of a Direct Loan after

October 1, 2011.

Alternative: If you had repaid the two Subsidized Federal Stafford Loans in full before you received the

Direct Subsidized Loan in January 2012, you would have qualified. However, you could not qualify if you

consolidated the two Subsidized Federal Stafford Loans after October 1, 2011, because you cannot

become eligible for the PAYE Plan by consolidating loans that made you ineligible under the first part of

the eligibility requirement (new borrower).

Note that if you’re not eligible for the PAYE Plan, you could repay your eligible Direct Loan Program

Federal Student Aid | StudentAid.gov Page 9 of 26

loans under the REPAYE Plan, which provides some of the same benefits as the PAYE Plan.

9. Who qualifies as a new borrower for the IBR Plan?

You are a new borrower for the IBR Plan if you had no outstanding balance on any other Direct Loan or

FFEL Program loan when you received a Direct Loan on or after July 1, 2014.

Because no new loans have been made under the FFEL Program since June 30, 2010, only Direct Loan

borrowers can qualify as new borrowers for the IBR Plan.

10. How can I find out if I qualify for an income-driven repayment plan and what my

estimated monthly payment amount would be?

Any borrower with an eligible loan type may choose to repay under the REPAYE Plan or the ICR Plan,

but only your loan servicer can make an official determination of your eligibility and your monthly payment

amounts for the PAYE or IBR plans.

To view estimates of your eligibility and monthly payment amounts under various repayment plans

(including the income-driven plans), use the U.S. Department of Education’s online Repayment Estimator

at StudentAid.gov/repayment-estimator. You can easily import your actual loan data into the

Repayment Estimator or manually enter your loan amounts.

Eligible Loans

11. What types of student loans can be repaid under the income-driven repayment plans?

The chart below shows the types of federal student loans that can be repaid under the income-driven

plans. Private student loans and defaulted federal student loans cannot be repaid under any of the

income-driven plans.

Loan Type

REPAYE

Plan

PAYE Plan

IBR Plan

ICR Plan

Direct Subsidized Loans

Eligible

Eligible

Eligible

Eligible

Direct Unsubsidized Loans

Eligible

Eligible

Eligible

Eligible

Direct PLUS Loans made to graduate or

professional students

Eligible

Eligible

Eligible

Eligible

Direct PLUS Loans made to parents

Not eligible

Not eligible

Not eligible

Eligible if

consolidated*

Direct Consolidation Loans that did not repay

any PLUS loans made to parents

Eligible

Eligible

Eligible

Eligible

Direct Consolidation Loans made on or after

July 1, 2006, that repaid PLUS loans made to

parents

Not eligible

Not eligible

Not eligible

Eligible

Subsidized Federal Stafford Loans (made

under the FFEL Program)

Eligible if

consolidated*

Eligible if

consolidated*

Eligible

Eligible if

consolidated*

Unsubsidized Federal Stafford Loans (made

under the FFEL Program)

Eligible if

consolidated*

Eligible if

consolidated*

Eligible

Eligible if

consolidated*

Federal Student Aid | StudentAid.gov Page 10 of 26

Loan Type

REPAYE

Plan

PAYE Plan

IBR Plan

ICR Plan

FFEL

PLUS Loans made to graduate or

professional students

Eligible if

consolidated*

Eligible if

consolidated*

Eligible

Eligible if

consolidated*

FFEL

PLUS Loans made to parents

Not eligible

Not eligible

Not eligible

Eligible if

consolidated*

FFEL

Consolidation Loans that did not repay

any PLUS loans made to parents

Eligible if

consolidated*

Eligible if

consolidated*

Eligible

Eligible if

consolidated*

FFEL

Consolidation Loans that repaid PLUS

loans made to parents

Not eligible

Not eligible

Not eligible

Eligible if

consolidated*

Federal Perkins Loans

Eligible if

consolidated*

Eligible if

consolidated*

Eligible if

consolidated*

Eligible if

consolidated*

*A loan type identified as “eligible if consolidated” cannot be repaid under the listed income-driven plan.

However, if you consolidate that loan type into a Direct Consolidation Loan, you may then repay the

Direct Consolidation Loan under the listed income-driven plan.

For example, a Subsidized Federal Stafford Loan (a type of loan made under the FFEL Program) cannot

be repaid under the REPAYE Plan because that plan is available only for Direct Loans. However, if you

consolidate a Subsidized Federal Stafford Loan into a Direct Consolidation Loan, you may then repay the

Direct Consolidation Loan under the REPAYE Plan.

Similarly, a Parent PLUS Loan may not be repaid under any of the income-driven repayment plans.

However, if you consolidate a Parent PLUS Loan into a Direct Consolidation Loan, the consolidation loan

can be repaid under the ICR Plan (but not the REPAYE Plan, the PAYE Plan, or the IBR Plan).

Consolidation is not right for all borrowers or all loan types. In particular, you may lose certain loan

benefits if you consolidate a Federal Perkins Loan. Find out more about loan consolidation at

StudentAid.gov/consolidation.

12. If I have private education loans, are they counted as part of my student loan debt when

my servicer determines my eligibility for the PAYE Plan or the IBR Plan?

No. Private education loans are not counted. Only nondefaulted Direct Loans and FFEL Program loans

that are eligible for repayment under the PAYE Plan or the IBR Plan are counted as part of your student

loan debt for purposes of determining your eligibility. This includes private consolidation loans that repaid

federal student loans. Eligible federal student loans that were consolidated into a private consolidation

loan are no longer federal loans and are not considered when determining your eligibility for the PAYE

and IBR plans.

Note: You lose many of the benefits and consumer protections of federal loans when you consolidate

them into a private loan. Find out more about the differences between federal and private student loans at

StudentAid.gov/federal-vs-private.

13. I want to repay my FFEL Program loans under the IBR Plan and my Direct Loans under

the PAYE plan. Will my loan servicers look only at my FFEL Program loan debt when

determining my eligibility for the IBR Plan, and only at my Direct Loan debt when

determining my eligibility for the PAYE Plan?

No. If you have both Direct Loans and FFEL Program loans, the 10-year Standard Repayment Plan

amount that is used in determining your initial eligibility for the PAYE or IBR plan is based on the total

Federal Student Aid | StudentAid.gov Page 11 of 26

amount of all of your Direct Loans and FFEL Program loans that are eligible for repayment under either

the PAYE Plan or the IBR Plan.

If you have both Direct Loans and FFEL Program loans, you could consolidate your FFEL Program loans

that are eligible for the IBR Plan into a Direct Consolidation Loan and then repay the consolidation loan

under the REPAYE Plan or (if you qualify) the PAYE Plan. This will give you a lower monthly payment

amount.

14. I consolidated loans I received to pay for my own education with PLUS loans that I took

out to pay for my child’s education. Can I repay the part of my consolidation loan that

repaid the loans I took out for my own education under one of the income-driven plans?

No. It isn’t possible to repay different portions of a consolidation loan under different repayment plans.

A consolidation loan that repaid a Parent PLUS Loan may not be repaid under the REPAYE Plan, the

PAYE Plan, or the IBR Plan, even if the consolidation loan also repaid one or more eligible loan types.

However, a Direct Consolidation Loan made on or after July 1, 2006, that repaid a Parent PLUS Loan

may be repaid under the ICR Plan.

15. If my loan is in default, can I repay it under an income-driven repayment plan?

No. Defaulted loans are not eligible for repayment under any of the income-driven repayment plans.

However, you may be able to remove your loan from default by making a specified number of monthly

payments in an amount that is determined using a formula similar to the IBR formula and is based on

your income. This is called “loan rehabilitation.” Once you have rehabilitated your defaulted loan, you

could then repay the loan under an income-driven plan.

As an alternative to loan rehabilitation, you may be able to consolidate your defaulted loans into a Direct

Consolidation Loan if you agree to repay the consolidation loan under an income-driven repayment plan.

Contact your loan servicer for more information about loan rehabilitation and consolidation.

Monthly Payment Amount

16. How is the monthly payment amount determined under the income-driven repayment

plans?

Under the REPAYE Plan, your monthly payment amount is always based on your income and family size.

Depending on your income, your monthly payment amount under the REPAYE Plan may be higher than

what you would be required to pay under the 10-year Standard Repayment Plan.

Under the PAYE Plan and the IBR Plan, your monthly payment amount is based on your income and

family size when you first begin repayment under the plan. However, if your income increases to the point

that your calculated monthly payment amount would be more than what you would have to pay under the

10-year Standard Repayment Plan, your monthly payment will be adjusted and will no longer be based on

your income. Instead, your required monthly payment will be the amount you would pay under the 10-

year Standard Repayment Plan, based on the loan amount you owed when you first entered the PAYE or

IBR plan. This ensures that you will never have a monthly payment that is greater than the amount you

would have to pay under the 10-year Standard Repayment Plan.

Under the ICR Plan, your monthly payment will be the lesser of an amount that is calculated based on

your income and loan debt, or an amount calculated based only on income. Depending on your income,

your monthly payment amount under the ICR Plan may be higher than what you would be required to pay

under the 10-year Standard Repayment Plan.

Federal Student Aid | StudentAid.gov Page 12 of 26

17. How is the monthly payment amount calculated under the REPAYE, PAYE and IBR

plans?

Under these plans, your required monthly payment is generally a percentage of your discretionary

income. For all three plans, your discretionary income is the difference between your AGI and 150

percent of the U.S. Department of Health and Human Services (HHS) Poverty Guideline amount for your

family size and state.

Under the REPAYE Plan, your required monthly payment amount is 10 percent of your discretionary

income at all times.

Under the PAYE Plan and the IBR Plan, your required monthly payment is a percentage of your

discretionary income during any period when you qualify to make payments based on income. The

percentage differs depending on the plan.

Under the PAYE Plan, your monthly payment is 10 percent of your discretionary income.

For the IBR Plan, your monthly payment amount is 10 percent of your discretionary income if you’re a

new borrower on or after July 1, 2014. If you’re not a new borrower, your monthly payment amount

under the IBR Plan is 15 percent of your discretionary income.

Example

You are single and your family size is one. You live in one of the 48 contiguous states or the District

of Columbia. Your AGI is $40,000.

You have $45,000 in eligible federal student loan debt.

150 percent of the 2016 HHS Poverty Guideline amount for a family of one in the 48 contiguous

states and the District of Columbia is $17,820. The difference between your AGI and 150 percent of

the Poverty Guideline amount is $22,180. This is your discretionary income.

If you’re repaying under the REPAYE Plan, the PAYE Plan, or (if you’re a new borrower) the IBR

Plan, the calculation works like this:

o 10 percent of your discretionary income is $2,218.

o Dividing this amount by 12 results in a monthly payment of $184.83.

If you are repaying under the IBR Plan and you’re not a new borrower, the calculation works like this:

o 15 percent of your discretionary income is $3,327.

o Dividing this amount by 12 results in a monthly payment of $277.25.

The REPAYE, PAYE, and IBR plan payment amounts shown in the example above compare with a

monthly payment amount of $500 under a 10-year Standard Repayment Plan (based on a loan debt

amount of $45,000 at an interest rate of 6%).

If the REPAYE, PAYE, or IBR Plan amount calculated as described above is less than $5, your required

monthly payment amount is zero. If the calculated payment amount is more than $5 but less than $10,

your required monthly payment is $10.

18. How is the monthly payment amount calculated under the ICR Plan?

Under the ICR Plan, your required monthly payment will be the lesser of

20 percent of your discretionary income, or

Federal Student Aid | StudentAid.gov Page 13 of 26

the amount you would pay under a Standard Repayment Plan with a 12-year repayment period,

multiplied by a percentage that is based on your income (this is called an “income percentage

factor”).

For the ICR Plan, your discretionary income is the difference between your AGI and 100 percent of the

HHS Poverty Guideline amount for your family size and state. This differs from the standard used for the

REPAYE, PAYE, and IBR plans, where discretionary income is based on 150 percent of the Poverty

Guideline amount.

Example

You are single and your family size is one. You live in one of the 48 contiguous states or the District

of Columbia. Your AGI is $40,000.

You have $45,000 in Direct Unsubsidized Loan debt.

The 2016 HHS Poverty Guideline amount for a family of one in the 48 contiguous states and the

District of Columbia is $11,880.

The difference between your AGI and the Poverty Guideline amount is $28,120. This is your

discretionary income.

20 percent of your discretionary income is $5,624. Dividing this amount by 12 results in a monthly

payment amount of $468.67.

Based on $45,000 in Direct Unsubsidized Loan debt at an interest rate of 6%, the monthly amount

you would pay under a Standard Repayment Plan with a 12-year repayment period, multiplied by the

income percentage factor for 2016 that corresponds to your AGI, is $375.06.

Since the payment amount that takes into account both income and loan debt ($379) is less than the

monthly payment amount that is equal to 20 percent of your discretionary income ($468.67), your monthly

payment under the ICR Plan would be $375.06.

The ICR Plan payment amount shown in the example above compares with a monthly payment amount

of $500 under a 10-year Standard Repayment Plan (based on a loan debt amount of $45,000 at an

interest rate of 6%).

If your calculated ICR payment amount is greater than $0 but less than $5, your required monthly

payment amount is $5.

19. Will I always pay the same amount each month under an income-driven repayment

plan?

No. Under all of the income-driven repayment plans, your required monthly payment amount may

increase or decrease if your income or family size changes from year to year. Each year you must

“recertify” your income and family size. This means that you must provide your loan servicer with updated

income and family size information so that your servicer can recalculate your payment. You must do this

even if there has been no change in your income or family size. Your payment amount will be effective for

the 12-month period after it is calculated.

Your loan servicer will send you a reminder notice when it’s time for you to recertify. To recertify, you

must submit another income-driven repayment plan application. On the application, you’ll be asked to

select the reason you’re submitting the application. Respond that you are submitting documentation of

your income for the annual recalculation of your payment amount.

Although you’re required to recertify your income and family size only once each year, if your income or

family size changes significantly before your annual certification date (for example, due to loss of

Federal Student Aid | StudentAid.gov Page 14 of 26

employment), you can submit updated information and ask your servicer to recalculate your payment

amount at any time. To do this, submit a new application for an income-driven repayment plan. When

asked to select the reason for submitting the application, respond that you are submitting documentation

early because you want your servicer to recalculate your payment immediately.

20. If I’m repaying under PAYE or IBR, what happens if my income increases so much that I

no longer qualify to make payments based on income? Do I then lose eligibility to repay

under PAYE or IBR?

No. If your income increases to the point that your calculated PAYE or IBR payment amount is more than

the monthly amount you would be required to repay under a 10-year Standard Repayment Plan, you will

remain on the PAYE or IBR plan, but your monthly payment will no longer be based on your income.

Instead, you will pay the amount you would have been required to pay under a 10-year Standard

Repayment Plan. This 10-year Standard Repayment Plan monthly payment amount will be calculated

based on the amount of your eligible loans that were outstanding when you first began repayment under

the PAYE or IBR plan.

Although your required monthly payment will be the 10-year Standard Repayment Plan amount (as

described above), you will continue repaying your loans under the PAYE or IBR plan, and your maximum

repayment period will remain at 20 or 25 years.

21. If I’m repaying under the PAYE or IBR plan and my income increases so that I no longer

qualify to make payments based on income, but I stay in the plan and make the 10-year

Standard Repayment Plan amount, is it still possible for me to receive loan forgiveness

after 20 or 25 years?

Making payments under the PAYE or IBR plan that are not based on income does not disqualify you from

receiving loan forgiveness. As long as you remain on the PAYE or IBR plan and you meet the other

requirements for loan forgiveness, you will qualify for forgiveness of any loan balance that remains at the

end of the 20- or 25-year period. However, if your income remains high and you continue to make the 10-

year Standard Repayment Plan payment amount, your loans may be repaid in full before the end of the

repayment period.

22. If my loan servicer determines that I no longer qualify to make PAYE or IBR plan

payments based on my income and I am paying a 10-year Standard Repayment Plan

amount, what happens if my income decreases?

During any period when your monthly payment amount is not based on your income, you still have the

option of recertifying your income and family size. If you recertify and your income or family size has

changed so that your calculated PAYE or IBR payment would once again be less than the 10-year

Standard Repayment Plan amount, your servicer will recalculate your payment and you'll return to making

payments that are based on your income.

23. Do Social Security disability payments count as income for purposes of the income-

driven repayment plans?

Social Security disability payments would be counted as income only if they are treated as taxable

income and are included as part of your AGI on your federal tax return, in accordance with IRS

requirements.

Federal Student Aid | StudentAid.gov Page 15 of 26

24. I have loans with different servicers and I want to pay all of my loans under an income-

driven repayment plan. How does each servicer determine if I’m eligible? If I qualify,

how does each servicer determine my payment amount?

If you have loans with different servicers and you want to repay all of your loans under an income-driven

repayment plan, you must apply to each servicer separately, and must check the box on the Income-

Driven Repayment Plan Request indicating that you owe eligible loans to more than one loan holder.

If you apply for the PAYE or IBR plan, each servicer will use the total amount of all of your eligible loans—

that is, your loans that are eligible to be repaid under the PAYE or IBR plans—to determine whether you

are eligible for the plan that you requested, even if some of the loans are with other servicers.

If you’re eligible for the plan you requested, each servicer will first determine your income-driven

repayment plan payment amount and then adjust that amount by multiplying it by the percentage of your

total outstanding eligible loan debt that is serviced by that servicer.

Example

60 percent of your total outstanding eligible loan debt is with Servicer A and 40 percent is with

Servicer B.

Your calculated monthly payment amount under the income-driven plan you have requested is $140.

You would be required to pay $84 per month (60 percent of $140) to Servicer A and $56 (40 percent

of $140) to Servicer B.

Repayment Period & Loan Forgiveness

25. If I choose an income-driven repayment plan, how much time do I have to repay my

loans?

For the REPAYE Plan:

If all of the loans you’re repaying under the REPAYE Plan were received for undergraduate

study (including any consolidation loan that repaid only loans received for undergraduate study),

the repayment period is 20 years.

If any of the loans you’re repaying under the REPAYE Plan were received for graduate or

professional study (including any consolidation loan that repaid a loan received for graduate or

professional study), the repayment period is 25 years.

For the PAYE Plan, the repayment period is 20 years.

For the IBR Plan:

If you’re a new borrower, the repayment period is 20 years.

If you’re not a new borrower, the repayment period is 25 years.

For the ICR Plan, the repayment period is 25 years.

Under each plan, any loan amount remaining after 20 or 25 years (as applicable) of qualifying repayment

will be forgiven.

There is a significant difference between the repayment period for an income-driven repayment plan and

the repayment period for the Standard, Graduated, or Extended repayment plans.

Under the Standard, Graduated, or Extended repayment plans, the repayment period is the period of time

Federal Student Aid | StudentAid.gov Page 16 of 26

over which you must repay your loan in full. Your monthly payment is set at an amount (based on your

loan balance and interest rate) that will ensure your loan is fully repaid within the maximum repayment

period for the plan you have chosen.

In contrast, the repayment period under an income-driven repayment plan is the maximum period of time

over which you must make payments, but you might not repay your loan in full by the end of the

repayment period. Your monthly payment amount under an income-driven repayment plan is generally

based on your income and family size, and may increase or decrease over the course of the repayment

period if your income or family size changes. As a result, the total amount of your payments might not be

enough to fully repay your loans after 20 or 25 years of qualifying repayment. Any loan balance that

remains will be forgiven. However, keep in mind that under current law the IRS considers loan amounts

forgiven under an income-driven repayment plan to be taxable income.

26. I began repaying loans I received for an undergraduate program under REPAYE. I later

went to graduate school and received new loans. When I began repaying my graduate

student loans under REPAYE, the repayment period for my undergraduate loans

changed. Why?

Under the REPAYE plan, your repayment period varies depending on whether you received all of the

loans you’re repaying under REPAYE as an undergraduate student (in which case the repayment period

is 20 years) or whether you received any of the loans you’re repaying under REPAYE as a graduate or

professional student (in which case the repayment period is 25 years).

In this situation, the repayment period for the loans you received for undergraduate study would be

extended from 20 years to 25 years as soon as the first loan you received for graduate study entered

repayment. However, time already spent in qualifying repayment on the undergraduate loans would count

toward the new 25-year repayment period for those loans.

27. If I repay my loans under an income-driven repayment plan, am I guaranteed to receive

forgiveness of at least some of my federal student loan debt?

No. Your monthly payment may increase or decrease over time based on changes in your income and

family size, as explained in other items in this Q&A document. Depending on your individual

circumstances, you may end up repaying your loan in full by the end of the repayment period.

28. What does “after 20 or 25 years of qualifying repayment” mean?

This means that you will qualify for forgiveness of any remaining loan balance after you have made the

equivalent of 20 or 25 years of qualifying monthly payments, and after at least 20 or 25 years have

passed.

Generally, a qualifying monthly payment for any of the income-driven repayment plans is a payment

made under

any income-driven repayment plan, whether based on your income or the 10-year Standard

Repayment Plan amount;

the 10-year Standard Repayment Plan; or

any other repayment plan, if the payment amount is at least equal to what the payment amount would

be under the 10-year Standard Repayment Plan.

For example, if you began repayment under the 10-year Standard Repayment Plan and later changed to

one of the income-driven repayment plans, the monthly payments you made under the 10-year Standard

Federal Student Aid | StudentAid.gov Page 17 of 26

Repayment Plan will generally count toward the required 20 or 25 years of qualifying monthly payments

for the income-driven repayment plan. Similarly, if you were previously in repayment under one income-

driven repayment plan and later switched to a different income-driven repayment plan, payments you

made under both plans will generally count toward the required years of qualifying monthly payments for

the new plan.

Also, any month that you are in an economic hardship deferment generally counts as the equivalent of a

qualifying monthly payment for purposes of the income-driven repayment plans. That is, even though you

are not required to make payments on your loans during a deferment, any months spent in an economic

hardship deferment while you are repaying under an income-driven repayment plan will generally count

toward the required 20 or 25 years of qualifying monthly payments. (Note that months spent in any other

type of deferment or months spent in forbearance do not count as the equivalent of qualifying monthly

payments.)

Depending on the repayment plan, only payments you made after a certain date or months of economic

hardship deferment after a certain date may be counted toward the required 20 or 25 years of qualifying

monthly payments. For the ICR Plan, payments made under certain other repayment plans (in addition to

those listed above) may also count toward the required 25 years of qualifying monthly payments,

depending on when you first entered repayment on your loans. Your loan servicer can provide you with

more detailed information about these requirements.

If 20 or 25 years (as applicable) have passed, but you have not made the equivalent of 20 or 25 years of

qualifying monthly payments, you would not yet be eligible to receive forgiveness of any remaining loan

balance. The example below explains this.

Example

You entered repayment under the REPAYE Plan in December 2015.

To qualify for forgiveness of any remaining loan balance at the end of the 20-year repayment period,

you must have made the equivalent of 20 years of qualifying monthly payments (240 qualifying

monthly payments) and 20 years must have elapsed.

In 2019, you receive forbearance for 12 months.

In 2022, you receive an economic hardship deferment for 12 months.

After 20 years have elapsed (December 2035), you have made the equivalent of 19 years of

qualifying monthly payments (216 monthly payments under the REPAYE Plan, plus 12 months of

economic hardship deferment, for a total of 228 qualifying monthly payments). The 12 months of

forbearance do not count toward the required 20 years of qualifying monthly payments. Therefore,

you would not qualify for forgiveness of any remaining loan balance until after you have made the

equivalent of an additional 12 months of qualifying monthly payments.

29. If my required monthly payment amount under an income-driven repayment plan is

zero, does that still count as qualifying repayment?

Yes. Any month when your required payment is zero will count as qualifying repayment.

30. How will I know when I’m eligible to receive forgiveness of any remaining loan balance?

Your loan servicer will track your qualifying monthly payments and years of repayment and will notify you

when you are getting close to the point when you would qualify for forgiveness of any remaining loan

balance.

Federal Student Aid | StudentAid.gov Page 18 of 26

Married Borrowers

31. Is my spouse's income included when my servicer determines my eligibility for an

income-driven repayment plan or my monthly payment amount?

It depends on the plan and, for some of the plans, how you and your spouse file your federal income tax

return.

REPAYE Plan

Your loan servicer will generally use both your income and your spouse's income to calculate your

monthly payment amount, regardless of whether you file a joint federal income tax return or separate

federal income tax returns.

However, only your individual income will be used to calculate your monthly payment amount if you are

separated from your spouse or are unable to reasonably access your spouse's income. If you filed your

last tax return jointly with your spouse, you’ll provide alternative documentation of your income, such as a

pay stub. If you filed your last tax return separately from your spouse, you can provide your tax return as

documentation of your income.

PAYE Plan, IBR Plan, and ICR Plan

If you and your spouse file separate federal income tax returns, your loan servicer will use only your

income when determining whether you qualify for the PAYE Plan or the IBR Plan, and when calculating

your monthly payment amount under the PAYE, IBR, or ICR plans.

If you and your spouse file a joint federal income tax return, your loan servicer will use your joint income

when determining your eligibility for the PAYE or IBR plan, and when calculating your payment amount

under the PAYE, IBR, or ICR plans. However, only your individual income will be used to calculate your

monthly payment amount if you are separated from your spouse or are unable to reasonably access your

spouse’s income. In this case, you’ll provide alternative documentation of your income, such as a pay

stub.

32. If my spouse also has federal student loans, how will this affect the determination of my

eligibility for an income-driven repayment plan or my monthly payment amount?

This depends on the plan, as explained below.

REPAYE Plan

Generally, your servicer will automatically adjust your payment amount proportionally, based on each

spouse’s share of the total loan debt. For example, if the calculated REPAYE Plan payment amount for

you and your spouse (based on your joint income) is $200 and you owe 60 percent of your combined loan

debt and your spouse owes 40 percent, your individual REPAYE Plan payment would be $120, and your

spouse’s individual REPAYE Plan payment would be $80. If you and your spouse have loans with more

than one loan servicer, your payment amounts will be further adjusted.

PAYE Plan and IBR Plan

If you and your spouse file a joint federal income tax return, your servicer will use your combined eligible

student loan debt when determining your eligibility for the PAYE Plan or the IBR Plan, and will

automatically adjust your payment amount proportionally, based on each spouse’s share of the total loan

debt. If you file separate federal income tax returns, only your eligible student loan debt will be used when

determining your eligibility for the plan, and there will be no adjustment to your payment amount if your

spouse also has eligible loans.

Federal Student Aid | StudentAid.gov Page 19 of 26

ICR Plan

If your spouse also has eligible Direct Loans, you may choose to repay your loans jointly under the ICR

Plan. If you choose to repay your Direct Loans jointly with your spouse under ICR, your servicer will

calculate separate ICR payment for each of you that is proportionate to your individual share of your

combined Direct Loan debt.

All IDR Plans

Unless you and your spouse choose the joint repayment option under the ICR Plan, your spouse is not

required to request an income-driven repayment plan in order for the adjustments described above to be

made. Your spouse may choose a different repayment plan but may need to provide authorization for

your loan servicer to access his or her loan information in the National Student Loan Data System

(NSLDS®).

33. My spouse and I file a joint federal tax return, but my spouse doesn’t have federal

student loans that are eligible for repayment under an income-driven repayment plan.

However, my spouse has private education loans and other debt. If I apply for an

income-driven repayment plan, will my loan servicer consider my spouse’s debt?

No. Only eligible federal student loan debt is considered when determining your eligibility or payment

amount under an income-driven repayment plan. Private education loans and other debt (either yours or

your spouse’s) are not considered.

34. My spouse and I file separate federal income tax returns. However, we live in a

community property state and are required to combine our incomes and split the total

amount evenly for federal income tax reporting purposes. If I apply for an income-driven

repayment plan, can my loan servicer consider only my individual income when

determining my eligibility and payment amount?

Your loan servicer may allow you to submit alternative documentation of your individual income that

would be used instead of the AGI shown on your federal income tax return. Before you submit alternative

documentation of your income, check with your loan servicer to see if this option is available.

35. My spouse and I have a joint consolidation loan. Can we repay the loan under an

income-driven repayment plan?

Yes. However, you and your spouse must each request the same income-driven repayment plan. Also,

regardless of how you and your spouse file your federal income tax return (jointly or separately), your

loan servicer will determine your eligibility and payment amount based on your and your spouse’s

combined income and eligible federal student loan debt.

36. My spouse and I want to consolidate our loans into a single joint consolidation loan and

then apply for an income-driven repayment plan. Is this possible?

No. The law no longer allows married borrowers to consolidate their loans into a single joint consolidation

loan. If you and your spouse both want to repay your loans under an income-driven repayment plan, you

must apply separately.

Federal Student Aid | StudentAid.gov Page 20 of 26

Application Process

37. How do I apply for an income-driven repayment plan?

You can apply online at StudentLoans.gov or request a paper Income-Driven Repayment Plan Request

from your loan servicer.

The Income-Driven Repayment Plan Request is a single application that covers all the income-driven

repayment plans. You can request a specific income-driven plan, or (the recommended approach) you

can request that your loan servicer determine which plans you are eligible for and then place you on the

plan that will provide the lowest monthly payment amount.

If you have more than one servicer for the loans that you want to repay under an income-driven plan, you

must submit a separate Income-Driven Repayment Plan Request to each servicer. If you are unsure who

your loan servicer is, you can find this information at StudentAid.gov/login or you can call the Federal

Student Aid Information Center (FSAIC) at 1-800-4-FED-AID (1-800-433-3243); (TTY: 1-800-730-8913).

38. How do I provide the income and family size information that my loan servicer needs to

determine my eligibility for an income-driven repayment plan and my monthly payment?

This depends on whether you submit the Income-Driven Repayment Plan Request electronically or

complete the paper form.

If you apply electronically, you have the option to provide your AGI electronically by using the IRS

Data Retrieval Tool on StudentLoans.gov, which allows you to transfer income information from your

federal tax return. This option is available if

you filed a federal income tax return in the past two years, and

your current income isn’t significantly different from the income reported on your most recent

federal income tax return.

If you complete the paper Income-Driven Repayment Plan Request, you can attach a copy of your

federal income tax return or an IRS tax return transcript (your loan servicer needs only the page that

shows your AGI).

With either the electronic or paper option, you will be required to certify your family size on the

application.

39. Once I’ve been placed on an income-driven repayment plan, do I have to reapply for the

plan each year?

You don’t have to reapply for the plan, but each year you must “recertify” your income and family size by

providing your loan servicer with updated information that will be used to recalculate your monthly

payment amount. You must do this even if there has been no change in your income or family size.

To recertify, you must submit a new Income-Driven Repayment Plan Request. You’ll be asked to select

the reason for submitting the application. Respond that you are submitting documentation of your income

for the annual recalculation of your payment amount. Generally, you’ll recertify income and family size

around the same time of the year that you first began repayment under the income-driven plan that you

selected. Your loan servicer will send you a reminder notice when it’s time for you to recertify.

Federal Student Aid | StudentAid.gov Page 21 of 26

40. What will happen if I don’t recertify my income and family size by the annual deadline?

It’s important for you to recertify your income and family size by the specified annual deadline. If you don’t

recertify your income by the deadline, the consequences vary depending on the plan.

Under the REPAYE Plan, if you don’t recertify your income by the annual deadline, you’ll be removed

from the REPAYE Plan and placed on an alternative repayment plan. Under this alternative

repayment plan, your required monthly payment is not based on your income. Instead, your payment

will be the amount necessary to repay your loan in full by the earlier of 10 years from the date you

begin repaying under the alternative repayment plan, or the ending date of your 20- or 25-year

REPAYE Plan repayment period. You may choose to leave the alternative repayment plan and repay

under any other repayment plan for which you are eligible.

Under the PAYE Plan, the IBR Plan, or the ICR Plan, if you don’t recertify your income by the annual

deadline, you’ll remain on the same income-driven repayment plan, but your monthly payment will no

longer be based on your income. Instead, your required monthly payment amount will be the amount

you would pay under a Standard Repayment Plan with a 10-year repayment period, based on the

loan amount you owed when you initially entered the income-driven repayment plan. You can return

to making payments based on income if you provide your servicer with updated income information,

and if your updated income still qualifies you to make payments based on income.

In addition to the consequences described above, if you don’t recertify your income by the annual

deadline under the REPAYE, PAYE, and IBR plans, any unpaid interest will be capitalized (added to the

principal balance of your loans). This will increase the total cost of your loans over time, because you will

then pay interest on the increased loan principal balance.

Under all of the income-driven repayment plans, if you don’t recertify your family size each year, you’ll

remain on the same repayment plan, but your servicer will assume that you have a family size of one. If

your actual family size is larger, but your servicer assumes a family size of one because you didn’t

recertify your family size, this could result in an increased monthly payment amount or (for the PAYE and

IBR plans) loss of eligibility to make payments based on income.

41. If I’m removed from the REPAYE Plan because I didn’t recertify my income by the

annual deadline, is it possible to return to the REPAYE Plan?

You can return to the REPAYE Plan only if you provide your servicer with documentation of your income

for the period when you were not on the REPAYE Plan. Depending on how long it has been since you left

or were removed from REPAYE, this could be the same income documentation that you would normally

submit to enter REPAYE (like your most recent tax return), or it could be income documentation from prior

years.

Your servicer will then calculate what your monthly payment amount would have been under the

REPAYE Plan during that period, and will compare this amount to your monthly payment amount under

the alternative repayment plan (or any other plan) over the same period.

If the amount you would have been required to pay under the REPAYE Plan is more than what your

monthly payment amount was under the alternative plan or another plan during this period, your new

REPAYE Plan payment amount will be increased. The amount of the increase will be equal to the

difference between what you were required to pay during the period when you were not on the REPAYE

Plan, and the amount you would have been required to pay if you had remained on the REPAYE Plan,

divided by the number of months remaining in your 20- or 25-year repayment period.

Federal Student Aid | StudentAid.gov Page 22 of 26

For example:

You received loans for undergraduate study and begin repaying those loans under the REPAYE Plan

when they first enter repayment. Because all of the loans you are repaying under REPAYE were

received for undergraduate study, your repayment period is set at 20 years.

After your first year of repayment under the REPAYE Plan, you do not recertify your income.

Starting with year 2 of repayment, you are placed on the alternative repayment plan. Your repayment

period is set at 10 years, because 10 years is less time than the remaining portion (19 years) of your

REPAYE Plan repayment period.

Your payment amount under the Alternative Repayment Plan is $200 per month, and you pay this

amount for 12 months.

You decide to reenter REPAYE and provide the necessary documentation to your loan servicer. Your

loan servicer determines that your REPAYE payment amount for the past year would have been $300

per month.

You paid $1,200 less over the course of the year under the alternative repayment plan than you

would have paid during the same period under the REPAYE Plan.

When you reenter REPAYE, you will have 18 years of your repayment period remaining, so the

$1,200 is divided by 216 (there are 216 months in 18 years), which equals $5.55 per month. This

amount will be added to your payment amount each month that you remain in REPAYE.

Your payment amount under REPAYE for the upcoming year (based on newer income

documentation) will be $150 per month.

After the increase is added in, your total REPAYE payment will be $155.55 per month for the next

year.

42. How long will it take my loan servicer to process my Income-Driven Repayment Plan

Request?

The time varies, depending on whether you apply electronically or submit a paper Income-Driven

Repayment Plan Request. It may take a few weeks, since the servicer will need to obtain documentation

of your income and family size. If you are currently repaying your loans under a different repayment plan,

your loan servicer may apply a forbearance to your student loan account while processing your request

for an income-driven repayment plan.

43. I want to apply for an income-driven repayment plan, but the AGI shown on my most

recent federal income tax return is significantly higher than my current income. I had to

change jobs and I’m now earning much less than I earned during the period covered by

my most recent tax return. What can I do?

If your AGI doesn’t accurately reflect your current circumstances, you can submit alternative

documentation of your income, such as your latest pay stubs. The Income-Driven Repayment Plan

Request (both electronic and paper) provides detailed guidance on submitting alternative documentation

of income.

Federal Student Aid | StudentAid.gov Page 23 of 26

44. What if I have untaxed income such as welfare, food stamps, or certain forms of

disability payments? Do I need to submit documentation of income from those sources?

No. You need to document income from taxable sources only (that is, income that you must report on

your federal income tax return). Benefits such as Temporary Assistance for Needy Families or

Supplemental Security Income (SSI) are not taxable income, and should not be reported.

45. If I have no income, how do I document this when I apply for an income-driven

repayment plan?

If you have no income, you can certify your status when you complete the Income-Driven Repayment

Plan Request. You do not have to provide any additional documentation, unless you are required to do so

by your loan servicer.

46. What happens if my income changes significantly before the annual date when I’m

required to recertify my income?

If your income has significantly decreased or increased, you may (but are not required to) ask your

servicer to recalculate your current monthly payment amount at any time. You can do this by submitting a

new Income-Driven Repayment Plan Request and checking the box to indicate that you are requesting a

recalculation due to a change in your circumstances. You will be required to provide documentation of

your current income.

If your loan servicer recalculates your monthly payment based on your request, this will change the

annual date that you are required to provide updated income information and certify your family size. The

new date will be one year from the date your monthly payment is recalculated, and then each year at

around the same time.

As noted above, you’re not required to report changes in your financial circumstances before the annual

date when you must provide updated income information. You can choose to wait until your loan servicer

tells you that you need to provide updated income information at the normally scheduled time. If you

choose to wait, your current required monthly payment amount would remain the same until you provide

the updated income information.

47. I understand that I must report my family size when I first apply for an income-driven

repayment plan and then annually as long as I remain on the plan. I don’t claim my child

as a dependent on my taxes and don’t have physical custody of my child, but I

contribute significantly to my child’s support. Do I count my child when reporting my

family size?

For all income-driven repayment plans, your family size includes your children if they receive more than

half of their support from you. You may count your child when determining your family size if you provide

more than half of the child’s financial support, regardless of who claims the child for tax purposes or who

has physical custody. If you don’t provide more than half of your child’s support, you may not include the

child in your family size for income-driven repayment plan purposes.

48. Can I apply for an income-driven repayment plan while I’m in a deferment or

forbearance?

Yes. If you wish to begin making payments under an income-driven plan before your deferment or

forbearance is over, ask your loan servicer to end the deferment or forbearance early. You can do this on

Federal Student Aid | StudentAid.gov Page 24 of 26

the income-driven repayment application.

Miscellaneous

49. I understand that under the REPAYE, PAYE, and IBR plans, the government will pay

some of the interest on my loans. How does this work?

Under the REPAYE, PAYE, and IBR plans, your calculated monthly payment amount may not cover all of

the interest that accrues on your loans each month (this is called “negative amortization”). In this

situation, the government will pay all or a portion of the remaining unpaid accrued interest that is due

each month. The specific interest benefit varies depending on the plan.

Under the REPAYE Plan, if your calculated monthly payment doesn’t cover all of the interest that

accrues, the government will pay

all of the remaining interest that is due on your subsidized loans (including the subsidized portion of a

consolidation loan) for up to three consecutive years from the date you begin repaying your loans

under the REPAYE Plan, and half of the remaining interest on your subsidized loans following this

three-year period; and

half of the remaining interest that is due on your unsubsidized loans (including the unsubsidized

portion of a consolidation loan), during all periods.

For example, if the monthly interest that accrues on your subsidized loans is $40, but your monthly

REPAYE Plan payment covers only $25 of this amount, the government will pay the remaining $15 for the

first three consecutive years from the date you began repaying your loans under the REPAYE Plan, and

will pay $7.50 of the remaining $15 in interest after this three-year period. If the monthly interest that

accrues on your unsubsidized loans is $30, but your monthly REPAYE Plan payment covers only $20 of

this amount, the government will pay $5 of the remaining $10 in interest during all periods.

Under the PAYE Plan and the IBR Plan, if your calculated monthly payment doesn’t cover all of the

interest that accrues on your subsidized loans (including the subsidized portion of a consolidation loan),

the government will pay all of the remaining interest that is due for up to three consecutive years from the

date you begin repaying your loans under the PAYE or IBR plan.

For example, if the monthly interest that accrues on your subsidized loans is $40, but your monthly PAYE

or IBR plan payment covers only $25 of this amount, the government will pay the remaining $15 for the

first three consecutive years from the date you began repaying your loans under the PAYE or IBR plan.

Under the PAYE or IBR plan, you are responsible for paying all of the interest that accrues on your

unsubsidized loans, as well as all of the interest that accrues on your subsidized loans after the end of the

three-year interest subsidy period. Interest that’s not covered by your monthly payment will continue to

accumulate and will be capitalized (added to your loan principal balance) if you no longer qualify to make

payments based on income, or if you leave the PAYE or IBR plan.

Under all three plans, the consecutive three-year period during which the government pays all of the

remaining interest that accrues on your subsidized loans does not include periods of economic hardship

deferment. However, periods of any other type of deferment or forbearance are counted.

For example, if you receive the interest subsidy benefit on your subsidized loans for your first year of